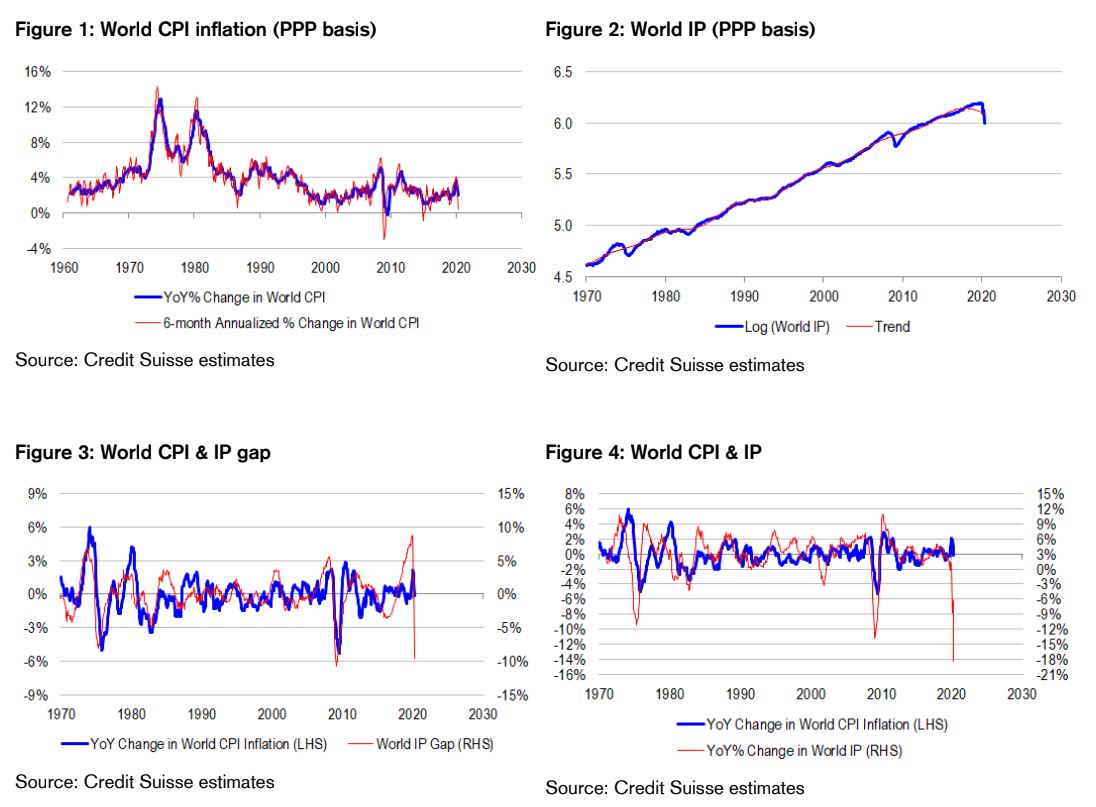

The world is not in deflation despite a sharper recession than the 2008 global financial crisis. In the “Great Moderation” era, economists have used output gaps to understand and predict inflation. Above (below) trend levels of activity, or activity growth, have historically been consistent with accelerating (decelerating) inflation. And over the years, we have seen some very extreme events to stress test the limits of this framework. For example, in the aftermath of the 2008 global financial crisis (GFC), world industrial production (IP), as measured on a purchasing power parity (PPP) basis, shrunk by 14% in the year-to-February 2009. Year-ended world CPI inflation, also measured on a PPP basis to abstract from exchange rate movements, slowed sharply to -0.2% shortly after. In other words, the GFC downturn was so sharp, that the output gap widened significantly, causing the world to enter deflation. However, in the COVID-19 crisis, world IP has shrunk by roughly 20% in the year-to-April 2020—a significantly faster pace of contraction than we saw in the aftermath of the GFC—but yet, world CPI inflation has only slowed to 2%. The COVID-19 crisis, as sharp as it has been, has not been enough to drive the world into deflation. And we do not need much imagination to guess what might happen next to CPI inflation should world IP stabilize or even recover from a low base.

Not a delay—but a structural break. Perhaps we are only seeing a delay rather than a decoupling. Perhaps CPI inflation is about to slow sharply and imminently in response to a negative demand shock. However, we note that even on a 6-month annualized basis, world CPI inflation is not negative. Base effects are unlikely to drive the world into deflation in the coming months. We also note that if we de-trend world IP using a linear filter, to derive an “output gap”, that the trend line dips towards the end of the sample—that is, potential growth turns negative. To be sure, there are notorious real-time estimation problems with output gaps. But this time, if the mathematical filters are wrong, they are wrong because they are greatly overpredicting potential growth, and therefore the size of the gap. Even assuming a small degree of capacity destruction in this crisis, as per our filter, the sheer magnitude of the output gap that has emerged from the downturn cannot be reconciled with stubbornly elevated inflation. This tells us that potential growth is slowing much more rapidly than the eye can see—that this time, the supply shocks from COVID-19 shutdowns and supply chain disruptions are almost equal to the demand shocks from fear and uncertainty. Even attempts to preserve the supply side through debt repayment holidays and additional liquidity are not enough to prevent a demand-to-supply mismatch in the presence of extraordinary demand stimulus working in the opposite direction. This recession is truly different.

