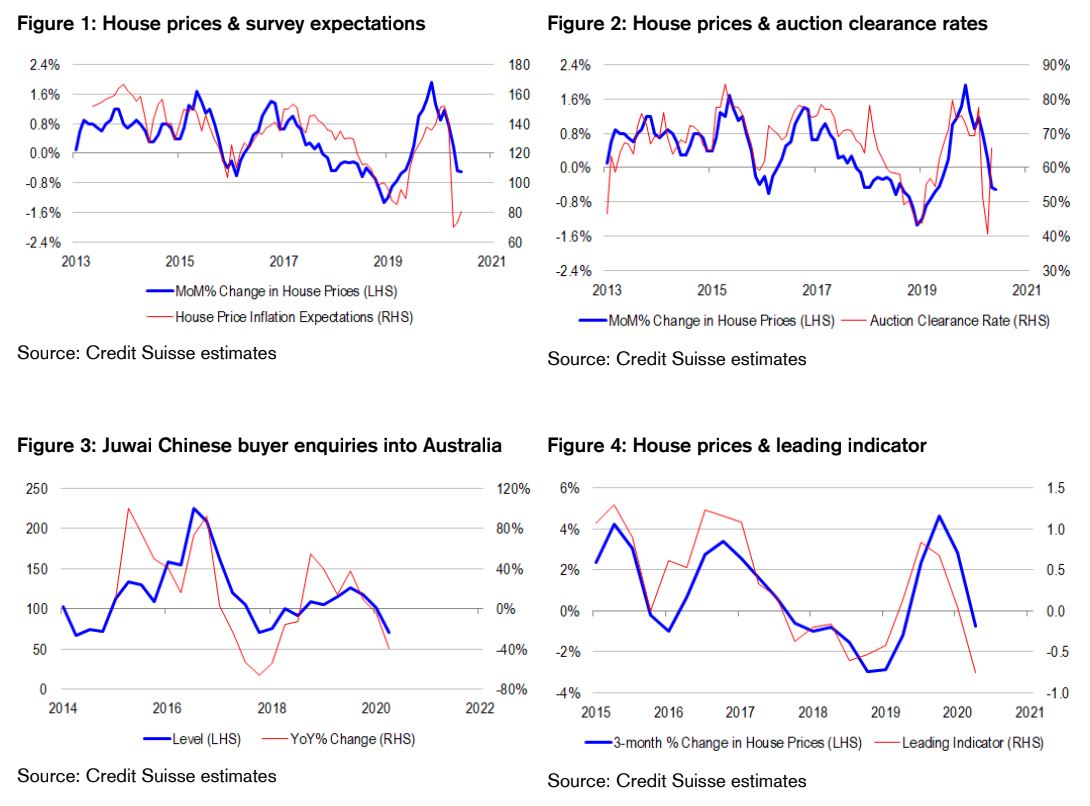

The need to triangulate sparse housing data. Following the recent Freedom of Information Act (FoIA) release of internal Reserve Bank of Australia (RBA) files, we now know that Bank officials are quite concerned about house price measurement distortions in a low turnover environment. Indeed, property data vendors like CoreLogic share these concerns, as evidenced by the temporary halt to publication of daily hedonic house price measures in recent times. Therefore, RBA officials are triangulating different data points to be able to cross-check the accuracy of real-time house price data. Historically, RBA officials rely heavily on weekly auction clearance rates – but clearly these are currently being distorted by low listing volumes and were being distorted for a time by COVID-19 shutdowns. Unsurprisingly then, officials are turning to the Westpac Consumer Survey measure of house price inflation expectations, and indeed cite this measure quite frequently in the FoIA files. In this article, we suggest that policy makers and investors add a third indicator to their toolkits – Juwai Chinese buyer enquiries. After all, household formation in Australia is heavily dependent upon net overseas migration driving population growth, and Chinese are among the most significant and wealthy migrants over the past decade or so.

