Small housing stimulus package. The Federal government is launching a new $688 million housing stimulus package. Selected owner-occupiers looking to build or renovate in 2H 2020 will be able to get a $25K grant from the government. To be eligible, home buyers need to be owner-occupiers rather than investors. They either need to earn less than $125K per annum individually, or less than $200K per annum as a couple. The grants only apply to new properties worth less than $750K (both land and structure value), or renovations between $150-750K that will not result in the property being worth more than $1.5 million. Compared with earlier headlines suggesting a package of $1 billion or more, with wider eligibility, we think that the housing stimulus package is disappointingly small. Even annualizing the impact on 2H (the window for the program), we only arrive at stimulus worth less than 0.1% of GDP. That said, we also think that the governnment is willing to announce more stimulus measures should they be required, although not necessarily in housing.

Home renovation spending follows the cycle in house prices. Private home renovations make up 38% of residential investment, and 1.9% of GDP. They typically follow house prices with a lead time of a quarter or so. In other words, households see incentives to upgrade their existing homes rather than buy new homes when they see housing becoming more expensive. Given small share of GDP, and now falling house prices, any stimulus package targeting this space needs to be big to cause a large delta in spending and meaningful contribution to GDP growth. But we doubt that the incentives delivered are large enough, nor the eligibility criteria wide enough to really move the needle on this front.

