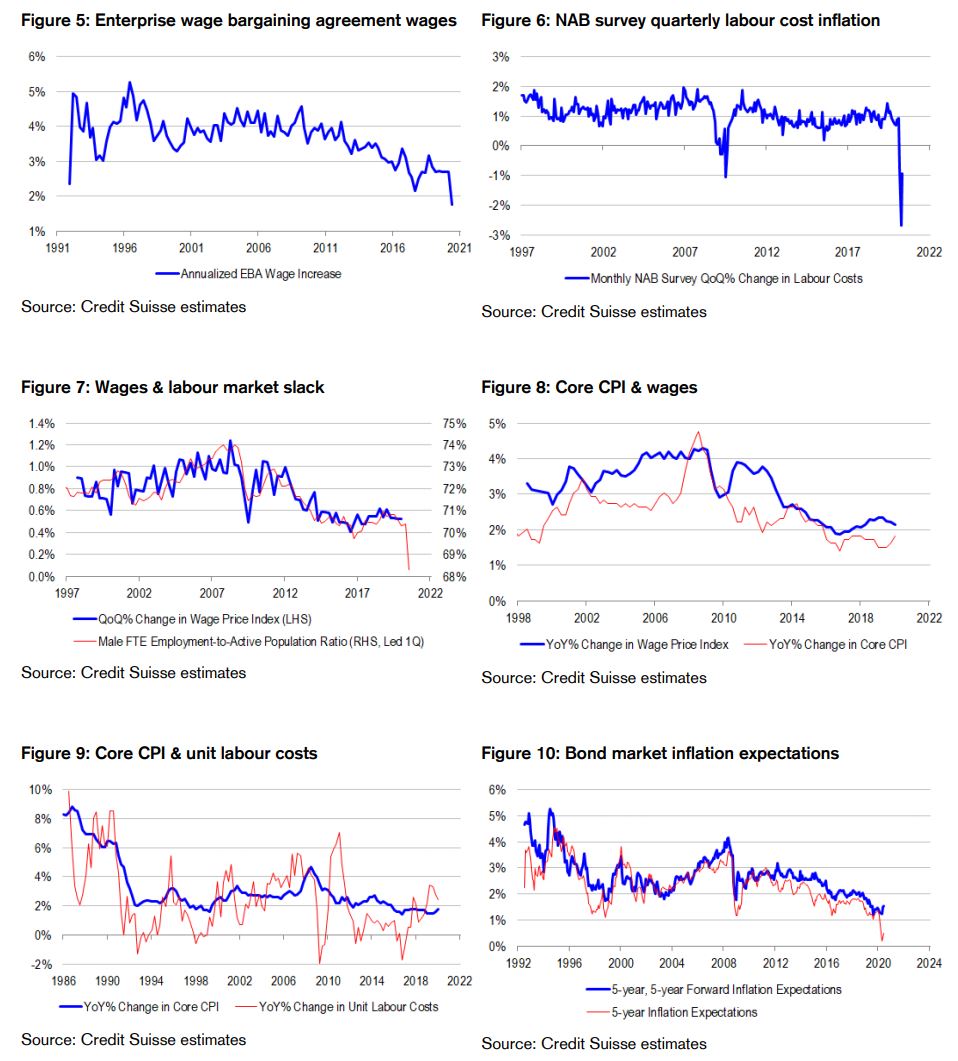

Extraordinary slack in the labour market. The unemployment rate has risen to 7.1% over the past few months, its highest level since October 2001. But the rate would have been much higher, closer to 10%, if not for a very sharp decline in the labour force participation rate. Our preferred cyclical measure of labour market slack, based on male full-time equivalent employment as a share of the “active” labour force (an average of the civilian population and the official labour force), has been designed to abstract from the long-term positive influence of women on the workforce and to limit the effects of cyclical participation swings. It has fallen to all-time historical lows. An unprecedented amount of slack in the labour market has emerged, severely undermining wage bargaining power and job security.

