Unless you want to lose money.

For investors, there is simply no reason to buy and plenty of reasons to sell. Even for first home buyers, there’s no reason to buy and plenty of reasons to rent.

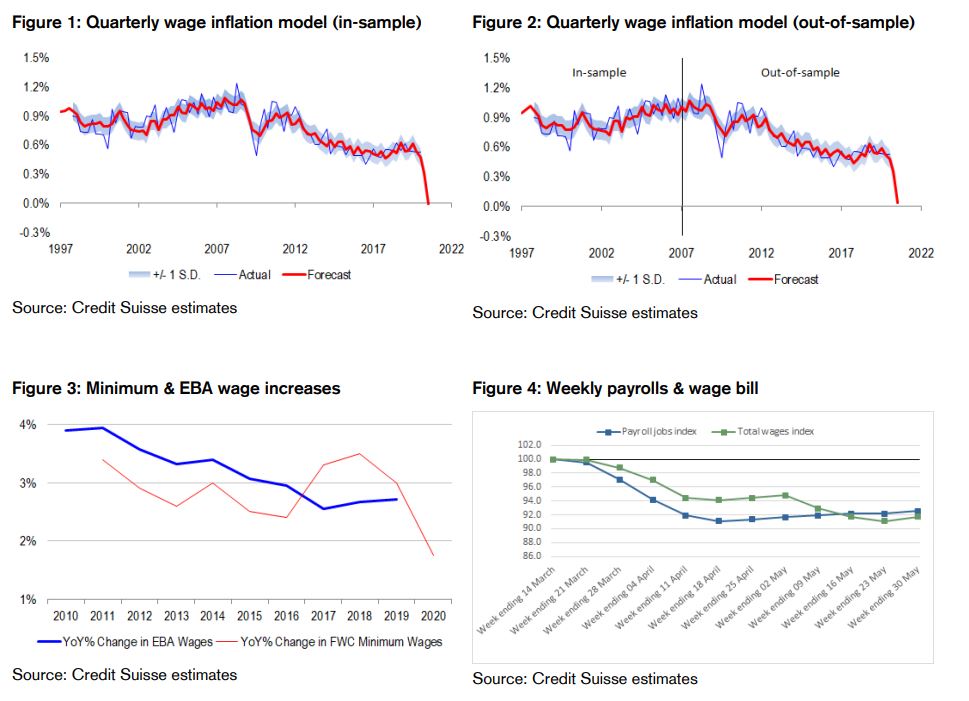

First, there is huge unemployment that is going to be very sticky with unprecedented wage pressures, via Credit Suisse:

Second, there is no immigration and tumbling international students which will prove very difficult to reverse. For instance, the Victorian virus outbreak today is directly the result of quarantine failures around a few hundred people. Imagine what it will be like if we try to bring in hundreds of thousands of migrants from virus-saturated migration growth areas like India, Nepal and LATAM:

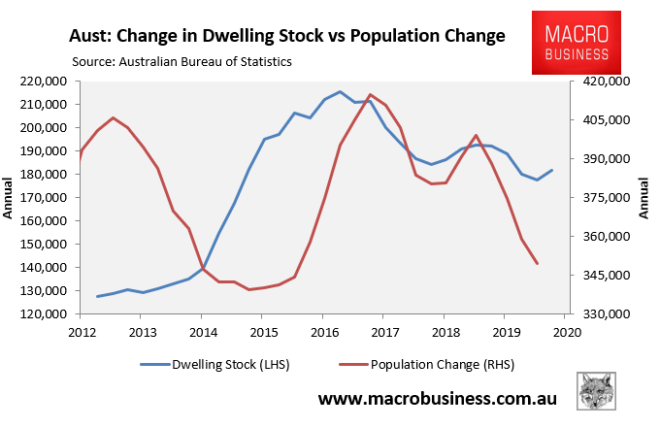

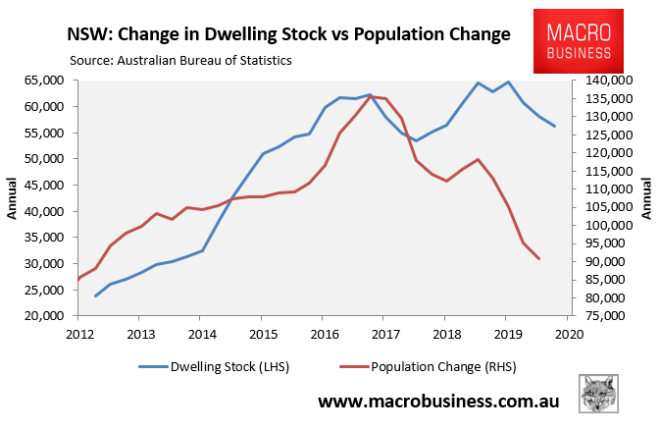

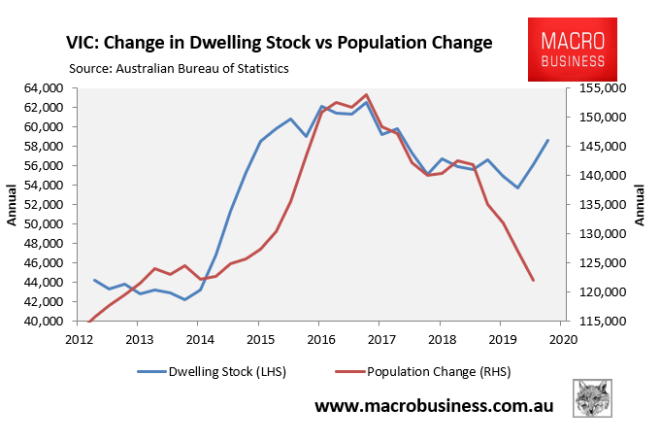

Third, this is leading to huge oversupply of residential property:

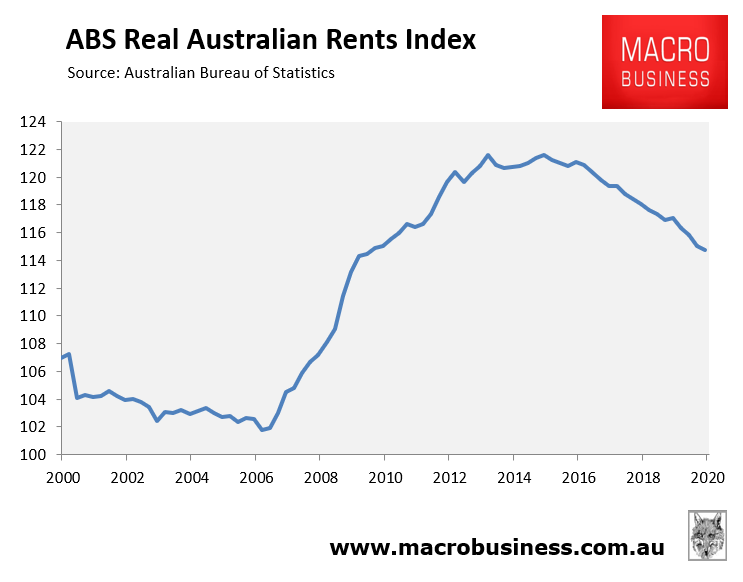

Fourth, tourism is also dead for years, meaning thousands of short terms rentals are now long term, adding to the rental stock and tumbling prices. Rents were already getting blasted for years before COVID-19 and now they are collapsing:

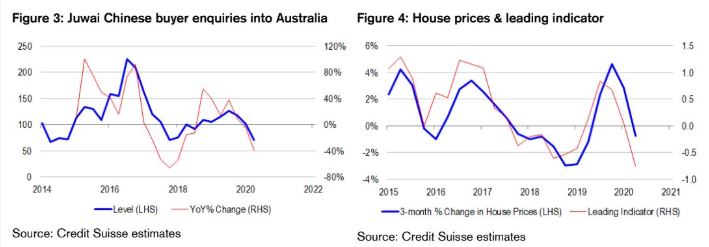

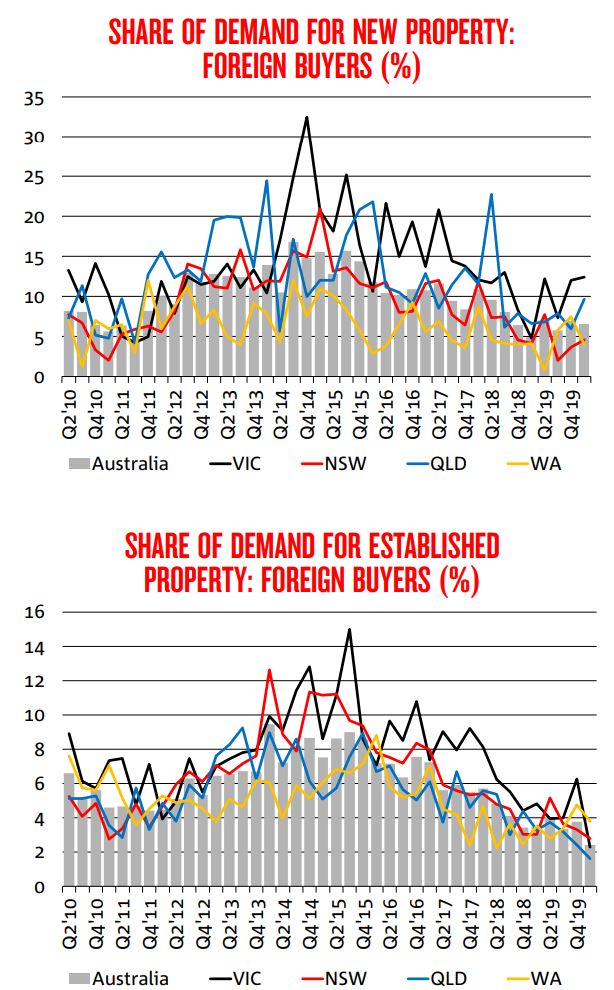

Fifth, Chinese buyers and renters have fled and will not return to anything like previous numbers, if at all, if the CCP has its way. Via Credit Suisse:

Sixth, banks are tightening lending standards and will also soon be forcing stock back onto the market. This was already underway pre-COVID and is worsening now, from the AFR today:

Instances of buyers being asked to justify their recent annual leave and provide pay slips on settlement day to prove they are still employed have been reported in the face of rising unemployment and job uncertainty.

“The income testing is getting harder,” said Sydney buyer’s agent John Carew. “The banks are doing more of a forensic review of pay slips”…

“Pre-COVID, if you were working at an ASX-listed company, that was enough. But now even that is under security,” he said.

The forbearance issue is huge and there are growing reports of multiple property owners being tapped on the shoulder to sell:

Seventh, policy is exhausted. The RBA is out of rate cuts and moving incredibly slowing to unconventional measures. Banks have reduced mortgage rates after the last cuts, certainly, but nothing like enough to offset the above headwinds. A few basis points versus 4.5% during the GFC. Australians now know that the RBA put is dead for housing.

There’s fiscal policy, of course, but it’s already in the market in a big way without doing much. And even an FHB grant on existing property today would do little beyond promoting a little short term activity.

These seven headwinds all hit debt-glutted Australian households that will be forced to deleverage and will want to lift savings structurally higher amid an ongoing COVID-19 shock, intensifying as fiscal supports are removed, at whatever pace.

The jig is up for the Great Australian Property Bubble.

Get out of its way.