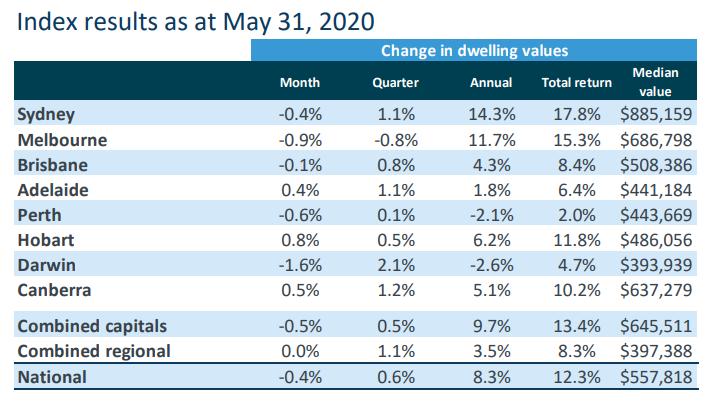

Following on from MB’s preliminary report at the 5-City level, CoreLogic has released its full dwelling value results for May, which reports that Australian dwelling values declined by 0.4% over the month, with capital city dwelling values declining more sharply by 0.5%:

As shown above, the smaller capitals experienced mixed conditions in May, with rises in Hobart (+0.8%) and Canberra (+0.5%) offset by a big decline in Darwin (-1.6%). Values across Australia’s regional areas were also flat.

According to CoreLogic, the decline in dwelling values was driven by the premium (top 25%) end of the market:

Advertisement