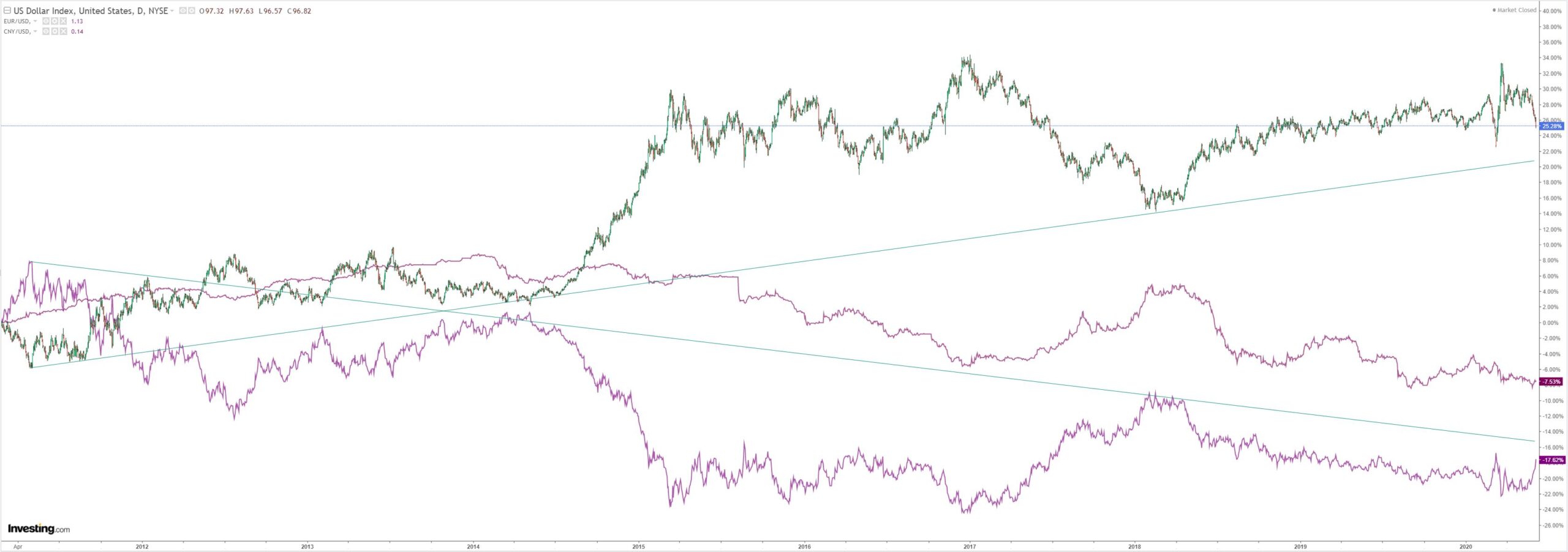

DXY is getting belted now as EUR surges into the Great Fakeflation:

The Australian dollar hit new highs last night before pulling back:

Advertisement

It is murdering EMs:

Gold managed a gain but is still disappointing as DXY falls:

Advertisement

Oil marches on:

Even dirt raised an eyebrow:

Miners blast on:

Advertisement

The EM stock bid stalled:

