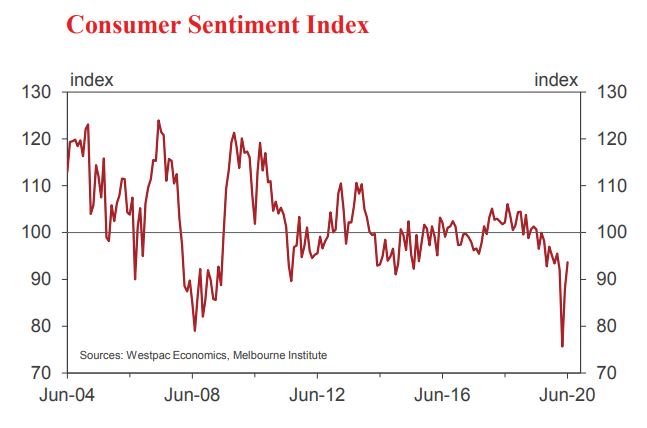

• The Westpac-Melbourne Institute Index of Consumer Sentiment rebounded 16.4% to 88.1 in May from the extremely weak 75.6 read in April.

Remarkably, consumer confidence is now back around pre-COVID levels, having recovered all of the extreme 20% drop seen when the pandemic exploded in March– April. Confidence has clearly been buoyed by Australia’s continued success in bringing the Coronavirus under control, which has in turn allowed for a further easing in social restrictions over the last month.

The Index is now only 2% below the average in the preceding September to February period. Note that sentiment was already on the weak side prior to the COVID shock with the Index through this earlier period showing a persistent excess of pessimists over optimists. With the unemployment rate set to remain elevated; extensive restrictions staying in place and the economy facing permanent structural change it would be surprising if the recent upward momentum continues and is able to sustain a stable level of confidence which is above that previous period.

We have also seen more even confidence levels in the major states as restrictions begin to be eased extensively across the country. Victoria lagged NSW in May with an 8.4% lift compared to 23%. However in June confidence in Victoria has jumped by 11.7% (to 94.9) compared to 4.8% in NSW (95.5). Overall confidence is now at comparable levels across both states.

While the monthly gains are impressive, the Index is still relatively weak by historical standards – in pessimistic territory overall and down 7% on a year ago. The general picture is of continued intense pressure on family finances

and concern about the near- term outlook for the economy but with firming optimism around prospects for finances in the year ahead and the economy’s medium term outlook.

The contrast between that medium-term outlook in this recession and the last recession in the early 1990s is important. This component of the Index is around 50% higher than the average over a long four years in that earlier period. Respondents are confident that they can see eventual better times ahead whereas in the early 1990s there was a pervasive mood of despair for years.

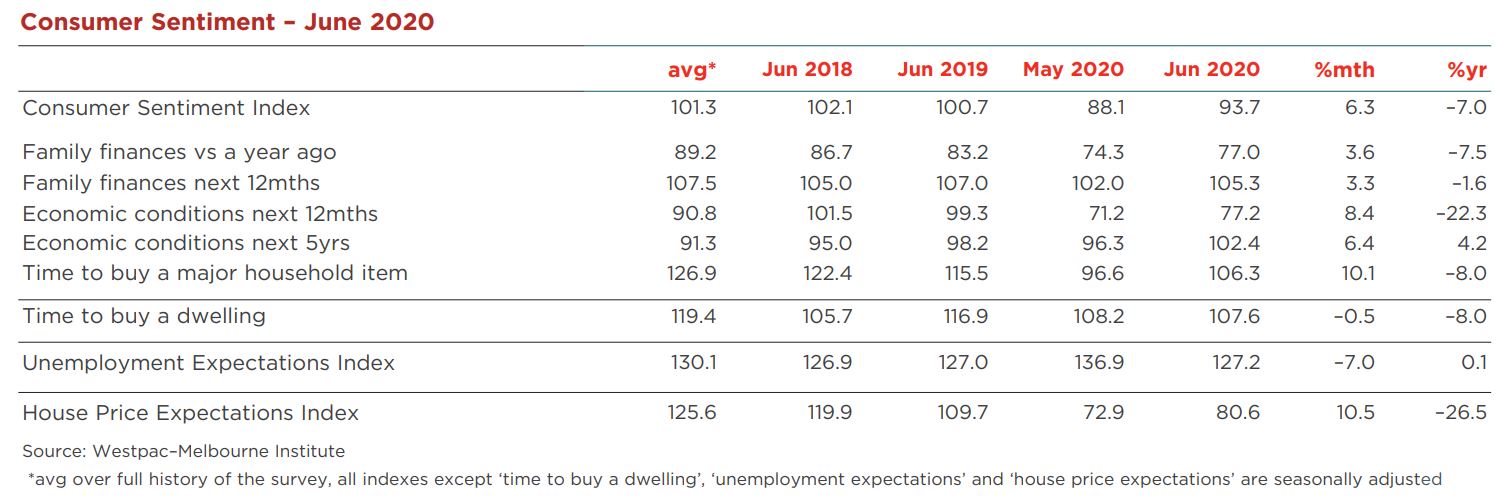

All component indexes recorded gains in June but the largest improvements were around views on the economic outlook and ‘time to buy a major item’.

Consumer concerns around the economy are definitely easing. The ‘economy, next 12mths’ sub-index is up another 8.4% and the ‘economy, next 5yrs’ sub-index is up 6.4%.