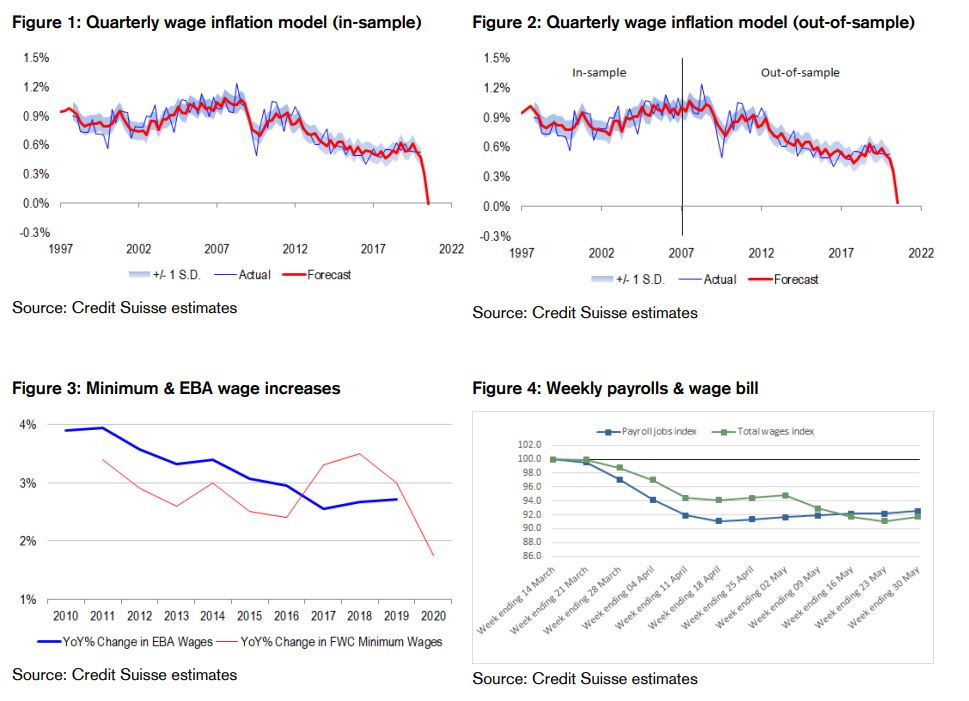

Fair Work Commission raises minimum wages by only 1.7% in financial year 2021. Recently, the Fair Work Commission (FWC) has announced that minimum wages will rise by 1.7% in the financial year (FY) 2021. Importantly, increases will be staggered over the next year, with 25% of award-reliant workers benefiting from the first tranche from 1 July, 40% of workers in the second tranche and the remainder in the final tranche. The announcement covers roughly 2.2 million Australians who are paid the minimum or who have their pay set by awards that rise in line with FWC decisions. The FY21 announcement represents the slowest pace of mandated wage inflation since the FWC started setting wages in 2010. It is an attempt to balance calls from the business lobby for wage freezes to “help workers find other jobs” during the shutdown phase, with calls from employee advocates for a 4% increase to help struggling households with the cost of living. Historically, FWC minimum wage increases are reasonably highly correlated with wage claims in Enterprise Bargaining Agreements (EBAs). But interestingly, we note that EBA wage increases have been undershooting FWC minimum wage increases in recent years. And we expect more of the same in FY21 given that minimum wage increases are quite staggered.

Business surveys point to ongoing shrinkage in labour costs. The National Australia Bank (NAB) business survey tells us that quarterly labour costs shrunk in the quarter-to-May by 0.9%, following a much larger decline in April of 2.7%. The shutdown period represents the first time since the 2008 global financial crisis (GFC) that labour costs have fallen, and the first time in history that they have fallen by more than 1% over a 3-month period. The good news is that perhaps the economy is starting to bottom out, consistent with a less negative outlook for employment and wages going forward. Indeed, high frequency payrolls and wages data that the Australian Bureau of Statistics (ABS) is publishing during the shutdown phase, points to sharp wage bill declines recently – but also to a tentative bottoming out process as the economy re-opens. The bad news is that wages and employment are falling in the presence of the government’s “Job Keeper” program, which incidentally is due to expire in September. One possibility is that government payments are directly dampening measured labour costs to the extent that they are set below what workers would normally earn. Another, more worrying possibility is that not enough businesses are getting access to the program, contributing to wage suppression via higher unemployment. Something is better than nothing to be sure – but post-September, the risk is that payments roll off, and everyone faces the darker reality of the economy in a COVID-19 world without the masking or smoothing effects of fiscal stimulus.

