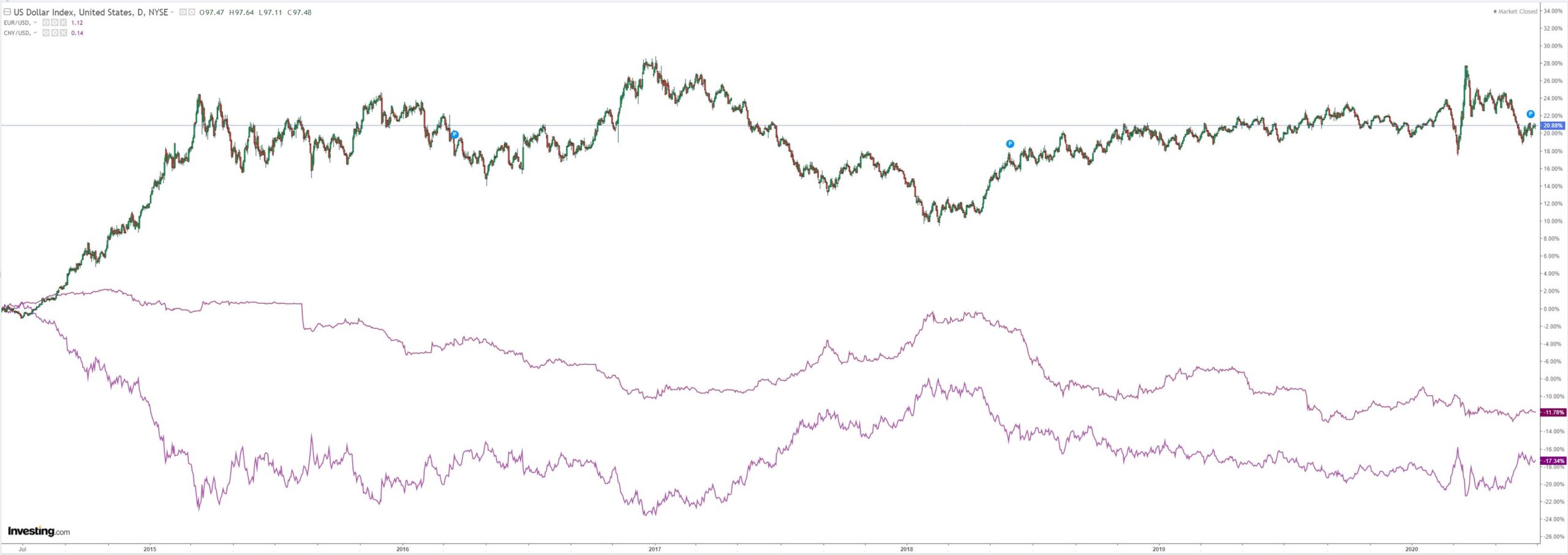

DXY was up last night:

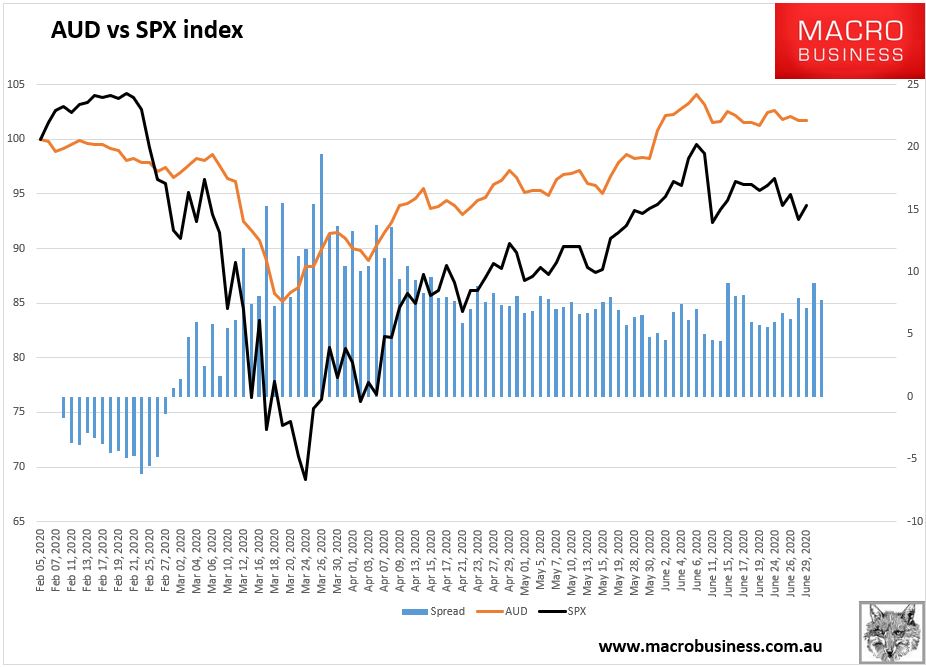

The Australian dollar was universally soft:

Gold held at the highs:

Oil too:

Dirt is clearly into an uptrend now:

Miners were stable:

And EMs stocks:

Junk is still sending a warning:

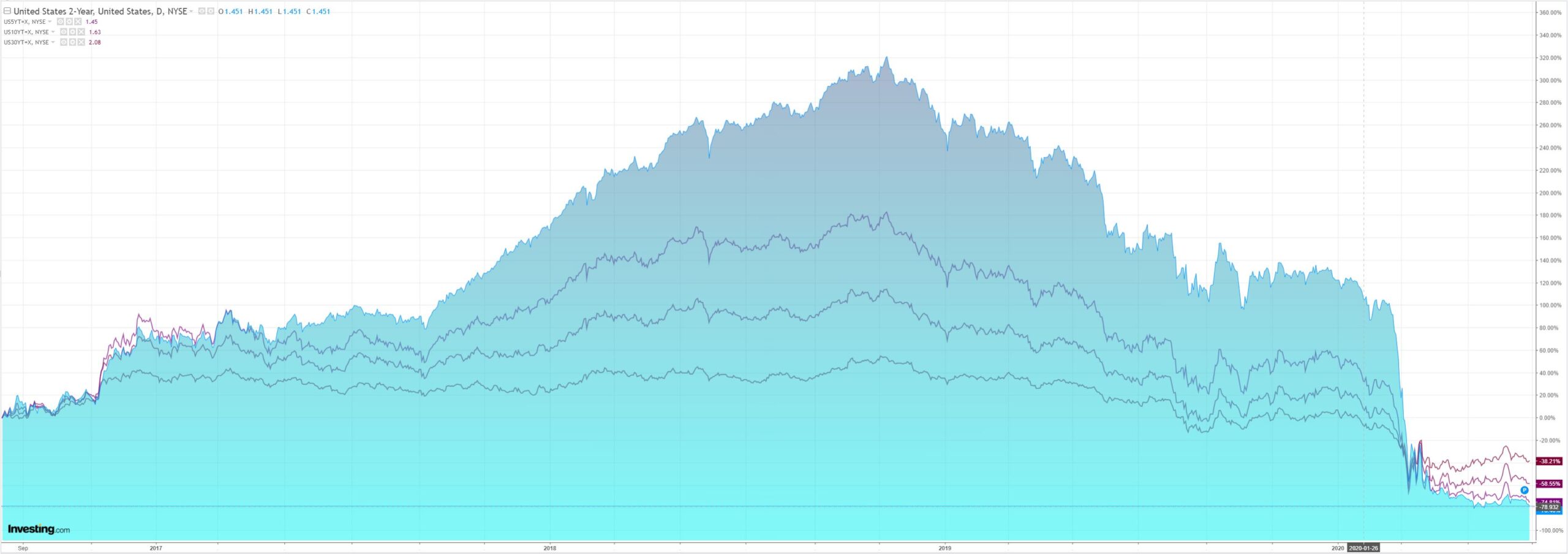

Bonds were mostly bid:

Stocks rebounded on the usual late ramp:

Westpac has the wrap:

Event Wrap

US pending home sales posted a surprise record gain of +44.3%m/m in May (vs est. +18%), the annual pace -10.4%y/y (est. -22%, prior -34.6%), as states emerged from the lockdown. The Dallas Fed manufacturing survey was stronger than expected, despite high Covid growth rates in the state. The survey index rose from -49.2 to -6.1 (est. -21.4), back at 2019 levels, led by production rising to +13.6 (from -28.0) and new orders rising to +2.9 (from -30.6). Although employment remained negative (-1.6, prior -11.5), wages rose (+6.8 from -0.2), and most other components showed solid improvements.

German CPI was firmer than expected in June, as was intimated by individual state data, rising +0.6%m/m (est. +0.3%m/m) to +0.9%y/y.

UK BoE released May credit data which showed a deeper pullback in mortgage approvals to a mere 9.3k (est. 25k, average pre-lockdown was above 65k), and a further pullback in consumer credit of -3%m/m (est. flat).

Event Outlook

Australia: May private sector credit will be published today with both the market and Westpac forecasting a flat read, 0.0% due to a slowdown in housing and the soft business outlook. RBA Deputy Governor Debelle will speak at 12:30pm on “The RBA’s policy actions and balance sheet”.

New Zealand: Given the flash result in early June, the final estimate for the June ANZ business confidence survey should confirm an improvement, though the index remains at depressed levels (prior: -33)

China: After a strong comeback, the market expects the manufacturing PMI (prior: 50.6, market f/c: 50.5) and non-manufacturing PMI (prior: 53.6, market f/c: 53.6) to hold their ground in June.

Euro zone: Inflation is likely to stay muted for the foreseeable future; the market is not expecting a material change in June (prior: 0.1%, market f/c: 0.2%)

UK: Consumer sentiment has stabilised after the personal finance and major purchase outlooks rose in May. The market expects a slight move up from -30 to -29 this month. The final estimate for Q1 GDP will likely remain unchanged at -2.0%. There is a lot more economic pain to come for the UK.

US: The market view on the S&P/CS home price index remains positive with expectations of a 0.5% gain in April despite Covid. Continuing the trend of positive regional survey data, the June Chicago PMI will be released today (prior: 32.3, market f/c: 44.0). Consensus estimates also see a boost in consumer confidence in June from 86.6 to 90.5. FOMC Chair Powell and Treasury Secretary Mnuchin will testify before the House Financial Services Committee (02:30 AEST) and FOMC member Williams will speak on Central Banking in the Age of Covid (01:00 AEST).

Pick any reason you like for the stocks bounce. My favourite is that it is Monday and weekend virus reporting is always better.

That’s still all that matters. The ASX/SPX correlation continues:

And will determine Australian dollar value until the dust settles around the relative value of stocks versus the recovery in prospect.