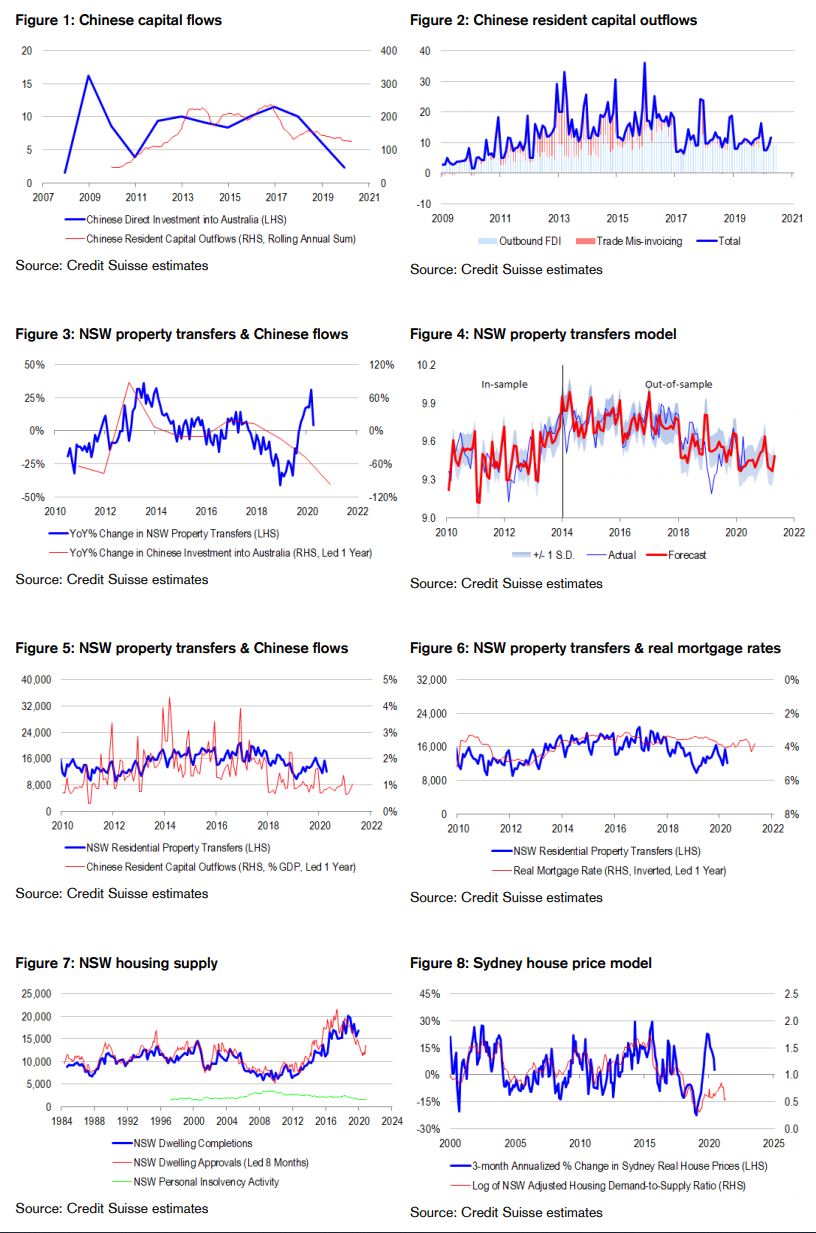

Chinese non-residential capital inflows into Australia have been on the decline. Since 2011, Klynveld Peat Marwick Goerdeler (KPMG) and the University of Sydney Business School have published estimates of Chinese investment into Australia. Their estimates cover investments made by Chinese entities, as well as their subsidiaries and special purpose vehicles in Hong Kong and Singapore, in Australia through mergers and acquisitions, joint ventures, and greenfield projects, excluding residential properties. Their data have been derived from a wide range of public sources including commercial databases, corporate information and official Australian and Chinese agencies such as the Australian Bureau of Statistics (ABS), the Foreign Investment Review Board (FIRB) and Ministry of Commerce of the People’s Republic of China (MOFCOM). Importantly, the data have been verified and synthesized on consistent bases. The latest report has highlighted three consecutive years of sharp decline in Chinese flows into Australia to $3.4 billion (0.2% of GDP) in 2019 from $15.7 billion (0.9% of GDP) in 2016.