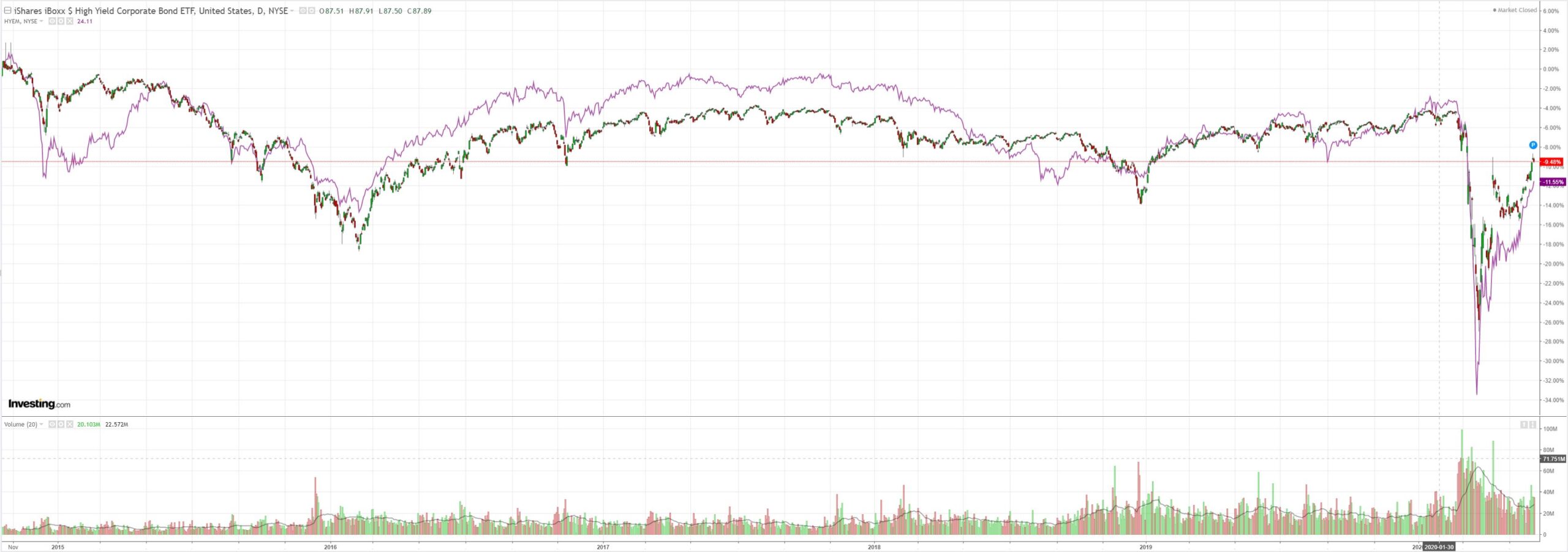

But junk blasted on:

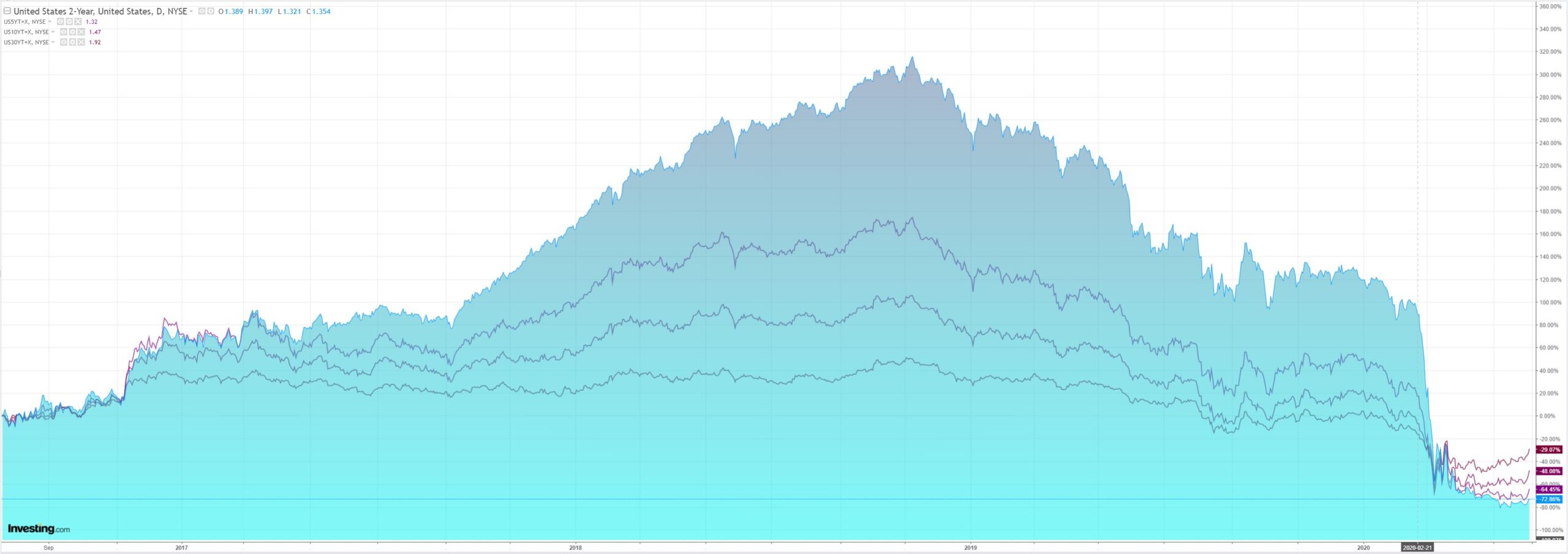

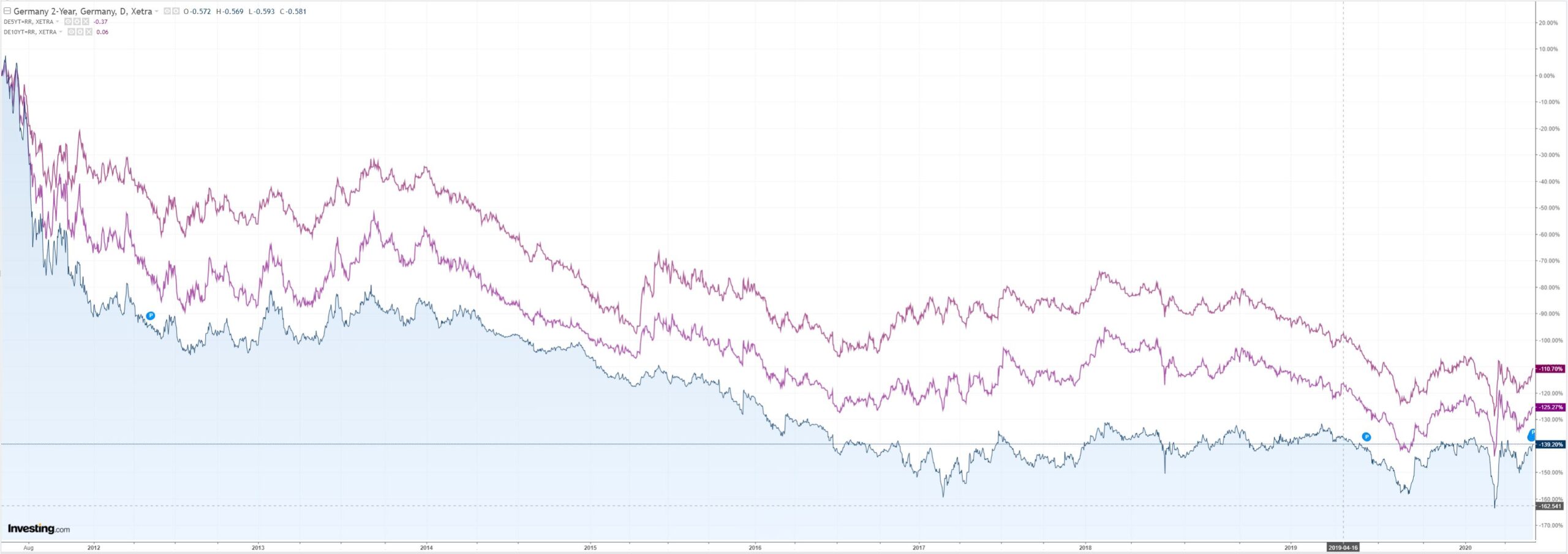

Bonds were all hit:

Advertisement

Stocks fell marginally:

Westpac with the wrap:

Event Wrap

The ECB left its key policy rates unchanged (deposit rate -0.50%) but increased its Pandemic Emergency Purchasing Program (PEPP) by EUR600bn to EUR1.350tr. The increase was larger than market expectations of between EUR250bn and 500bn. It was also extended until “at least” the end of June 2021 and maturing assets would be reinvested until “at least” the end of 2022.