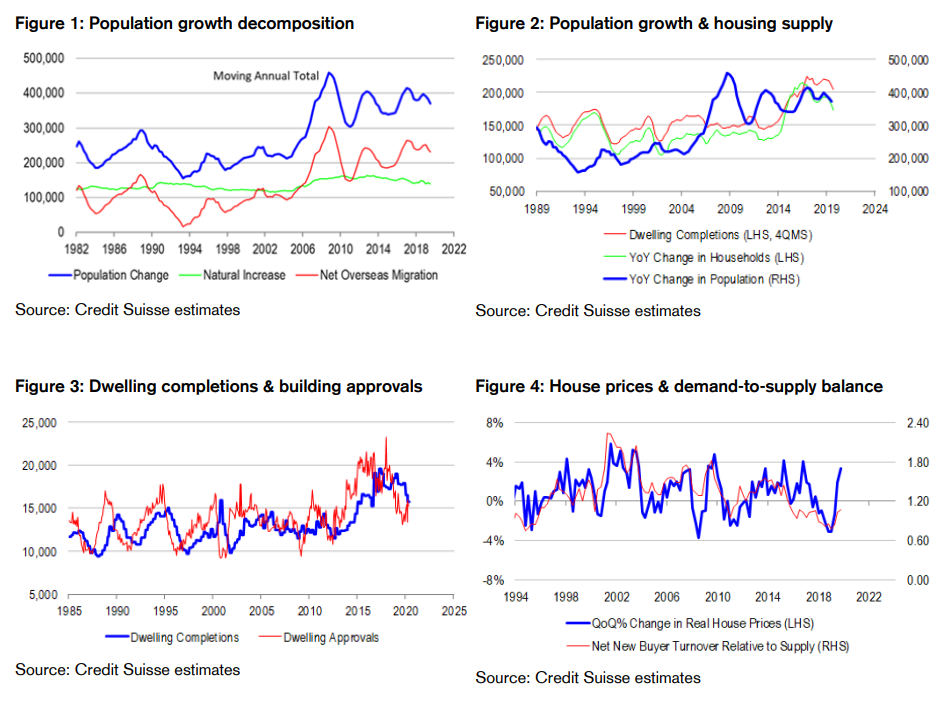

Very little chance of local buyers completely making up for the shortfall in foreign demand. The lion’s share of Australia’s population growth comes from immigration. Without immigration, 2019 population growth would have been 0.6% – not 1.5%. And while the pace of natural increase is solid by international standards, it is not enough to stave off population ageing. Indeed, even migration cannot do this in the medium term. COVID-19 “soft” border closures are likely to significantly curtail population growth and household formation. For example, if the government’s projections are right, and immigration falls by 85% in the next year, underlying housing demand could potentially fall below 100K per annum, compared with the current dwelling completions of 190K and the annualized level building approvals of 180K. The housing market would become materially oversupplied in a very short space of time. Indeed, the demand shock from much lower population growth would be so large, that it would be difficult to offset it with local demand by boosting housing affordability. History tells us that the conversion ratio population growth to net new local buyers (investors and first home-buyers) is a one-to-one function of housing affordability (on a principal plus interest cover basis), adjusted for population ageing … but from 5 years ago! It is very difficult to instantaneously improve housing demand by changing affordability conditions a little. The biggest and quickest delta is in population growth. We recognize that many readers will find our findings counterintuitive, because we have seen housing booms recently corresponding with adjustments to home-buying incentives. But we must be careful not to become to univariate in our recollections of history – there are, and have been many moving parts to the housing equation.

Why does it take so long for locals to respond to affordability? Like the case in most other asset classes, valuation is a key driver of expected returns in housing. High (low) affordability today should correspond to high (low) house price gains in the future. Indeed standard affordability metrics, adjusting for population ageing and structural fading of housing demand therein, are able to predict 10-year ahead house price movements with reasonably accuracy but for the most recent period driven by global, rather than local factors. From an investment signal perspective, the important difference in housing, compared with other asset classes, is that momentum is a much more critical driver of behaviour, specifically for investors. If we combine this trend following behaviour with a more forward-looking approach based on affordability, we get a blended measure of expected returns that looks surprisingly like … housing affordability from 5 years ago. Effectively, the historical relationships suggest that it is investor inertia which drives the long lead time from housing affordability to net new buying, abstracting for a moment from population growth. And the experience of the past decade has been very mixed for investors – a Chinese and credit driven boom followed by sharp declines due to the drying up of Chinese inflows, macro-prudential tightening and more recently, border closures as well as rental freezes. With all of this in mind, investors need some encouragement to wipe their memories clean of volatility, and to get their interest up again. They will need a lot of encouragement to take the mantle from missing foreign buyers and make up for an ageing population. The Reserve Bank of Australia (RBA) cannot do much more to help at the effective zero bound on rates, leaving responsibility on the government’s shoulders. And we think that what is being delivered by the government falls well short of what is required, and perhaps was always bound to.

Policy makers either recognize they cannot help much without opening the borders, or do not recognize the scale of the problem at hand. The small housing stimulus package either represents a smart concession, a difficult compromise, misunderstanding, or a failure to appreciate the coming shock. Fiscal policy makers could be recognizing that there is not much they can do to lift housing demand without opening the borders in earnest. They could be heeding advice from years past that the goal is to create jobs rather than asset price bubbles and debt sustainability issues. The Liberal National Party (LNP) could be pre-empting overspending claims that have haunted past governments post counter-cyclical stimulus, by switching quickly back to an austerity ideology. Indeed, the recent insistence of the LNP in New South Wales (NSW) on public servant wage freezes to create budget for spending elsewhere in the system, to us smacks of the myth that the government is funding constrained when the reality for the state government is quite different because of RBA quantitative easing (QE). A final possibility is that policy makers could simply be unaware of how sharp the decline in housing could be from lower migration, hoping that the shock proves temporary and that the private sector will adjust accordingly. Regardless, the housing stimulus package is cold comfort for housing, consumer and banking sectors, and suggests to us that the government is banking heavily on sharp recovery from re-opening efforts alone. All of this is a risky proposition in our view. In the first place, virus curves are only flattening because of the shutdown restrictions in place – it is an unknown what they would do when the restrictions are lifted, especially without a cure, treatment or vaccine. Secondly, it is too much to ask of housing vendors to do all the adjustment for the housing market to restrict supply during the soft border closure phase. The issue is not so much falling house prices that we worry about – but the potentially non-linear effects of rising housing uncertainty on consumers and housing investors and de-leveraging risks therein. Compounding the problem of de-leveraging risk is fiscal fade once the economy goes past peak stimulus. Sustained fiscal stimulus for an extended period, in “coordination” with the RBA is critical. Within the government’s ideology, it seems to us that if such stimulus is going to happen, it will be in reaction to disappointments in the recovery phase or new shocks, and will most likely be delivered via infrastructure spending.

Small indeed. Obviously the Government does not feel it can boost house prices directly any more so it will opt for lower building and rebooted immigration instead.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.