However, in the case of near term expectations, this is coming from an exceptionally weak starting point, the subindex recording a dire 53.7 in April. At 77.2, this component is still lower than any read since the GFC (excluding April and May) and very weak by historical standards. It is broadly consistent with only a gradual improvement from what will almost certainly prove to have been a recession in the first half of 2020.

That said, the 102.4 read on the ‘economy, next 5yrs’ subindex – an 18 month high – points to growing confidence that gains will be sustained once the recovery comes through.

Consumer assessments of family finances showed more muted moves – the ‘finances vs a year ago’ sub-index up 3.6% and the ‘finances, next 12 months’ sub-index up 3.3%. Current assessments of finances remain a notable weak spot. The sub-index read of 77 is a less impressive improvement on April’s low of 70.4 and still 12ppts below the long run average of 89. A reading of 77 is consistent with intense pressures on household budgets.

Consumers’ forward views are much brighter – at 105.3, the ‘finances, next 12 months’ sub-index is in net optimistic territory just a couple of points shy of its long run average of 107.5. The mix points to what is likely to be a delicate period for policy. A tangible improvement in finances, linked to the reopening of the economy, will be required (rather than just an expected one). This improvement will need to be firmly in place before key supports to household finances such as JobKeeper, JobSeeker and home loan repayment holidays can be withdrawn.

On a more promising note, the picture from buyer sentiment suggests we may see a significant ‘pop higher’ in some forms of spending near term. The ‘time to buy a major item’ sub-index posted another strong 10.1% gain in June after a 26.7% surge in May. Some of this is undoubtedly the direct impact of the Coronavirus and social restrictions – consumer views on ‘shopping’ appear

to be returning to normal although buyer sentiment is still a long way from pre-COVID levels – the 106.3 reading on this sub-index may be positive but it is still well below the long run average of 127.

Our June survey includes an update of additional questions, which measure respondents’ recall of various categories of news. Note that the previous series in March was conducted prior to the COVID-19 outbreak and associated lockdown.

In both surveys there is a strong focus on the domestic economy but, not surprisingly, there has been a clear shift.

In March concerns over news abroad were prominent.

The virus outbreak was starting to spread beyond China sparking concerns about the global economy as financial markets were melting down.

In the June survey, the focus is more on government policy and jobs. News on the economy had the highest recall throughout (54% in June and 45% in March). There was a marked improvement in the assessment of the economy in June although, overall, opinions were still cautious.

However, the second and third highest news items recalled in June were ‘employment’ (35%) and ‘Budget and tax’ (27%). That compares with March, when ‘international conditions’ (25%) captured more attention.

Notably, whereas the news on ‘employment’ is viewed as deeply unfavourable this month, the news on ‘Budget and tax’ was viewed much less negatively than in March.

In March 74% of respondents were negative about government policy compared to only 54% in June.

While consumers remain concerned about the economy’s near-term prospects and the news around employment they are much less concerned about the prospect of a further rise in unemployment. The Westpac-Melbourne Institute Unemployment Expectations Index fell a further 7% in June, following a 13.4% drop in May more than unwinding all of the 17.4% jump over March–April (recall that lower readings indicate that more consumers expect unemployment to fall in the year ahead). The impressive turnaround means the index is now at 127, slightly below its long run average of 130. Note that this is consistent with a stabilisation in unemployment around current levels over the next year rather than a decline back to preCOVID levels. Nevertheless, the easing in job loss fears is

a key factor that will tend to see those still with jobs less restrained with their spending decisions. The complication around this reading is how those respondents whose employers are receiving JobKeeper payments feel about their job security.

Sentiment around housing showed a modest improvement in June, assessments around ‘time to buy’ consolidating on previous gains and price expectations showing a lift, albeit to still very weak levels.

The ‘time to buy a dwelling’ index dipped 0.5% but held on to most of May’s strong rebound following the collapse in this index in April. At 107.6, the index continues to hold in positive territory but is still well below 2019’s average level of 118 – a pattern evident across all of the major states.

To date, house prices have held up surprisingly well, albeit on extremely low turnover. Resilient reads on ‘time to buy a dwelling’ are encouraging but the survey continues to point to a sharp deterioration in the outlook for prices compared to a few months ago.

Consumer expectations for house prices posted a solid gain, with the Westpac-Melbourne Institute House Price

Expectations Index lifting 10.5%. That said, at 80.6, the index is still in deeply pessimistic territory, 43% below the optimistic readings immediately prior to the COVID-19 lockdown. Again, pessimism extends across all the major states although it is somewhat more entrenched in Victoria (75.3) than in NSW (84.2).

Responses to additional questions on the ‘wisest place for savings’ show risk aversion has lifted since March. ‘Safe options’ are still in favour – two thirds of consumers nominating deposits, superannuation or ‘pay down debt’ as the best place for savings, compared to 63% in December.

The proportion favouring real estate dropped back to 9% from 13% in March – matching the record low set this time last year. With price expectations negative, investors look likely to stay away from Australia’s housing market near term. Unusually, more respondents nominated shares (11.4%) than real estate as preferred investment options.

The Reserve Bank Board next meets on July 7. This survey will boost confidence around the Board table. Note that the Bank’s current forecasts envisage the unemployment rate still at 6.5% (two percentage points above the full employment rate) and inflation at 1.5% (one percentage point below the target) by June 2021. Despite this unsatisfactory situation the Board has committed to no further action on interest rates. Having reached the assessed effective lower bound on the cash rate of 0.25% the Governor has noted that it is extraordinarily unlikely that the Bank will take rates lower.

An earlier than expected recovery in the economy will ease pressure on that current entrenched policy stance.

Impro\ved but still quite depressed about house prices.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.