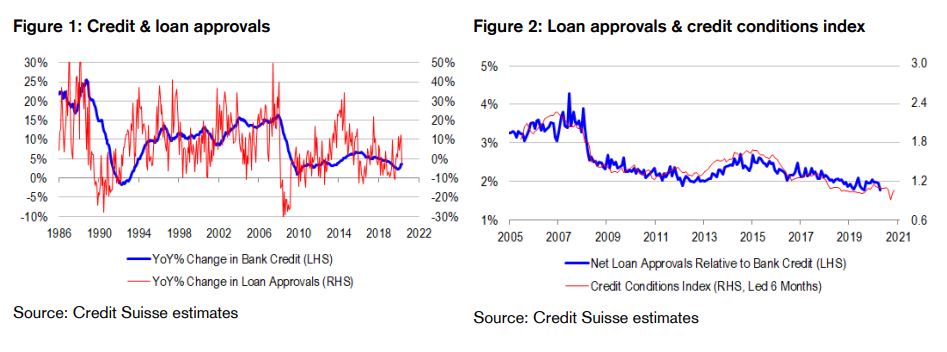

Loan demand plunges in April. Loan approvals fell sharply by 9.2% in April, taking year-ended growth lower to -2.9% from 12.6%. Compositionally, weakness was broadly based across lending categories, with particularly sharp falls in personal and business construction loans. Worse still, the Australian Bureau of Statistics (ABS) believes that loan application backlogs from March spilled over into April, making the April data look a lot better than it actually was. Clearly, COVID-19 shutdowns and related tightening of credit conditions have had negative effects on credit creation.

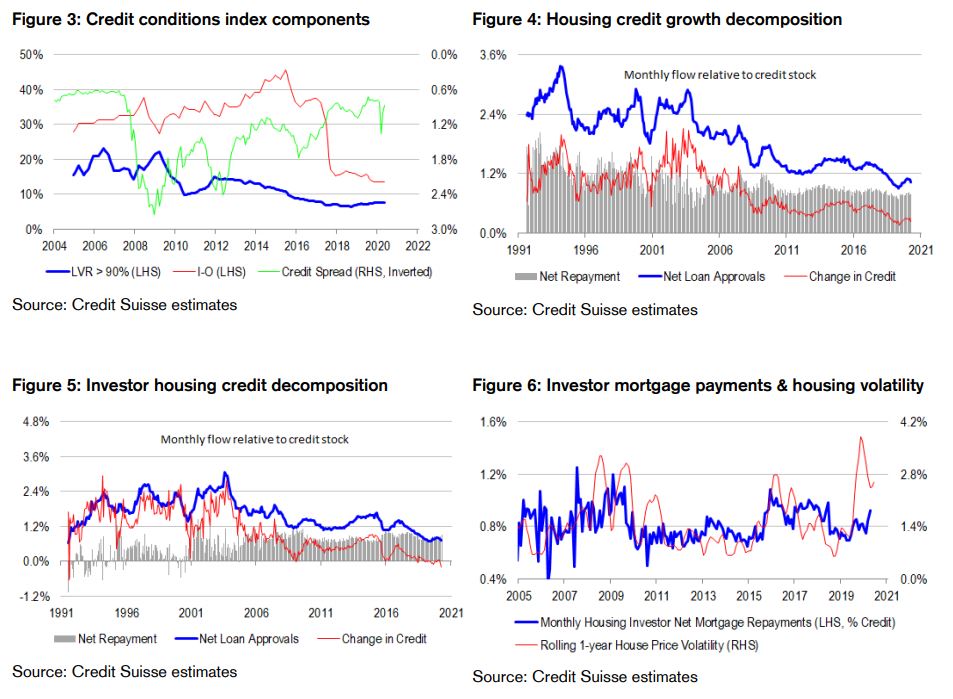

Weakness in loan demand foreshadowed by tighter credit conditions. Weakness in loan demand does not surprise us, because leading indicators have foreshadowed this outcome some time ago. Our proprietary credit conditions index (CCI) is based on banks’ willingness to lend on interest-only terms, banks’ willingness to lend to high loan-to-value ratio (LVR) customers, and inverted credit spreads as a proxy for the easiness of corporate lending conditions. The CCI leads loan approvals (expressed as a share of credit) by several quarters. Over the past few months, the CCI has headed lower on the back of tightening corporate credit conditions, and stagnant mortgage lending standards. Only very recently has it started to recover on the back of central bank quantitative easing (QE) efforts causing credit spreads to narrow. But overall, the CCI has evolved in such a way that it has pointed to loan demand weakening further before stabilizing. And the loan approvals data has indeed been following this forecast trajectory.

Bank credit growth is likely to slow. Historically, the cycle in loan approvals leads the cycle in credit growth, because movements in flows tend to lead movements in the stock. And now that loan approvals are falling, it is only a matter of time before the back book of loans catches down too. Indeed, credit growth is already slowing sharply in monthly sequential terms, as drawdowns on credit lines peak, and true weakness in marginal loan demand starts to surface.

More evidence of housing investor de-leveraging offsetting owner-occupier repayment holidays. New loans are not the only driver of credit growth – repayment activity matters a lot too. By definition, credit growth should equal new loans written net of refinancing activity and repayments. Applying this definition to housing credit, we note that overall net principal repayments are little changed from previous months. However, the lack of change masks some very divergent trends among the components. Owner-occupier net repayments are declining, reflecting applications for debt repayment holidays from the banks. But investor net repayments are increasing, reflecting the desire for leveraged “risk parity” investors to de-risk and de-lever now that they are being wrong footed on the rising risk profile of housing. Indeed, the evidence is that the de-leveraging behaviour of investors is overshadowing the non-repayment activity of owner-occupiers. In other words, housing credit growth is slowing despite the best of efforts from policy makers and banks to reflate the stock of credit through non-repayment and deferrals.

Overall credit impulse could slow sharply. We are concerned that by the time we see bank credit growth slow in earnest, that fiscal policy makers will already be thinking about paring back stimulus. There is a material risk that the economy’s overall credit impulse will fade quite rapidly in 2H, weighing on the domestic recovery.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.