Australian and global measures of Chinese flows are highly correlated. The KPMG and University of Sydney series of Chinese flows into Australia is highly correlated with our preferred global measure of Chinese resident capital outflows based on outward direct investment (ODI) and trade misinvoicing. We traditionally focus on gross Chinese resident capital outflows, rather than net capital flows from the balance of payments, because there are very large portfolio allocation differences between the funds that Chinese push out to the rest of the world versus the funds that foreigners pull out. Combining the different data sets, it appears that Australia’s share of global flows has declined dramatically over the years to only 1.9% in 2019 from 7.1% in 2017.

Chinese resident capital outflows have been a powerful leading indicator of Australian housing demand. In principle, Chinese ODI data should not tell us much about Chinese demand for Australian residential property. However, we have found that since the inception of the official Chinese ODI series in 2009, that roughly 60% of the cycle in New South Wales (NSW) housing turnover can be explained and indeed, predicted by Chinese resident capital outflows to the rest of the world and Australian real mortgage rates. Stronger (weaker) Chinese flows, and lower (higher) real mortgage rates have typically foreshadowed stronger (weaker) NSW home sales in the following year. Somehow, Chinese ODI flows have been highly correlated with Chinese demand for Australian property, whether because of spill over effects, or common decision making processes. Importantly, the mapping of Chinese flows and real mortgage rates to housing turnover has proven remarkably stable in- and out-of-sample, giving us confidence in our model’s suitability for forecasting. To be sure, there have been periods where actual turnover has materially diverged from our model’s predictions. For example, during 2018-19, housing turnover significantly undershot the level foreshadowed by Chinese flows and real mortgage rates. However, the undershooting occured after a period of overshooting from 2017 to early 2018, and subsequently corrected in late 2019. In other words, Chinese flows and real mortgage rates have been useful longer-term anchors for housing turnover, even during periods of over- and under-shooting. We suspect that idiosyncratic factors we have not been able to capture well in our model, such as Australia’s shifting popularity as a destination for Chinese investors, and the Australian election cycle have contributed to over- and undershoots in recent years.

Chinese flows could now be stabilizing, putting a floor beneath housing demand but not necessarily prices. The KPMG and University of Sydney series of Chinese investment into Australia suggests that Chinese interest has been weakening, boding poorly for anyone looking to sell assets to Chinese residents at the turn of the year. However, our preferred measure of Chinese resident capital outflows, current as of April 2020, is suggesting that global flows may actually be in the process of stabilizing. And if our model is any guide, this should be consistent with Sydney housing turnover stabilizing as well in the year ahead, but for shifts in the city’s popularity as a destination for Chinese investors. The trouble is that even if Chinese demand stabilizes, it will only be at levels consistent with flat Sydney housing market turnover in the period ahead. And current levels of housing demand are not sufficient to absorb new supply. Therefore, stabilization in Chinese flows is unlikely to put a floor beneath house prices over the next year, even if it does put a floor beneath turnover. Also, we need to consider that soft border closures and geo-political tensions could limit Chinese interest in Australian capital cities, causing undershooting in demand relative to our model.

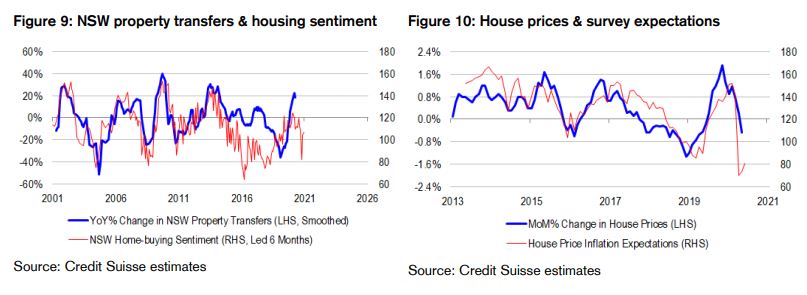

Surveys suggest that locals are more positive on affordability, but not house price inflation. Recent consumer sentiment surveys tell us a story very consistent with the evolution of Chinese capital flows. Surveys suggest that homebuyers feel a lot more confident that now is a good time to buy than a few months ago. But even after the bounce, prevailing levels of homebuying sentiment are not historically consistent with growth in housing turnover – only stabilization. Also, while more homebuyers are thinking that now is a good time to buy, consumers generally do not expect house prices to rise in the period ahead. House price inflation expectations are not recovering with homebuying sentiment, and currently sit at levels historically consistent with house prices falling quite sharply. In our view, the general public is aware that slower migration and heavy supply of new builds are likely to keep the housing demand-to-supply balance in oversupply territory for quite some time. Moreover, fiscal and monetary policy makers are either unwilling or unable to fill in the void.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.