Demand is recovering. All of the leading indicators of demand we track—the Institute of Supply Management (ISM) new orders index, US retail sales growth, US loan demand, the Chinese credit impulse, the slope of the world real yield curve and excess liquidity—point to better growth outcomes in the period ahead. Collectively, they either point to less negative growth, or outright positive growth. And if a 20% contraction in world IP is not enough to drive the world into deflation in this cycle, it is not hard to imagine that a pick up in activity growth could drive an acceleration of inflation beyond 2%.

Inflation is not tomorrow’s problem. Many investors are of the view that inflation is only a longer term problem, and that central banks will deliberately fall behind the curve to ensure recovery. After all, there should be no material risk of a wage-price spiral emerging from strong employee bargaining power, especially in such a high unemployment environment, And given central bankers’ sensitivities to a growing laundry list of macro and market factors, it would seem quite unlikely that they would tighten prematurely to deal with longer term inflation risks. But we think that the outlook is far more complicated than what the conventional wisdom would sugest. For starters, we need to ask the reverse question. Rather than ask whether or not inflation will rise to high enough rates to become a threat in the near future, we should ask why inflation is not slowing much in response to the sharpest downturn in the global economy in a generation. In terms of the cost mark up dynamics that drive traditional inflation models, we note that wage inflation is one thing—but productivity growth is quite another. Right now, we are seeing productivity shrink on the back of permanent business closures and supply chain disruptions while wages continue to rise. Therefore, firms are effectively paying workers more to do less. Indeed, it is distinctly possible that these dynamics could persist if longer term, firms look to secure their supply chains by insourcing production activities from abroad, regardless of competitive advantages or disadvantages. Also, firms are likely to try to pass on cost increases from productivity losses, taking advantage of unusual pricing power in a high stimulus environment. After all, money created by large scale fiscal deficit spending ultimately has to go somewhere and mathematically it is likely to show up at some point in inflated corporate profit margins. Turning to the state of play for central banks, we note that most economists are taking the view that policy drives economy which drives markets. But we take the opposite view—that markets drive the economy which in turn drives policy. Our issue is that inflation risk can be priced into bonds even before cash rates rise, and the rise in yields could cause a tightening of financial conditions for asset allocators in light of extremely stretched asset valuations and low expected returns therein. Indeed, there is a risk that with bonds and equities trading on negative risk premia, that the major asset classes could sell off together. Secondly, even if central bankers manage to suppress bond yields and rates volatility near term, they will only succeed in driving down real yields, weakening the USD and driving up commodity prices. In other words, inflation could pick up anyway. We are not necessarily guaranteed high inflation in the period ahead—but we are almost guaranteed high inflation volatility. And history tells us that inflation volatility is a big problem for equity market valuations, especially from such elevated levels.

We prefer a quality overlay, with anti-momentum and anti-value positions as well as some inflation hedges. We understand why equities are rallying near term on re-opening efforts—but nevertheless, we are very wary of a relapse in equities because of stretched valuation and de-leveraging risks therein. We are also wary of the risks of higher inflation and bond yields, as well as the risk that central bankers will try even harder to limit how high bond yields can go in order to prevent a broad-based sell off across asset classes. At an asset allocation level, we see gold and selected commodities dominating bonds across a number of plausible scenarios, especially given that bonds are trading on negative term risk premia, with very little valuation upside. And at a factor level, we want quality and defensiveness—but not the extremely crowded names that would be vulnerable to a passive or risk parity event caused by higher bond yields or higher volatility. We also want to avoid naive value in scenarios where financial markets become disorderly, or the real yield curve flattens. There is a very wide range of scenarios to position for, and most of these will not occur at the same time. We do not have a crystal ball—and so rather than make bold macro calls on how the world will evolve, we instead take refuge in diversification where it is on offer at a reasonable price. For now, we think that long quality, short momentum and short value positioning, combined with an overweight stance on commodities covers the spread of risks while also generating alpha. Within the ASX 200, our comfort in commodities is in the fact that larger capitalization names have strong balance sheets and therefore rank well on quality factors.

I personally think that the risk of an inflation breakout is somewhere infinitesimally above zero.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.