Wide ranging discussion in the early June meeting. Based on the conclusion to the statement accompanying the RBA’s June meeting decision, one would have thought that fiscal-monetary co-ordination was an important theme for discussion among board members. But the June meeting minutes revealed very little explicit attention given to the thematic. To the extent that it was an important theme, it was addressed indirectly in the broader discussion about economic prospects. Members talked a lot about improving employment data in May, highlighting the importance of timely stimulus efforts in helping the economy to avoid much deeper contraction. But they were still wary of the risks of housing market deterioration and capex retrenchment outside of mining, noting state government efforts to ease planning restrictions to counter some of the downside. Globally, members seemed to focus on the risks of the Chinese economy undershooting.

“Wall street” versus “Main Street” divergence a focus. Interestingly, RBA board members discussed “the sharp recovery in the prices of risky assets since their lows earlier in the year and whether this was warranted given the large decline in global economic activity and the highly uncertain outlook.” Rarely do Bank officials talk much about equity markets, presumably because housing matters more in Australia as an asset class, especially from a rates perspective. But clearly RBA officials are keeping an eye on bubble risks, in part because they are struggling to reconcile the equity market’s implied views on activity and earnings growth with their own, and in part because they are wary of the risks from heavy-handed central bank intervention in markets. What we are curious about though is whether or not Bank officials explicitly recognise that much of the recovery in equity and fixed income markets has to do with the reflation of passive and risk parity investment bubbles through central bank undertakings to keep rates and volatility lower for longer. Growth is a consequence – not a cause of this process.

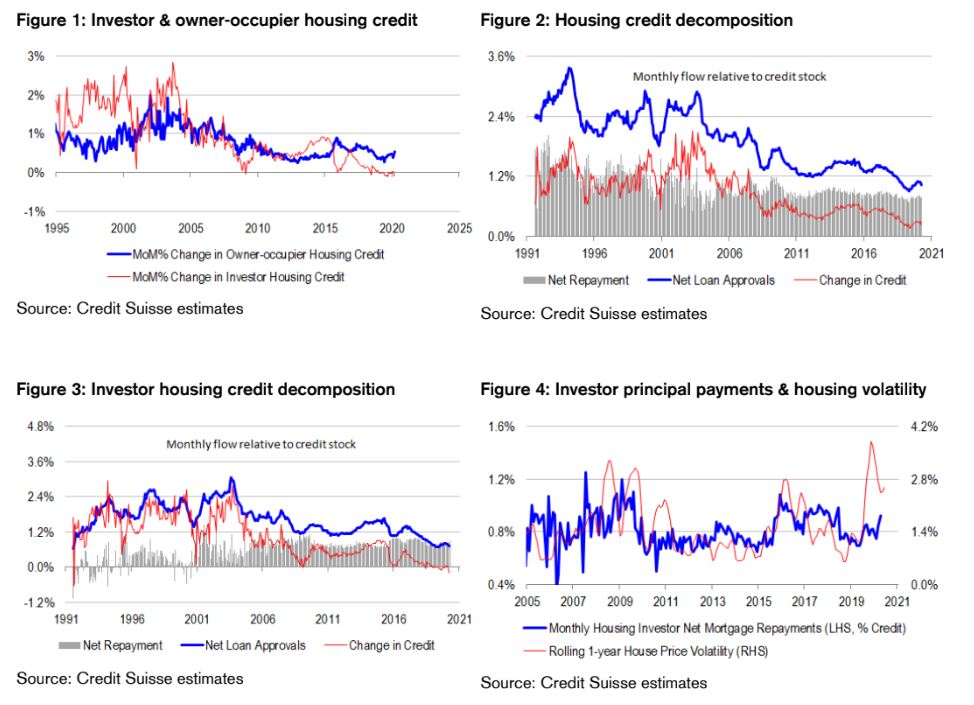

Household de-leveraging a focus. RBA board members made special mention of the fact that mortgage principal payments are on the rise despite debt deferrals being granted by the banks. Officials attributed the increase in repayment activity to precautionary motives, and a lack of opportunity to spend money during the shutdown period. We are encouraged by the fact that the Bank is recognising ongoing de-leveraging and the apparent frustration of attempts to reflate the stock of housing through non-repayment. However, we note that Bank officials did not explicitly split out owner-occupier behaviour from investor behaviour. If they did this, they would see that debt deferrals are actually working to contain owner-occupier principal payments and boost credit growth. But they would also see another risk parity story unfolding – that investors embrace the strategy of levering up on their lowest perceived risk asset class, and are currently getting wrong-footed in their collective assumption that housing is the least risky asset class. With this in mind, it makes sense that investors are de-risking and de-leveraging on their housing portfolios now that housing risk is increasing. The nuance matters a lot in our view, because it helps us to see more sinister and systematic forces at work – not just temporary distortions from the shutdown period. It adds to the case that there is a need for fiscal-monetary co-ordination for an extended period of time, because the private sector is not yet in a position to create money through credit growth, making it imperative for the public sector to fill the void.

Risk parity is the missing thread. The conventional approach to macroeconomic analysis of markets is to start with the view that policy drives economy which in turn drives markets. But we think that it is worthwhile thinking from the opposite perspective – that markets drive economy which in turn drives policy. This is because asset prices are extremely important drivers of developed economy growth via wealth and credit effects. Indeed, asset prices are not targeted in the central bank’s definition of price stability, and are therefore free to roam outside the control box. But we also like the reverse causation perspective, because GDP is a portfolio in as much as a basket of securities is a portfolio, and there are lessons for economists from portfolio theory. Both GDP and financial portfolios require low or negative correlation between constituents to achieve diversification, and avoid large drawdowns. Indeed, this assumption is critical to the proper functioning of passive and risk parity portfolios. But when correlations rise from zero or negative towards one, GDP and financial portfolios become “one-trick” ponies, because everything either rises together or falls together. The chances of boom-bust cycles increase in these circumstances. For this reason, it is very important to recognise what the sources of correlation risk are. Clearly, central bank intervention is an important, driving influence of markets at present, underpinning the RBA’s discussions about frothy equity market valuations. Therefore, we need to carefully understand what the limits of this intervention are. Clearly housing and leverage are still critical drivers of the domestic economy, but are being undermined by the portfolio consequences of high uncertainty. All in all, there is much out of the RBA’s hands here, and we think that the best it can do is not rock the boat by contributing to higher volatility so as to undermine the Australian risk parity trade in housing. And even the RBA’s best may not be enough in the circumstances, creating the need for more fiscal help, because fiscal stimulus creates a short-term, independent or uncorrelated growth driver in the GDP portfolio. But fiscal policy makers are clearly thinking that the mere fact of re-opening the economy will drive sustainable and strong growth, and therefore are only making fine-tuning or targeted adjustments to stimulus. They are not considering the large mathematical fiscal drag on the economy that occurs when stimulus tapers off, because they are assuming that no-one will notice if and when the private sector starts borrowing again. Perhaps this is really the crux of the discussion at the RBA’s June meeting.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.