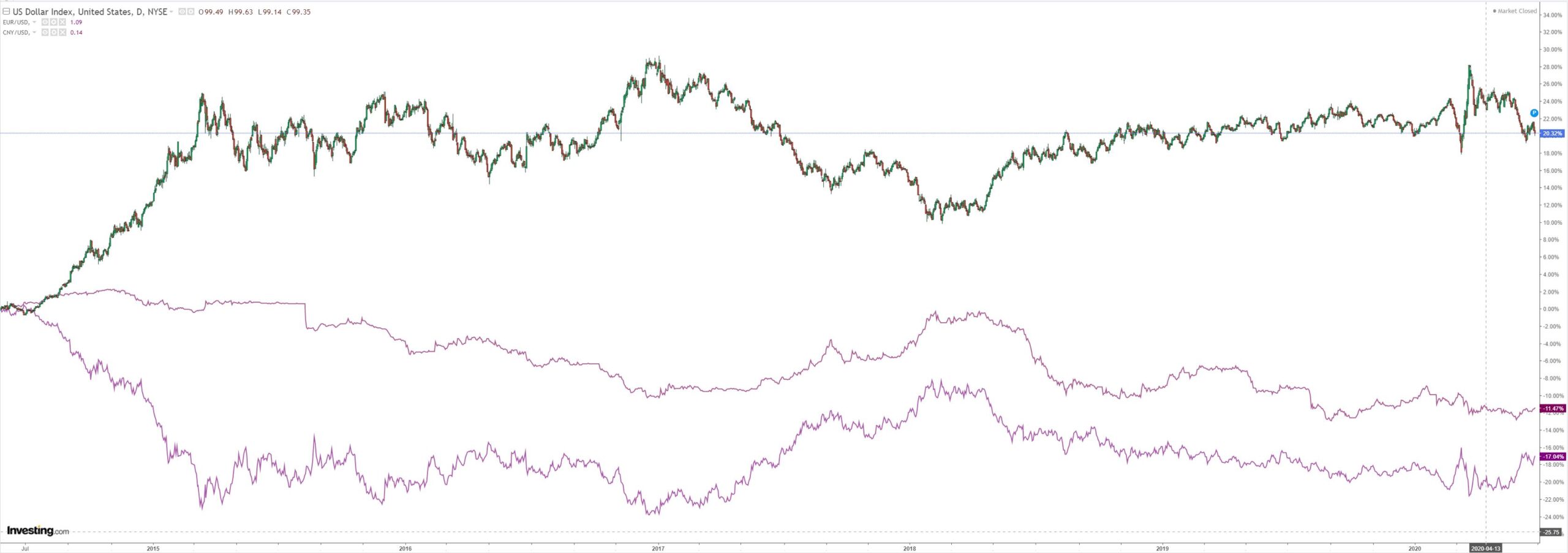

DXY resumed falls last night:

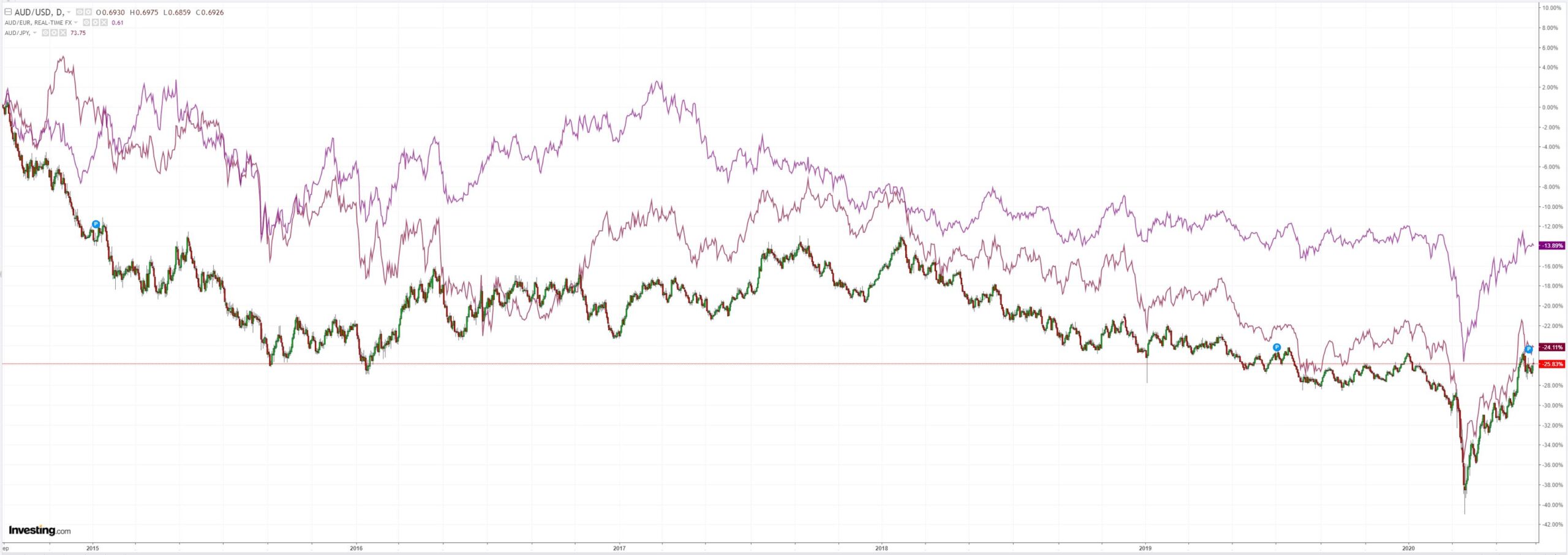

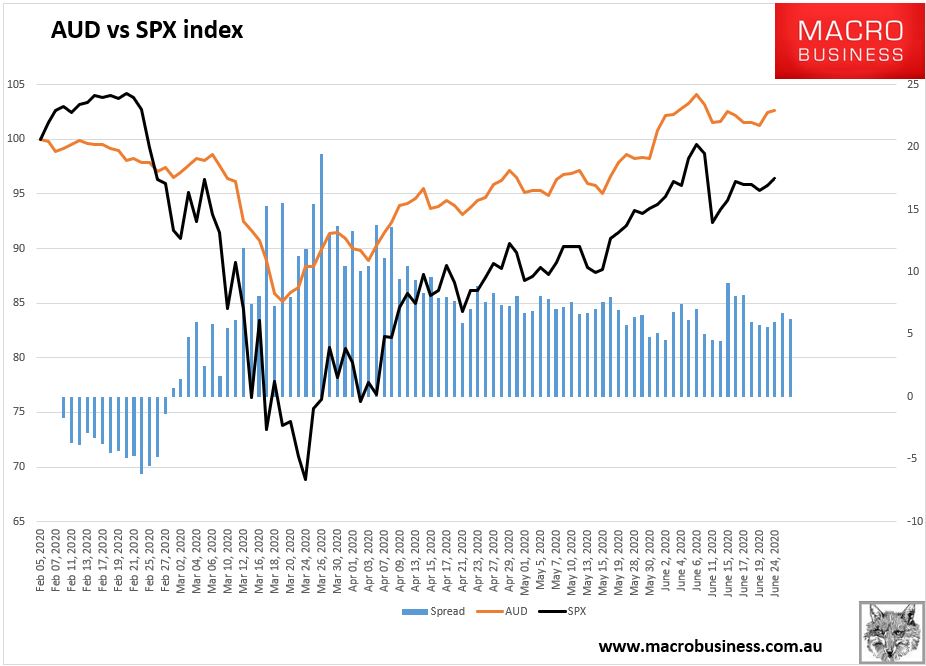

The Australian dollar was pretty soft all things considered:

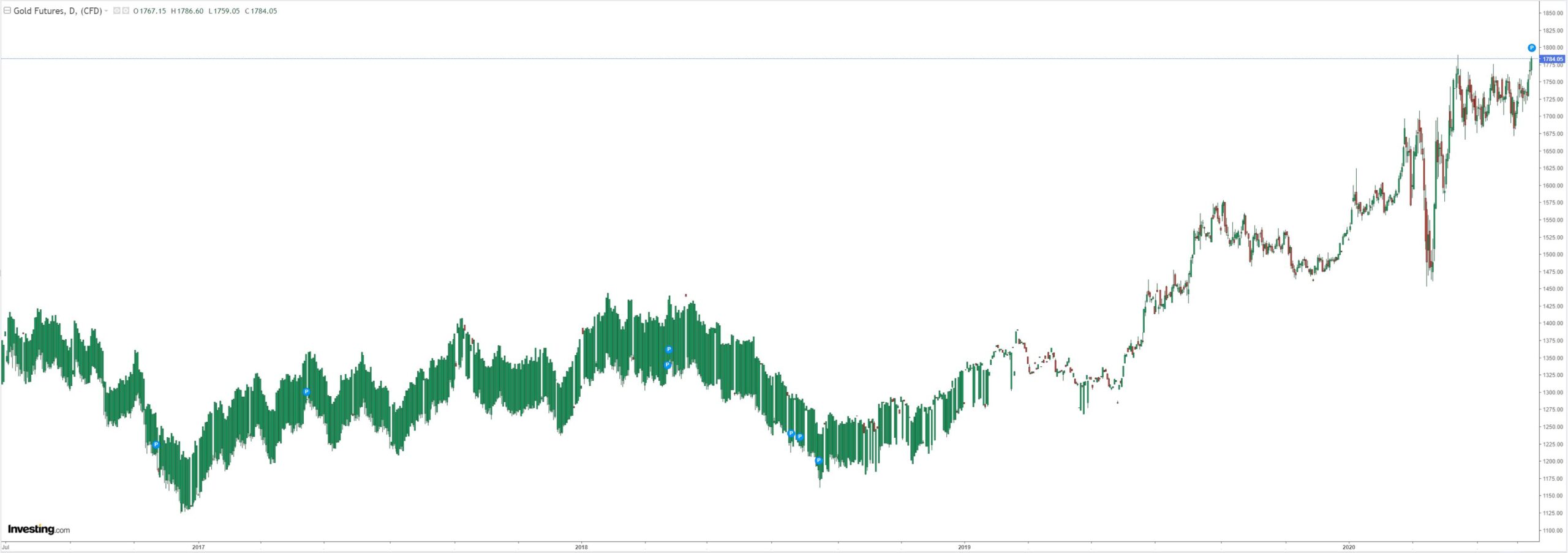

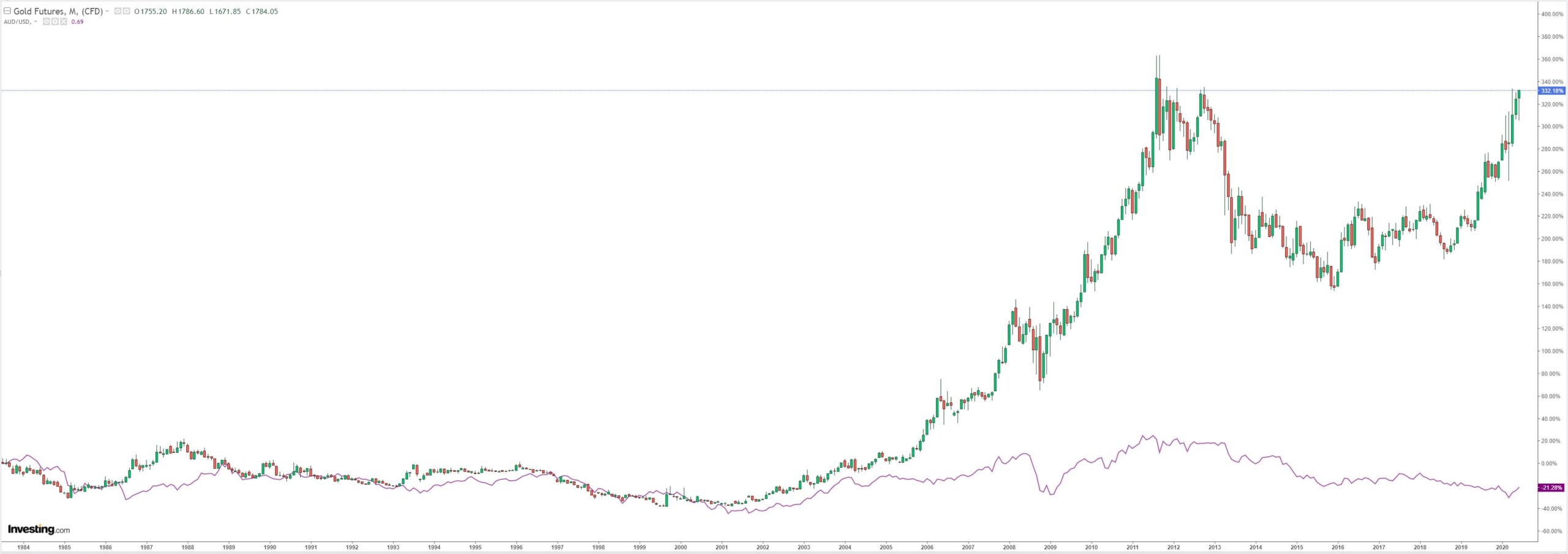

Gold finally broke out to new closing high:

Oil struggled:

And dirt:

Miners were strong:

EM stocks too:

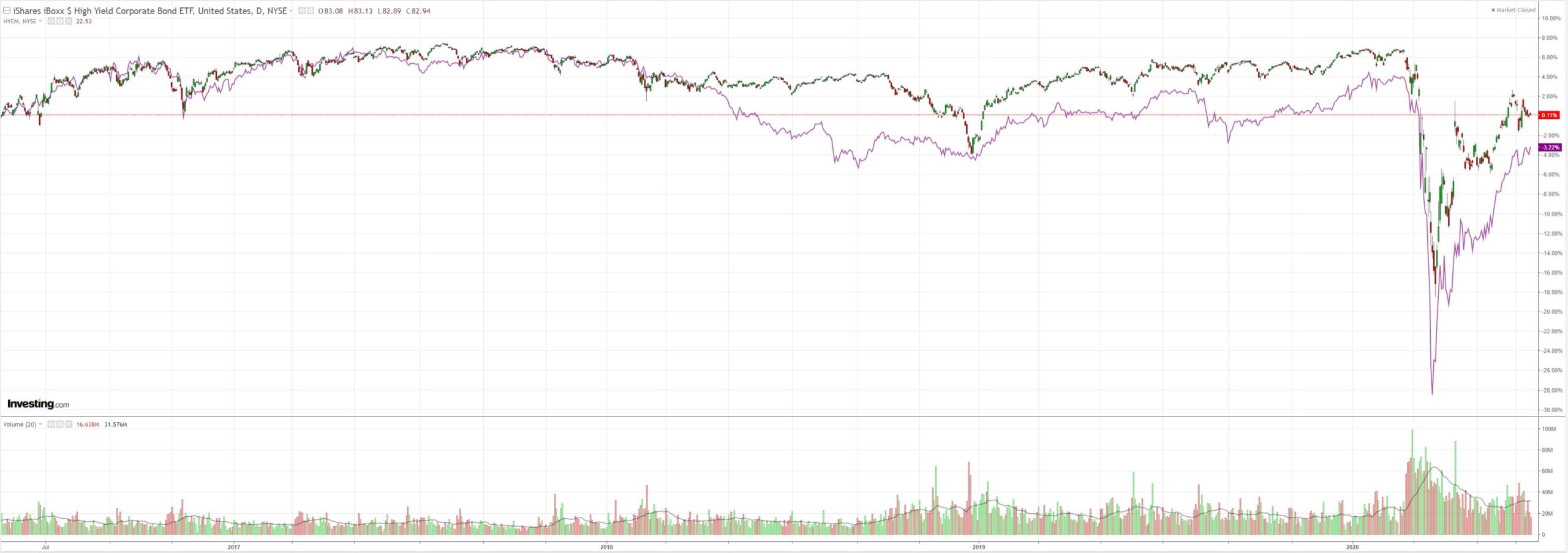

And junk:

