Jeremy Cooper, retirement income chairman at Challenger, has comprehensively debunked the myth of the ‘retirement trap’ – the notion that the benefit of having extra superannuation savings is more than offset by reduced access to the Aged Pension:

Age pension payments reduce at a rate of $3 per fortnight for each $1000 in assets over the thresholds. This amounts to $78 a year, or a rate of 7.8 per cent. It’s called the taper rate.

Many say it’s too hard to earn income at a rate of 7.8 per cent a year to replace the age pension for which wealthier retirees are being overlooked. They say retirees who have built up savings above the thresholds are worse off than if they hadn’t saved anything.

The “trappist” view wrongly compares investment returns on savings above the thresholds against the cash flows received from the age pension. They are not so easily compared. Using an investment return lens ignores how retirees can use their capital to their benefit.

Retirees don’t need a return as high as 7.8 per cent to beat the taper rate. They can spend some of their capital to match the age pension withdrawn. This has the advantage that they will get more age pension in future years, so they might eventually need to spend less capital over time.

Too right. Superannuation nest eggs are not supposed to be preserved so that they can be passed on to one’s heirs. They are supposed to be drawn down to fund one’s retirement.

Consider a 65-year old with a superannuation nest egg of $500,000 earning 5% per annum.

Someone with a ‘trappist’ mindset would argue that this nest egg would only provide $25,000 a year in income (i.e. 5% times $500,000), when in fact $38,200 is available over 20 years if principal is also drawn down.

We should also remember that the Coalition in 2017 merely returned to pension taper rate to the level that existed prior to Peter Costello halving it in 2006.

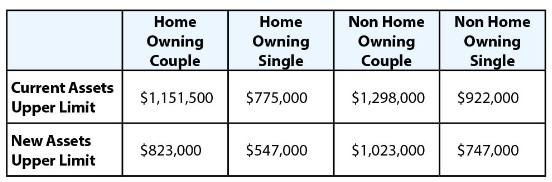

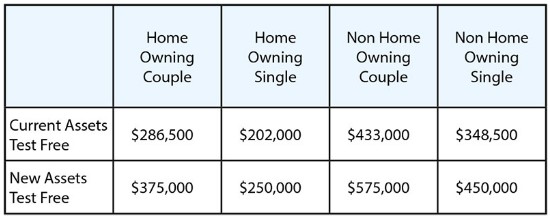

Costello’s changes had created the ridiculous situation whereby retiree home owning couples with $1.15 million in other assets, and home owning singles with $775,000 of other assets, could still qualify for the part Aged Pension along with the Pensioner Concession Card.

While some wealthy retirees would no longer keep receiving the part Aged Pension (but would keep their concession card) under the Coalition’s 2017 reforms:

The Government would provide additional funding to pensioners with fewer assets:

The reform package was projected to save the Budget (and younger Australians footing the bill) some $2.4 billion over four years, whilst improving the lot of pensioners without significant assets. On equity and sustainable grounds, it was a policy no-brainer.

As an aside, the best way to expand to Aged Pension without costing taxpayers is to abolish the compulsory superannuation system, whose concessions cost the Budget $43 billion a year and are poorly targeted to high income earners:

The obscene cost of Australia’s superannuation system is preventing the Age Pension from being lifted.