Eurozone April retail sales were not as weak as feared, at -11.7%m/m (vs -15.0% expected).

US weekly jobless claims at 1.877m was close to expectations, although continuing claims at 21.487m were above the 20.0m expected. April trade balance was close to expectations at -USD49.4bn. The widening of the deficit was due to a decline in exports of 20.5%m/m whilst imports declined 13.6%m/m.

Event Outlook

Australia: The AiG Performance of Services index fell to a record low of 27.1 in April. In the May update, the focus will be on signs of recovery as the economy reopens.

US: Westpac (and the median analyst) expects that non-farm payrolls fell by 7500k in May, lifting the unemployment rate to around 20.0%. In this period of heightened labour market volatility, the participation rate will play an important role in determining where the unemployment rate ultimately lands. With rising job losses and increasing spare capacity, May average hourly earnings are expected to slow to 1.0% after April’s spike. Consumer credit data is also released. Credit card debt has plummeted during the lockdown, with consumers being restrained in their ability to spend. The market is looking for a record fall of $20bn in April.

The Great Fakeflation – a three year financial cycle compressed into three months – is now entering its final fantasy. We’ve seen the boom, the bust, the safe haven DXY, the stimulus, the bid for “bargain” stocks, the falling DXY, the run back to EMs, the rotation to value and now, the final convulsion into fantasy, the inflation panic and bond back-up.

Advertisement

Every decent strategist understands this cycle. Indeed, you could write it into an ago, and let it bid each phase. Perhaps that’s what has happened. Via Nomura:

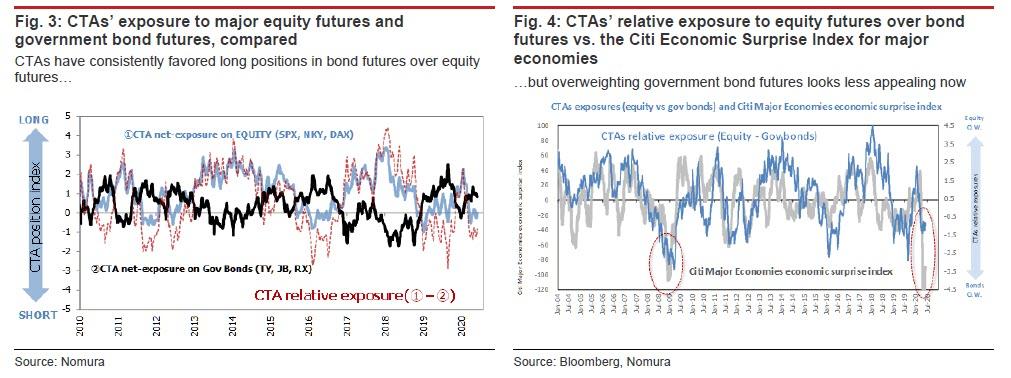

Nomura thinks that it is possible that CTAs (systematic trend-following investors with a top-down perspective) are being pressed into a further portfolio shift away from overweighting bonds towards overweighting equities. For the moment, CTAs’ positions still show a preferential tilt towards long positions in bonds (DM government bond futures). However, the prospect of a bottoming out in the economy (as pointed to by the improvement in the economic surprise index) has probably made bond-buying a less appealing idea from a technical standpoint as well.