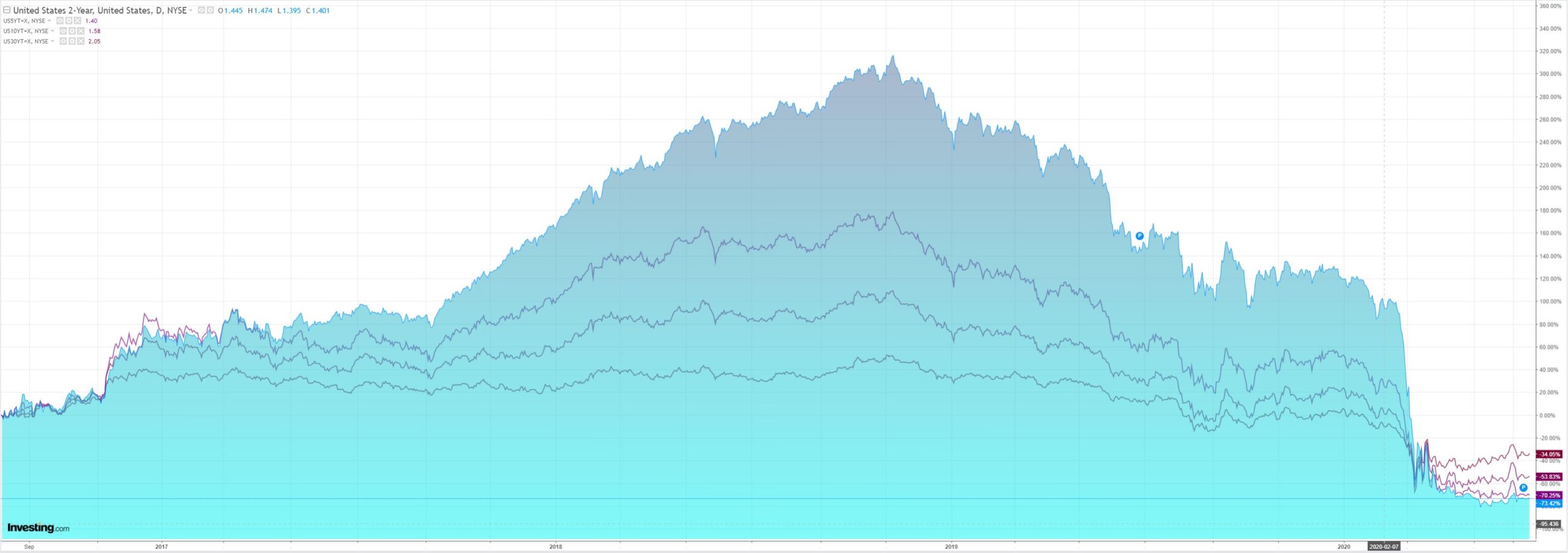

Bonds were soft:

The great bubble inflated some more:

Westpac has the wrap:

Event Wrap

US Administration spokesmen continued to discuss the potential of cash payouts and tax cuts in the next economic support/stimulus package. White House Economic adviser Kudlow added that the China trade deal “is on” and that China was “actually picking up their game” on more than just commodity purchasing.

US Flash June PMIs rebounded to near expected levels. Manufacturing rose to 49.6 (est. 50.0, prior 39.8) and services to 46.7 (est 48.0, prior 37.5). Richmond Fed June manufacturing survey rose to 2 from prior -27 (est. 0-2), with sound gains in most components and a healthy lift to 5 (prior -35) in new orders. May new home sales rose to 676k (est. 640k). The monthly gain of 16.6% was outsized due to a sharp downward revision to April (from 623k to 580k).

Eurozone Flash June PMIs beat expectations with manufacturing rising to 46.9 (est. 45.0, prior 39.4) but gains were, as in other regions, more substantial in services which rose to 47.3 (est. 41.4, prior 30.5). French PMI’s actually entered expansion: manufacturing 52.1, services 50.3. However, Markit’s write up pointed to the severity of the current recession and likely slow recovery despite the lift in optimism from respondents.

UK Flash June PMIs also rose more than anticipated. Manufacturing edged into expansion at 50.1 (est. 45.0, prior 40.7) and services rose to 47.0 (est. 40.0, prior 29.0). Though noting the turnaround, Markit warn of the impact on employment in relation to a modest recovery in 2021.

Event Outlook

New Zealand: The RBNZ will meet today. Westpac and the market expect the cash rate and the weekly pace of asset purchases to remain unchanged. The RBNZ may however choose to emphasise it has other policy tools available if further stimulus is required.

China: Although the current account balance will be confirmed to have experienced a dramatic fall in Q1 2020 to a deficit of $29.7 billion, the services balance is expected to be supportive going forward.

Germany: The market expects a robust improvement in the June IFO business climate survey from 79.5 to 84.8 as optimism grows.

US: The FHFA house price index has recorded slight gains throughout the COVID-19 pandemic. The May result will likely be no different (prior: 0.1%, market f/c: 0.3%). FOMC members Evans (02:30 AEST) and Bullard (05:00 AEST) will take part in virtual discussions on the economy.

In other words, the European PMIs were terrible and things are still getting worse even if at a slower pace. The market doesn’t care.

The SPX/AUD correlation is intact and that is still all that matters:

But I will pretend that other factors are playing a role, for fun. Gold breaking out is usually a bullish sign for the AUD although that correlation has fallen away over the years:

Given gold is really just the undollar the correlation makes sense. But I wouldn’t take that too far. Gold is leveraged to the relative strength in the underpinnings of the USD, not the USD itself, so it can run much further than the currency can fall.

Strong gold is a marginal bullish pressure for the AUD.