Juwai buyer enquiries are falling and extremely volatile. The common claim from RBA officials is that Chinese property buying is either limited or immeasurable. Against this backdrop, it is important to note that Juwai offers real-time data from their online portal on Chinese interest in properties abroad. They release data points on buyer enquiries into the Australian market selectively, and not necessarily on a consistent basis. But it is possible to piece together the data they do provide to construct a historical series of buyer enquiries. To be sure, piecing together and reconciling different Juwai data points is time and energy consuming, much like trying to do the same for Chinese official economic data! That said, we think that the excercise is incredibly worthwhile. Juwai make available their Australian “dwelling investment tracker” from 2014 to early 2019. Since 2019, we need to add on incremental updates from newsflow. Juwai reports than in the year-to-September 2019, buyer enquiries rose by 37.3%. For the year 2019, they report that buyer enquiries rose by 8.9% (although it unclear whether this is a calendar year-average or year-ended growth figure). For 1Q 2020, Juwai reports an 8.6% monthly rise in enquiries in January, a fall in February due to COVID-19 shutdowns, a 12.7% rebound in March, and a quarterly decline of 14%. In April 2020, they report a doubling of enquiries relative to each month in 1Q, and in May, they report a 65% reduction, citing geo-political tensions as a reason for the sharp pullback. Juwai also tells us that in May, the level of buyer enquiries dropped to its lowest level in almost 3 years. We can broadly reconcile all of these data points if we assume that the 8.9% rise in buyer enquiries in 2019 is a year-ended figure, that the 14% 1Q 2020 decline is a quarter-ended figure, and that the 100% April 2020 increase is a month on prior quarter average figure. The reported profile of buyer enquiries is consistent with trend weakness since 3Q 2019 and incredible volatility, with April being something of an outlier. Note that mathematically, a movement from 1 to 2 is a 100% increase – but the same movement from 2 to 1 is only a 50% reduction. Percentage movements are relative and base-dependent. Therefore, the near-doubling of buyer enquiries in April is completely overshadowed by the 65% reduction seen in May, resulting in the series level approaching historical lows. What concerns us is not just the weakness in buyer enquiries – but the sheer volatility from month to month, because if Chinese buying interest is volatile, we should expect housing demand and prices to be just as uncertain. We are not completely convinced by the claim that geo-political tensions are driving the volatility, because China is experiencing acceleration of capital flight, and it therefore makes sense that stricter capital controls are being put in place, generally weighing on buyer enquiries. But regardless of the cause, higher volatility in Chinese flows is not a positive development for the housing market in such unprecedented and uncertain times.

Proprietary housing market indicator pointing to prices falling by more than 2% a quarter. In the spirit of corroboration, we construct a housing market indicator using year-ended growth in Juwai Chinese buyer enquiries into Australian property, Westpac house price inflation expectations (expressed as a deviation from neutral levels), and auction clearance rates (expressed as a deviation from the “break-even” 60% level). After scaling each variable for its historical volatility and averaging across Z-scores, we arrive at a very useful leading indicator of house price inflation. Currently, it points to house prices falling by more than 2% per quarter, reflecting sharp weakness in buyer enquiries and extremely subdued house price inflation expectations on the one hand, and a moderate recovery in auction clearance rates on the other. Importantly, the indicator’s predicted rate of house price decline is faster than the rate being recorded by CoreLogic data at present. Therefore, we are inclined to be sceptical about claims that the moderate increase in clearance rates recently is a sign of housing market stability. Rather, we think that the sharpness of the downturn in the market is greater than what was experienced from 2018-2019. We hesitate to extrapolate the projected quarterly pace of house price decline into a peak-to-trough forecast because we simply do not know how long foreign buying interest will be subdued for. But we suspect that soft border closures will remain in place at least until the end of 2020 on government advice, and because COVID-19 and its mutations are still out there without an adequate treatment, cure or vaccine. Therefore, it is reasonable to expect that house prices will fall by 2% or more for several quarters. And in any case, we are not just concerned about the direction of house prices, but also, the volatility of prices as a driver of investor behaviour.

