DXY was down sharply last night:

The Australian dollar surged:

Gold is still stuck right at the break out line:

Oil hit new recovery highs:

Base metals were mixed:

Miners did better:

EM stocks as well:

Not junk:

Bonds were firm:

Nasdaq kept the bubble alive, at new all-time highs:

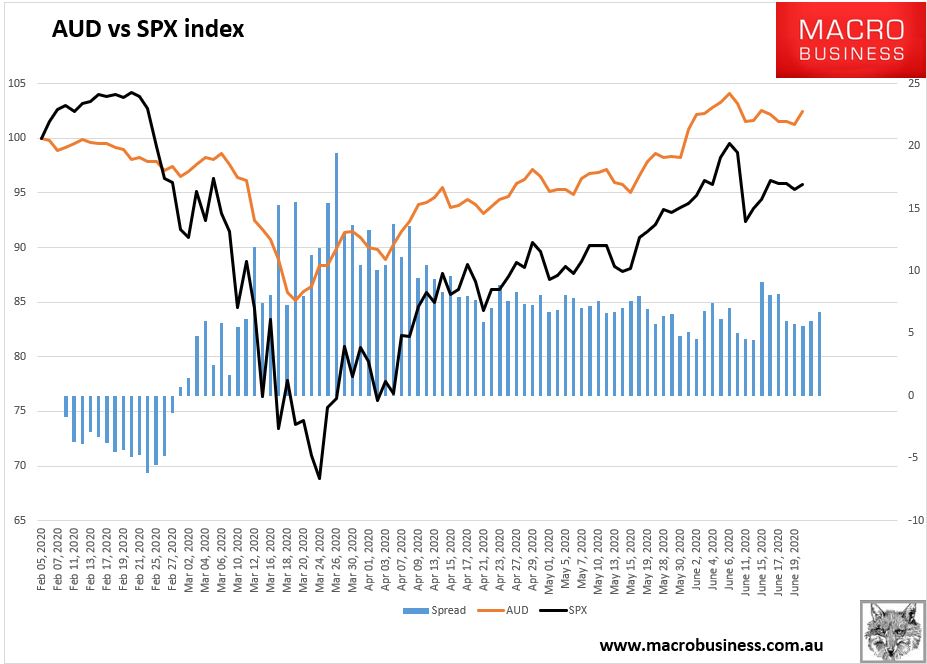

The SPX/AUD correlation rolls on:

Westpac has the wrap:

Event Wrap

US May Chicago Fed National Activity survey rose to +2.6 (est. -10) from prior -17.9, led by improvements in production and employment components. May existing home sales fell 9.7% to 3.91mn, the lowest level in a decade as lockdowns hit the real estate sector.

Event Outlook

Australia: Preliminary merchandise trade data for May will be released, but is unlikely to have a substantial effect on markets given its ‘unfriendly format’ — not seasonally adjusted and on a customs basis.

Japan: The Jibun Bank manufacturing and services PMIs will be released today. Respective readings of 38.4 and 26.5 in April are likely to be improved upon, though a further significant contraction in activity is still expected.

Taiwan: Industrial production growth has slowed but remains positive over the year. The market forecasts a slight decline from last month’s YoY% estimate of 3.51% to 2.95% in May.

Germany: PMI data is expected to show an improvement in activity across manufacturing (prior: 36.6, market f/c: 42.3) and services (prior: 32.6, market f/c: 42.0). Within manufacturing, auto production came to a virtual standstill in April, but at least a third of activity has reportedly come back online in May.

Eurozone: The release of Markit PMI data continues in the Eurozone overnight, with the market predicting an increase in manufacturing (from 39.4 to 44.8) and services (from 30.5 to 41.2).

US: New home sales may surprise to the upside given the partial re-opening of state economies that is occurring (prior: 0.6%, market f/c: 1.9%). High unemployment will remain a significant headwind in the months ahead, partially offset by ultra-low interest rates. The Markit PMIs for the manufacturing sector (prior: 39.8, f/c: 47.8) and services (prior: 37.5, market f/c: 44.8) are set to rise. Regional survey outcomes are also likely to be positive.

Not much to add. AUD outperformed after Phil Lowe’s unnecessarily stupid comments yesterday.

In the last few weeks, AUD has outperformed stocks a little as our virus performance comes to bear. Fair enough. But Australian dependence upon immigration for growth will come to bear on the recovery in the medium term. No other country is more damaged by collapsed people flows than we are and that will necessitate a much lower currency or much higher public spending in the medium term.

For now, nothing has changed. The AUD will rise so long as stocks do. And vice versa.