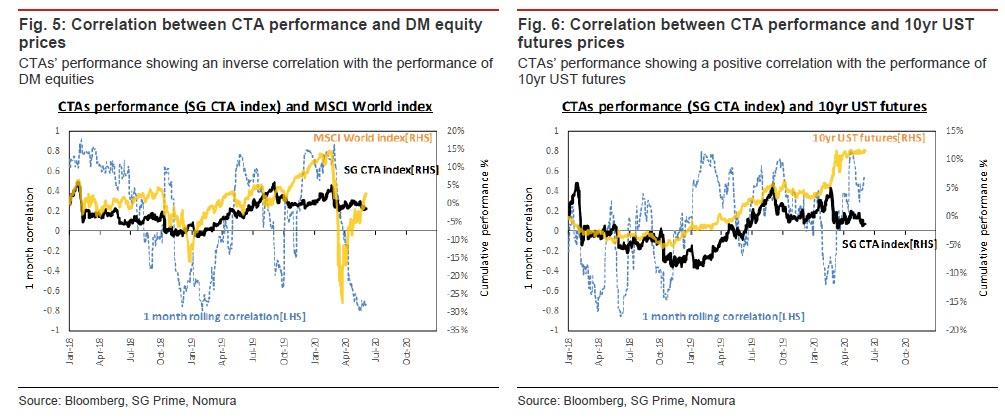

Indeed, if we look at the one-month rolling correlations between actual CTA performance (as measured by the SG CTA Index) on the one hand and stock market or bond market performance on the other, we find that CTA performance has been inversely correlated with the performance of equities (normally an indication of short positions) and positively correlated with the performance of bonds (normally an indication of long positions). If nothing else, this would seem to make it clear that CTAs have been slow to get on board the current equity rally, and that a sell-off in bonds is still the pain side for them.

So at what level do CTAs capitulate on their bond longs and turn short, unleashing a selling cascade?

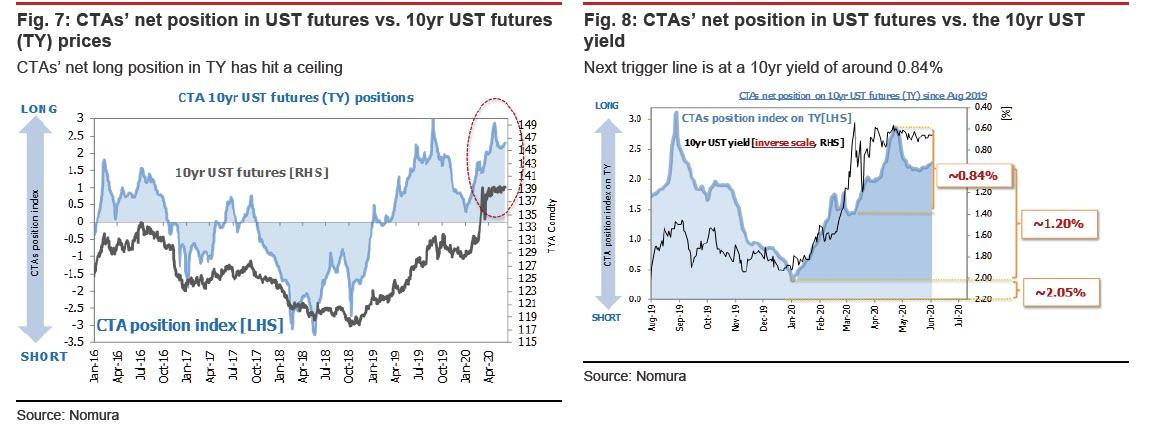

According to Nomura’s CTA position index (representing our estimate of the positioning of CTAs based on real-time data) CTAs to still have a net long position in 10yr UST futures, “although with a conspicuous notch recently where that position appears to have hit a ceiling.” This means that should the pressure created by global macro hedge funds’ sell-off of USTs increase to the point that the 10yr UST yield climbs above the “red line” that exists at around 0.84%, CTAs would likely be drawn into exiting their long positions in TY to cut their losses.

The Great Fakeflation has nothing to do with the underlying economy:

Advertisement

China has barely managed a 90% recovery;

the US isn’t going to get that far as it’s virus fight turns interminable via half lockdowns;

EMs are going into the virus not out of it;

Europe is an export economy leveraged to the above three.

So, what will happen as the Great Fakeflation, processed through the imagination of an algo, comes face to face with reality sometime later this year?

The cycle script typically ends with a bursting asset price bubble as inflation surges into monetary tightening.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.