Proprietary wage tracker indicates decline in wages ahead. Our proprietary wage tracker uses the most timely available partial indicators to “now-cast” and even predict quarterly inflation in the official wage price index. It is based on our preferred cyclical measure of labour market slack, EBA wage claims and labour cost inflation reported in the NAB business survey. The model explains roughly 76% of the forward variation in the wage price index since its inception in 1997. Importantly, its parameters are quite robust and stable through time, giving us confidence that our modeling framework does not overfit the data, and is reliable for use in forecasting. Model stability matters a lot to us at the best of times, but especially in the context of wages because official models have consistently and badly over-predicted wage inflation over the past decade. If we take the recently announced FWC minimum wage increase as a proxy for EBA wage claims (an optimistic assumption in our view), and also account for the latest NAB business survey and labour market data for May, our wage tracker would point to slightly negative wage inflation in the quarter ahead – a first in Australian history. To be sure, there are episodes in history when we have seen negative quarterly prints for growth in average earnings – but each of these occasions have resulted largely from factors not controlled for in the “average” measure such as changes in hours worked per person, or sample compositional shifts across different types of work with different pay grades. Indeed, we are currently seeing how large some of these distortions can be in the US data, but on the upside as low-income workers drop out of the sample. In contrast, the wage price index has been designed to be quality and compositionally adjusted, making negative readings a very big deal.

Core CPI inflation likely to slow. It remains to be seen whether or not Australians are willing to take pay cuts, even on a temporary basis. But nevertheless, there is a very sharp slowing in wage inflation in the offering. Wages are a component of unit labour costs, and unit labour costs are a key driver of CPI. There are a number of reasons why wages and CPI inflation are not always aligned through time. But notwithstanding these, history tells us that whenever wage inflation slows below the pace of core CPI inflation, that core CPI inflation always subsequently slows. Part of the reason why is that negative real wages growth undermines consumer spending which in turn weakens corporate pricing power. Similarly, high uncertainty accompanying softness in wages and income insecurity can weigh on consumer spending in such a leveraged environment. Given the sharp slowing in train for wage inflation, and the currently “elevated” starting point for core CPI inflation of 1.8%, we expect to see core inflation decelerate meaningfully in the short term. Longer term, much of the inflation outlook hangs on how much the output gap closes, whether through demand recovery or supply side destruction, and currency.

Tricky inflation pricing in bonds. The disinflationary view is hardly contrarian. At time of writing, bonds are discounting 0.5% annualized inflation on a 5-year horizon, and 1% annualized inflation on a 10-year horizon. 5-year, 5-year forward break-even inflation expectations, a proxy for the Reserve Bank of Australia’s (RBA’s) inflation targeting credibility, are running at 1.5%. No-one believes that the RBA will hit its 2-3% inflation target any time soon, or even longer-term. Therefore, it is hard to profit from a disinflationary view in the bond market, because bonds are already priced for very weak outcomes. We are more focused on the prospect of increased volatility in rates and inflation dynamics, as some parts of domestic demand recover on re-opening efforts, housing suffers from low migration, fiscal stimulus fades and supply shrinks on permanent business closures and supply chain disruptions. We also have concerns about the RBA’s ability to smooth this all out by “merely” using forward guidance, quantitative easing (QE) and yield curve control. To be sure, policy makers could spin the rhetoric of “good luck, and good management” again, like they did during the GFC. The different moving parts to the growth and inflation equations could magically cancel themselves out with a bit of help. But given how large the forces at work are, and prevailing high levels of uncertainty in the private sector (and indeed, within the RBA itself), we are not so optimistic.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.