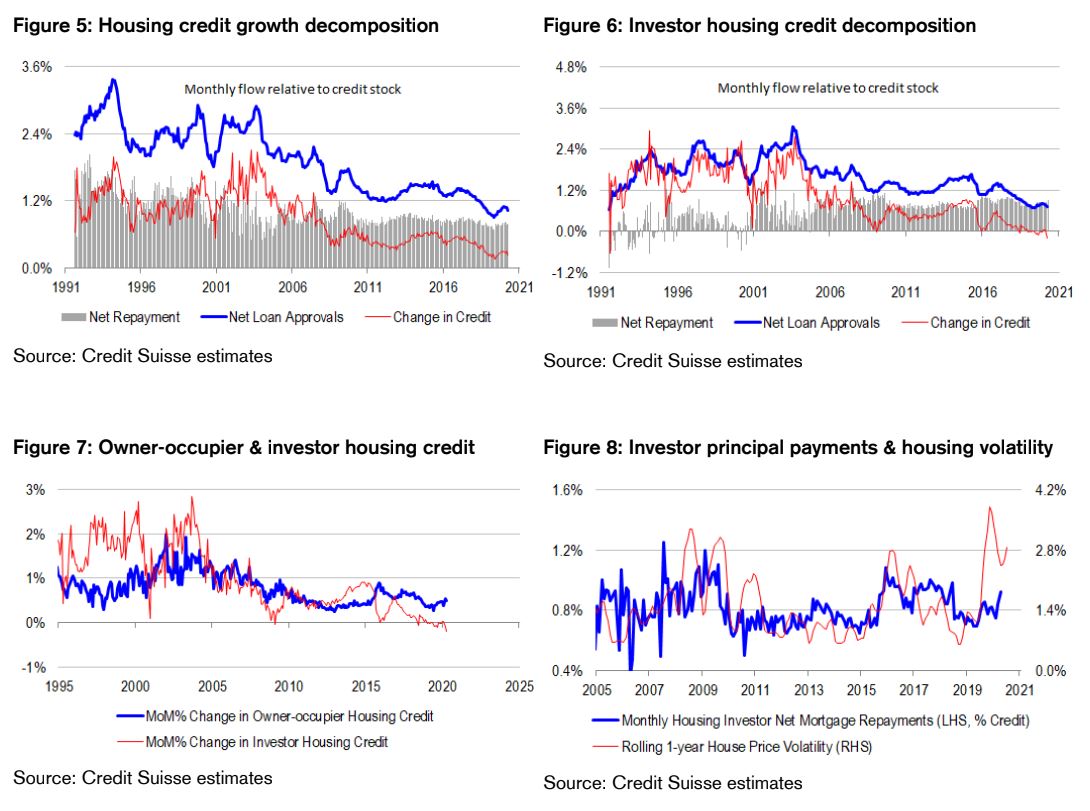

Expect housing investor de-leveraging to continue. We think that house price volatility is likely to rise further in the coming quarters. It is currently elevated and could rise further if our proprietary housing indicator is anything to go by. Indeed, the dispersion within and across components of the indicator is already a red flag. Rising volatility matters for the credit outlook because housing investors are risk parity investors. That is, housing investors pursue an “efficient” form of investing, levering up on their lowest perceived risk asset class to equalize risk contributions across different investments and achieve superior “risk adjusted returns”. And historically, housing looks like the lowest risk asset class. Unsurprisingly then, leverage is greatest on housing. But on the flipside, when the risk profile of housing rises materially beyond what investors initially assumed, they tend to de-risk and de-lever by paying off principal. Indeed, over the past decade or so, there is a remarkably close correlation between the rate of investor mortgage principal repayment and house price volatility. If house price volatility remains elevated or rises further, we can expect to see more aggressive principal repayment from investors, potentially overshadowing the reduction in principal payments from owner-occupiers from debt deferrals and repayment holidays. Worse still, the household saving rate could climb materially a the expense of consumer spending and related job creation. And if all of this occurs, attempts by policy makers to reflate the stock of credit by lowering repayments and incentivizing the banks to run down their capital buffers for the sake of more aggressive loan growth, could backfire. In the circumstances, there are real risks that the private sector credit impulse could flat-line or even turn negative. Therefore, it is imperative for the public sector to do its part in lifting the overall credit impulse through deficit spending. The trouble is that in order to arithmetically generate GDP growth from a starting point of heavy stimulus, the government will need to ramp up deficit spending beyond current levels. Otherwise, we will get fiscal fade and the government will effectively pass the baton of growth back to a potentially struggling private sector. Indeed, this path seems to be getting more likely by the day, with government officials thinking only of running fine-tuning adjustments and limited extensions to stimulus programs, rather than something more comprehensive. Officials seem to be making a little too much of the growth rebound that could come on reopening efforts alone, or staking too much on a cure, vaccine or treatment for COVID-19 being discovered soon. But as they say, hope is not a strategy … And we certainly hope that policy makers are not giving up.

Underweight housing exposures within the equity market. We think that there are still material de-leveraging risks on the horizon, centred on housing. Consequently, the domestic cycle could very easily lag the global cycle. We are underweight residential property developers, homebuilders, discretionary retail and banks within the equity market.

Looks like we’re in for pretty good bust to me:

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.