CoreLogic’s head of research, Eliza Owen, believes that high unemployment and falling incomes presents clear downside risks for the Australian property market. And unlike previous episodes, the market will not be saved by falling interest rates this time around:

Comprehensive coverage of labour markets from the ABS highlights sobering headwinds for the property market. Job and income levels are likely to remain subdued as mortgage holidays expire and stimulus measures are wound back. Rental markets are expected to be particularly dampened by disproportionate job losses among young people, and those working in tourism, hospitality and the arts…

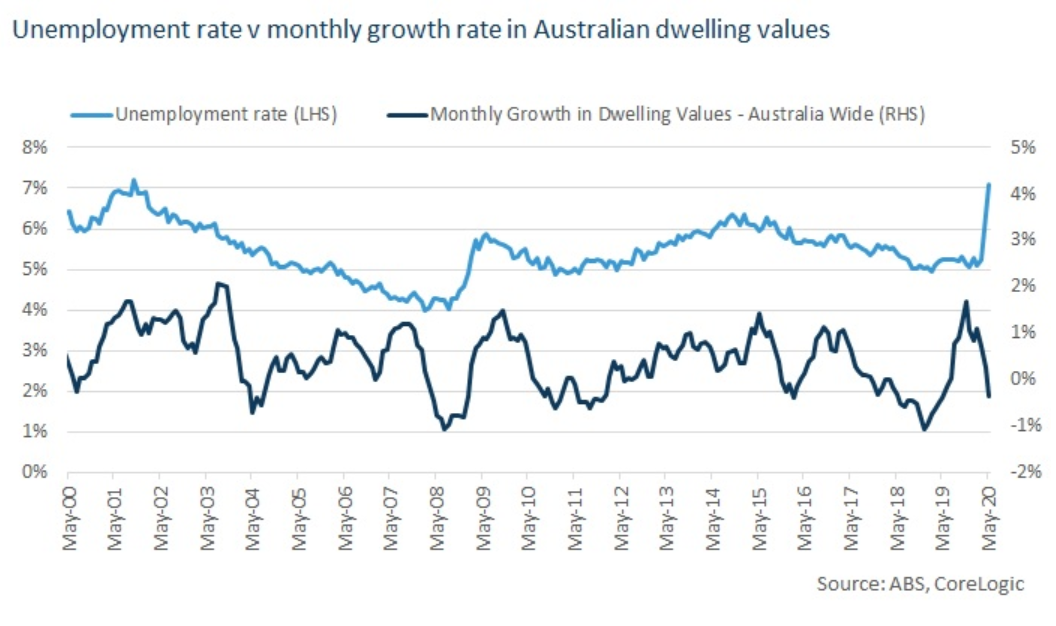

Historically, increases in the unemployment rate have not necessarily led to house price falls. In fact, the opposite had been the case. The unemployment rate and the monthly growth rate in Australian dwellings have been moderately, positively correlated at about 0.5 for the past two decades. This means housing growth rates have fallen when unemployment has fallen, and housing growth rates have risen in times when unemployment has risen.

While this may seem counter-intuitive, it is not uncommon for some housing markets to perform well when unemployment rises. That is because when unemployment surges and the economy weakens, the monetary response has been to lower the cash rate. The cheaper cost of debt actually creates growth in housing for those who can still afford to buy.

The chart below shows the monthly unemployment rate against the monthly growth rate in national dwelling values.

However, data over May shows the historic relationship between the unemployment rate and housing market performance has deteriorated. As the unemployment rate hit its highest level in almost two decades, the monthly change in housing values was negative. This is despite the cash rate reaching a record low, and RBA data suggesting average new mortgage rates were just 2.8% for owner occupiers, and 3.2% for investors over April.

This may be a function of unemployment being too widespread to enable low interest rates to stimulate housing market conditions. Another contributing factor could be a shift in investor expectations; with falling cash rates a major contributor to future capital growth, housing assets may be less appealing to investors as the cash rate hits a record low.

Another important implication from the back series of the unemployment rate is to note how relatively high levels of unemployment were sustained after the Global Financial Crisis in 2008, rather than unemployment returning to pre-GFC levels.

As with the GFC, structural changes in the economy amid COVID-19 are likely to see the unemployment rate elevated for some time. Businesses are likely to struggle to re-hire staff in the short term as their liquidity is increasingly constrained, and a period of social distancing may have forced businesses to transition to less labour-intensive operations. In other words, businesses who have found ways to operate through the crisis may not need to re-hire as many staff.

This suggests that over the next year or so, lasting, loosened conditions in the labour market could dampen demand for housing. With the cash rate now at a record low, recovery in incomes and jobs will be necessary to increase purchasing capacity.

How income losses impact mortgage repayments

Analysis from the RBA suggests that a 1 percentage point increase in the rate of unemployment can lead to an increase in the mortgage arrears rate of about 0.8 percentage points. At November last year, the mortgage arrears rate in Australia was about 1 per cent…

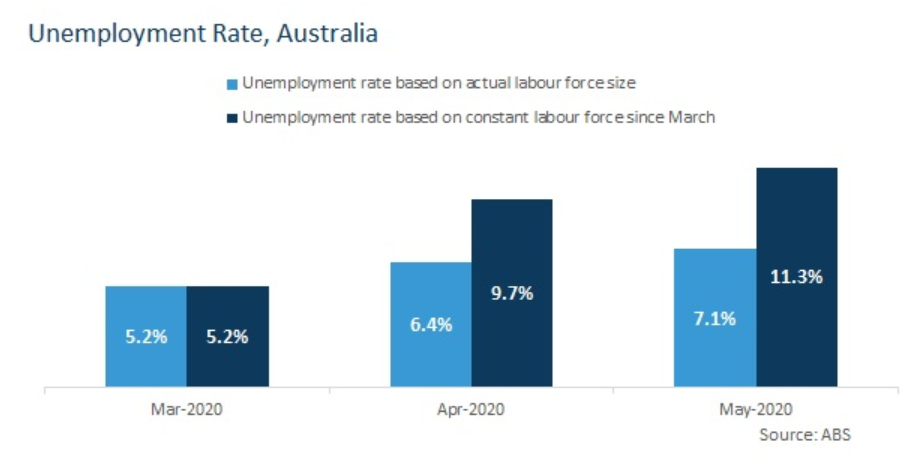

If the size of the workforce had stayed steady since March, the May unemployment rate would be 11.3%. At face value, this suggests that an increase of 1 percentage point in the unemployment rate may have more of an impact on arrears. However considering the composition of job losses amid COVID-19, the direct risk to property may be offset to an extent…

Detailed data shows a less direct threat to the housing market

Though labour market conditions have significantly deteriorated, many of the job losses seen over the past few months may not present a direct risk to the housing market. That is because many of those who have suffered job loss, are also less likely to hold mortgage debt.

For example, of 59.7% of the decline in the number of people employed between March and May were across those in part-time work. About 40% of the decline in total employed were among those aged between 15 and 24. Given the typical first home buyer is aged 25-34, it is unlikely many of those who have lost work in this age group would have mortgage debt.

Additionally, ABS analysis of payroll data suggests the biggest declines in employment by sector are across tourism, accommodation and the arts. Workers with these characteristics are less likely to hold mortgage debt than older workers in industries such as professionals, service workers and trades.

The economic impact of these job losses is still significant, and will impact the housing market indirectly, even if young people and those in tourism, hospitality and the arts, are less likely to hold mortgage debt. That is because they are more likely to rent. So the current declines in employment will likely have an indirect impact on housing prices, through weaker rental demand and downside risk for higher rental vacancies, lower rents and deteriorating yields.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.