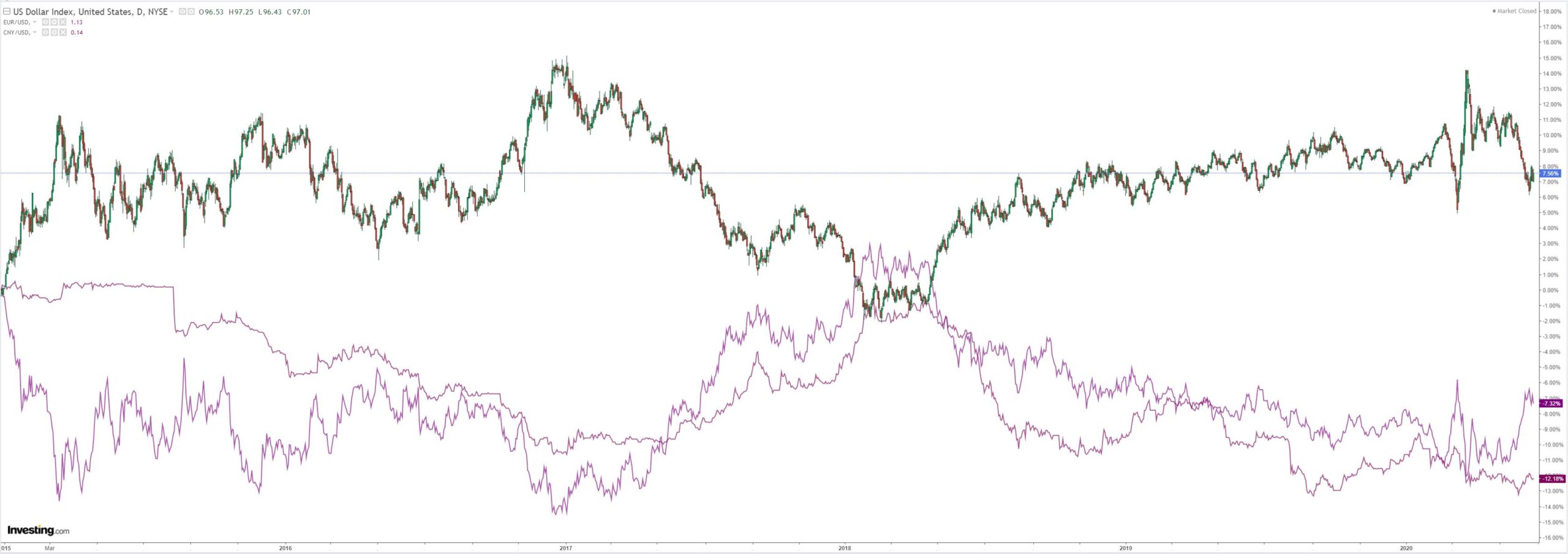

DXY was strong last night:

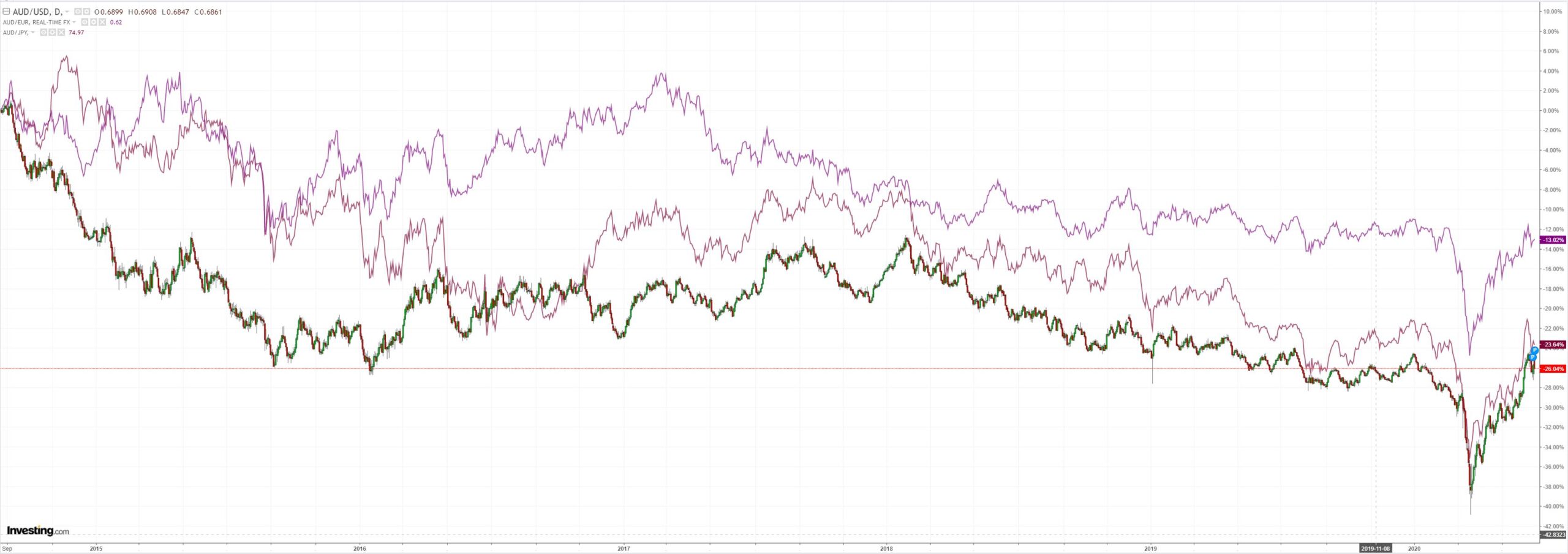

So the Australian dollar was weak:

EMs were even weaker:

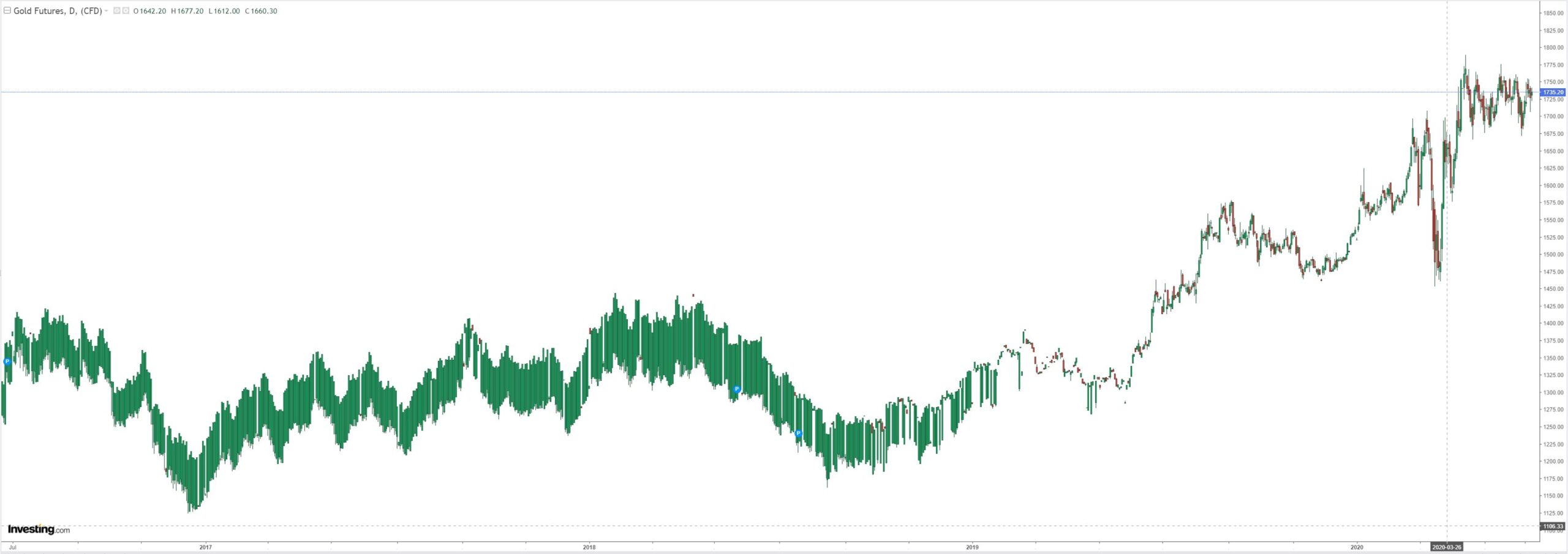

Gold is trapped at the break out line:

Oil gained:

Dirt too:

Miners were mixed:

EM stocks flamed out:

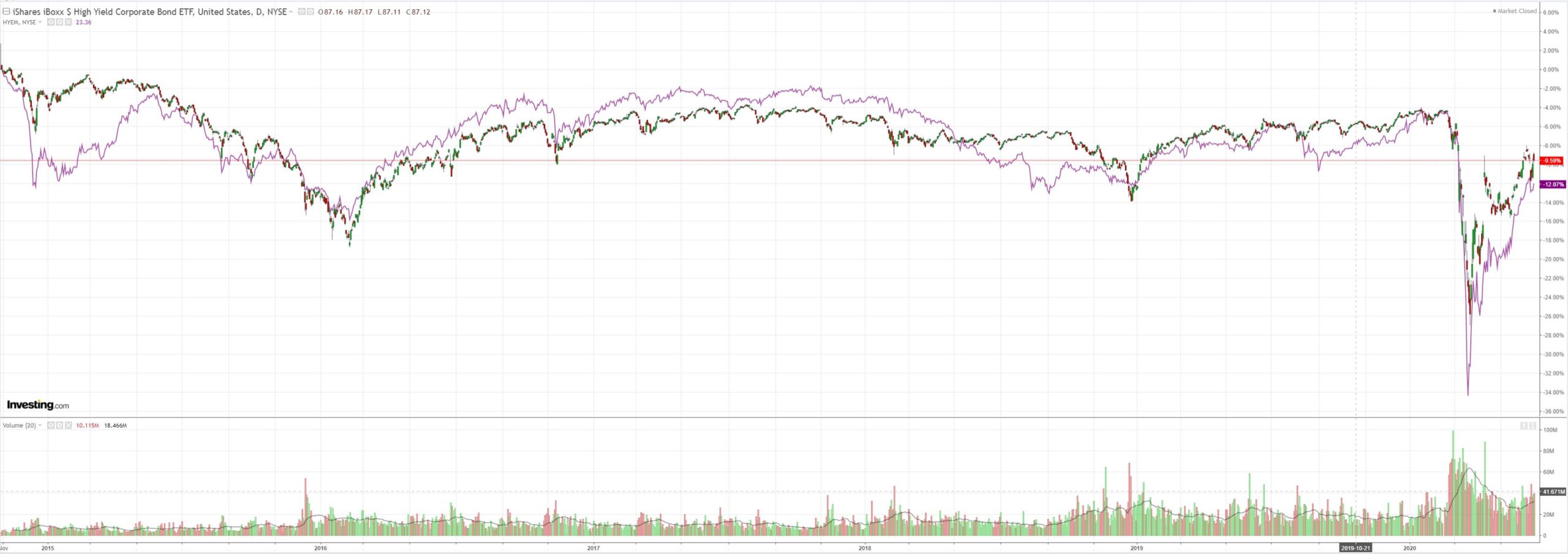

Junk did better:

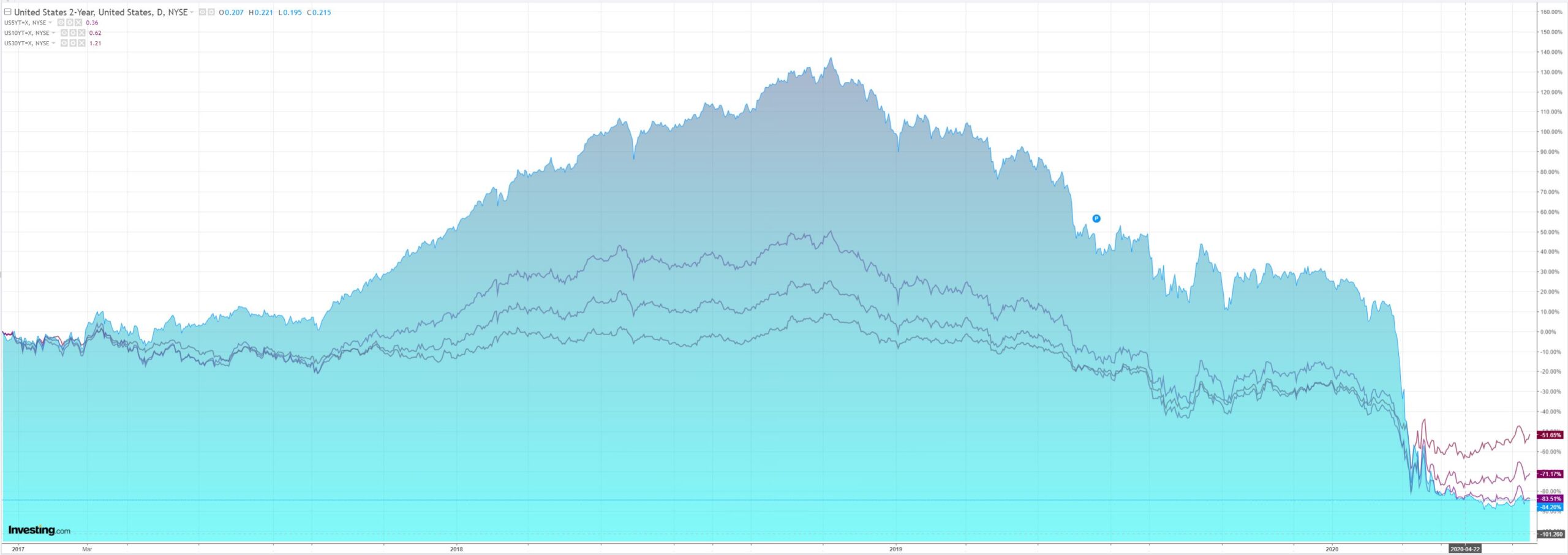

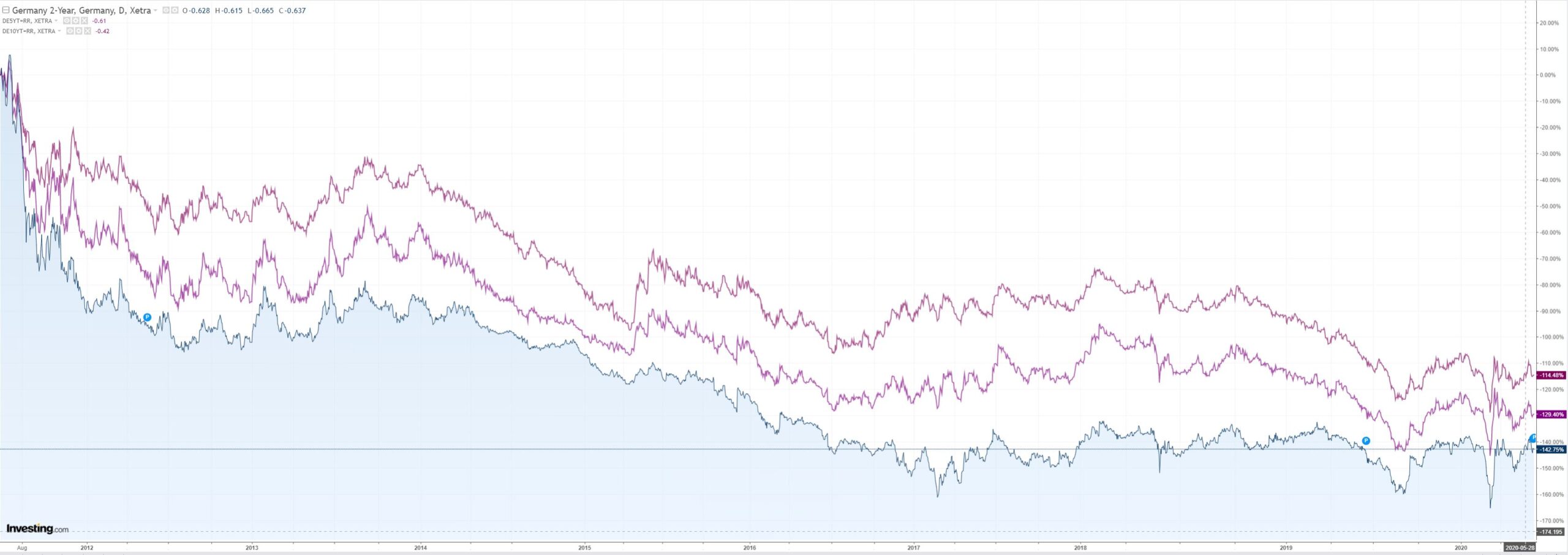

Bonds sold:

Stocks have recovered half their recent losses:

Wrap from Westpac:

Event Wrap

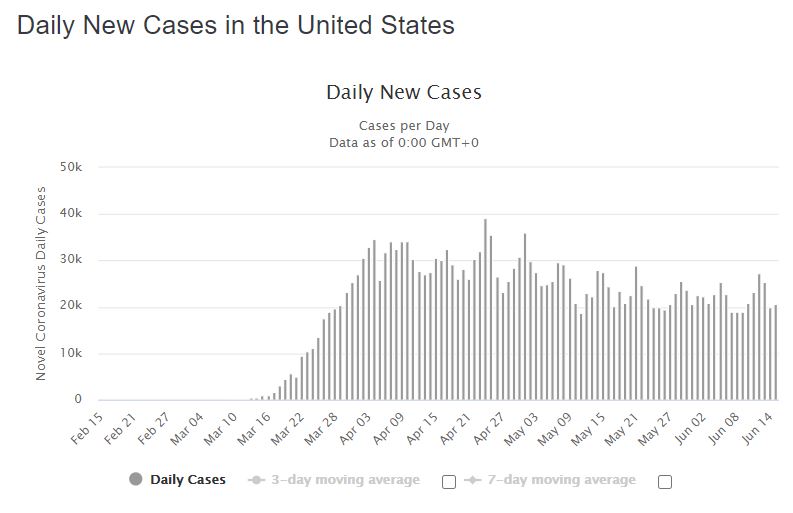

There were reports that Florida’s COVID infection rate had risen to 3.6% from a 7-day average of 2.5%, Texas hospitalisations had risen 8.3% (highest in 2 weeks), and Beijing had imposed activity restrictions (closing schools and stopping travel to Beijing).

Fed Chair Powell maintained a positive and accommodative tone. Following his testimony, Powell responded that yield curve control had not been decided upon and was at the early stages of being evaluated by the FOMC. Uncertainty about the recovery ensured the Fed’s accommodative stance whilst remaining flexible.

US retail sales headline bounced sharply in May, +17.7%m/m (vs est. +8.4%m/m, prior revised to -14.7%m/m from -16.4%m/m. The control group rose +11.0%m/m (est. 5.2%m/m, prior revised to -12.4%m/m from -15.3%m/m) and ex-auto and gas rose +13.4%m/m (est. +5.4%m/m, prior revised t -14.4%m/m from -16.2%m/m). Following April’s record fall, May’s record rebound still leaves sales substantially below 2019 levels.

May industrial production only rebounded +1.4%m/m (vs est. +3.0%m/m, prior revised to -12.5%m/m from -11.2%m/m), with capacity utilisation remaining low at 64.8% (prior revised to 64.0% from 64.9%). The NAHB homebuilder confidence survey rose more than anticipated to 58 (est. 45. prior 37). Although the NAHB economist cited concerns over employment and virus risks, he noted increased demand for single family, low density suburban homes.

Eurozone ZEW June survey posted large increases in economic expectations, although current conditions remained weak. Expectations rose for Germany to 63.4 (est. 60.0, prior 51.0) and Eurozone to 58.6 (prior 46.0), while current conditions languished at -83.1 (prior -93.5) and -89.2 (prior -95.0) respectively.

Event Outlook

Australia: The Westpac-MI Leading Index slumped to -5.16% in April, a rate comparable to the lows seen during the GFC and in prior recessions. The May reading is likely to see a further deterioration given many components of the index are still extremely weak and as the headline measure from the survey is a 6-month annualised changed – heavily impacted by the severe declines of March and April.

New Zealand: The annual current account deficit narrowed to -3.0% GDP in Q4 last year. Westpac expects it to narrow further to -2.7% of GDP as goods exports rise slightly and imports decline sharply.

Europe/UK: Inflation will remain absent in both the Euro area and UK in May. Consensuses estimates sit at -0.1% and 0.0% respectively.

Canada: The May CPI is likely to be weak given expectations of a 40% contraction in economic growth. The market predicts a flat result for inflation of 0.0% from -0.2% in April.

US: A rebound in housing starts and permits for May looks promising with the market forecasting large gains in both (starts – market f/c 23.5%, prior: -30.2%; permits – market f/c: 17.3%, prior: -20.8%). FOMC Chair Powell will complete two days of testimony in Washington (02:00 AEST) and Mester (06:00 AEST) will also speak.

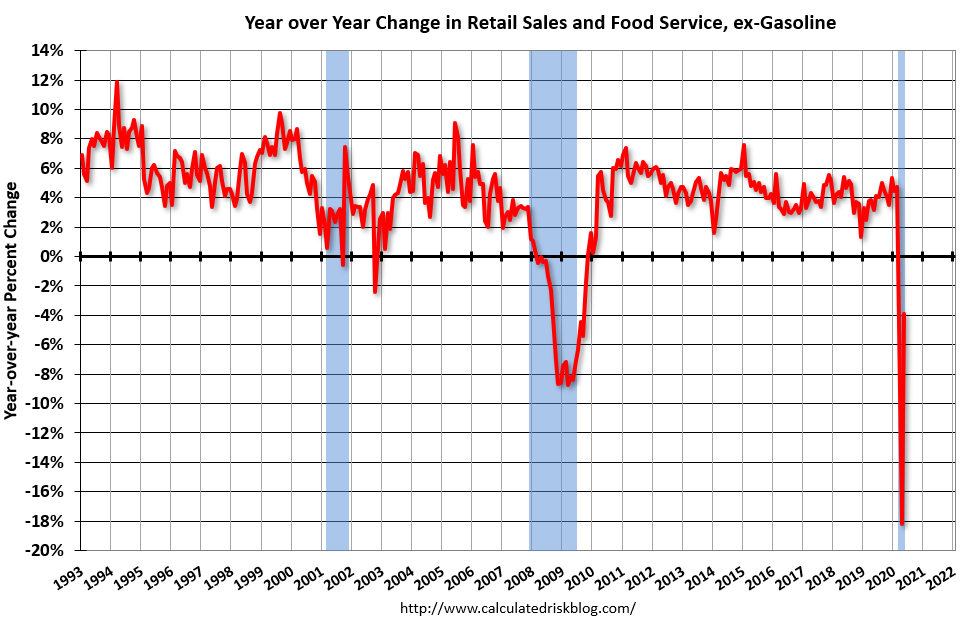

There was much excitement in stocks owing to the US retail report but it was not very good at all, down 4% in May year on year:

We can expect some kind of pent-up demand in the US’ mighty consumer but it’s going to get killed by the ongoing virus spread in short order:

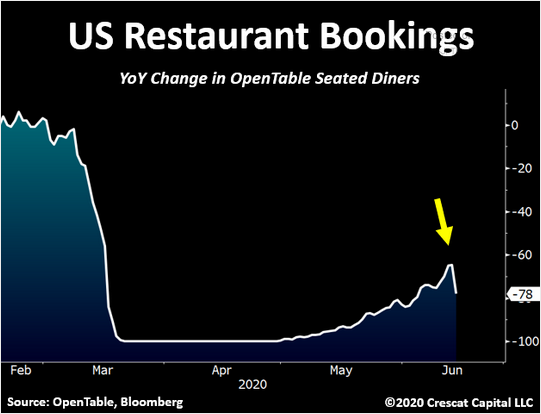

It has already landed on eating out:

Jay Powell tried to warn as much last night. All stocks heard was MOAR stimulus, which is the equity market’s singular refrain for now.

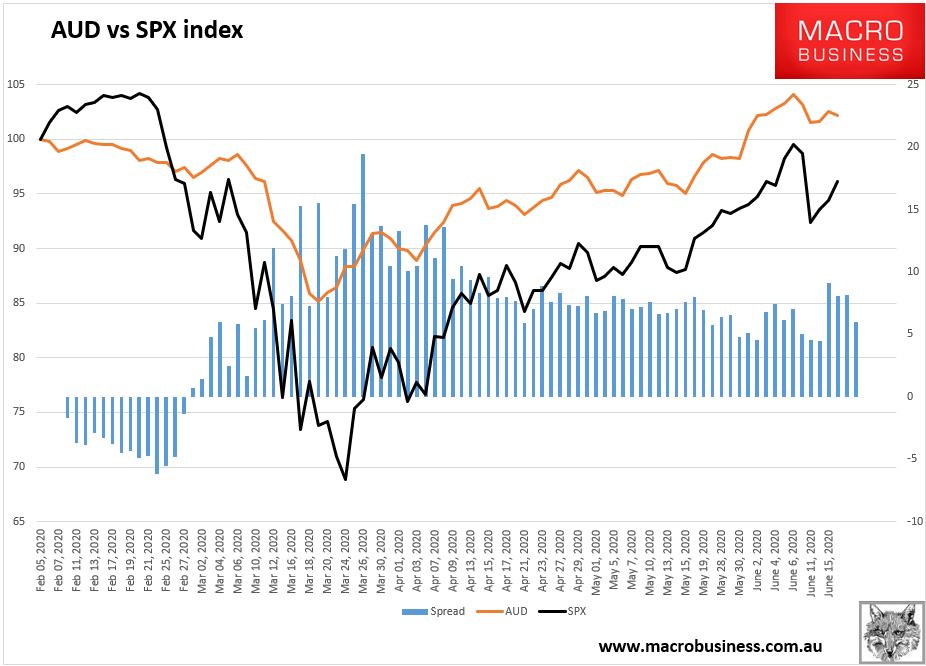

It was left to forex to price risk as virus cases rose and China and India mulled war. The USD rose and the AUD got a rare break from rising with stocks:

They still appear joined at the hip.