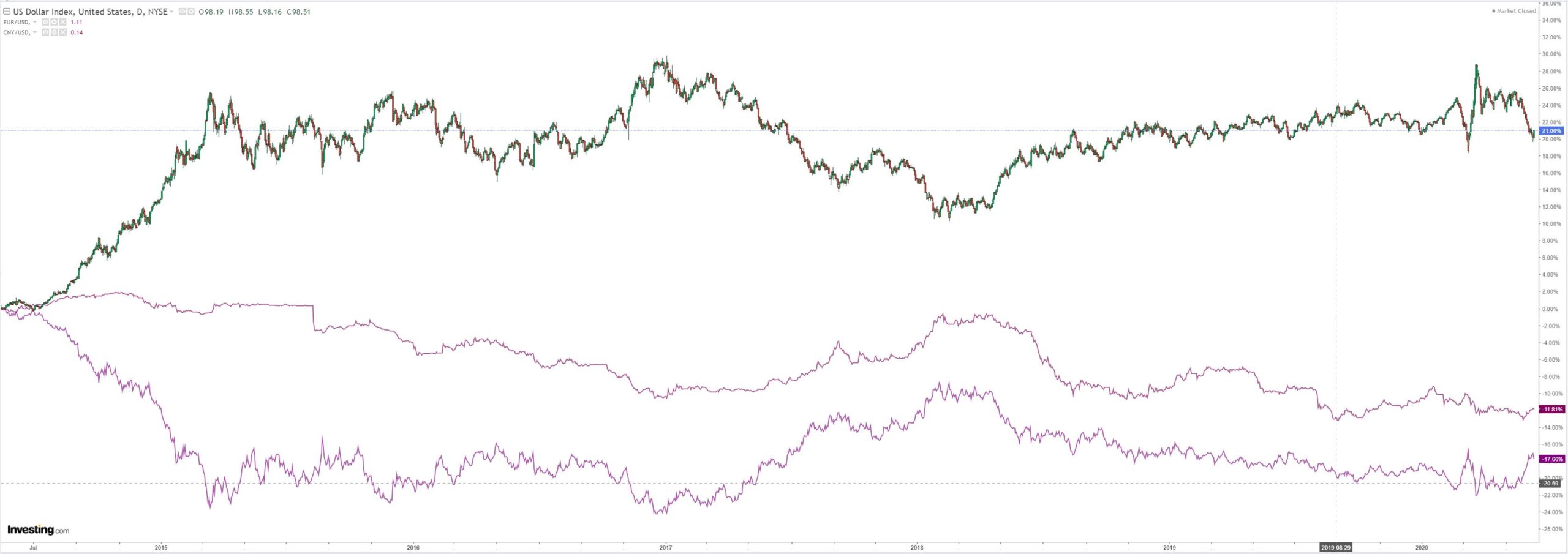

DXY took off last night:

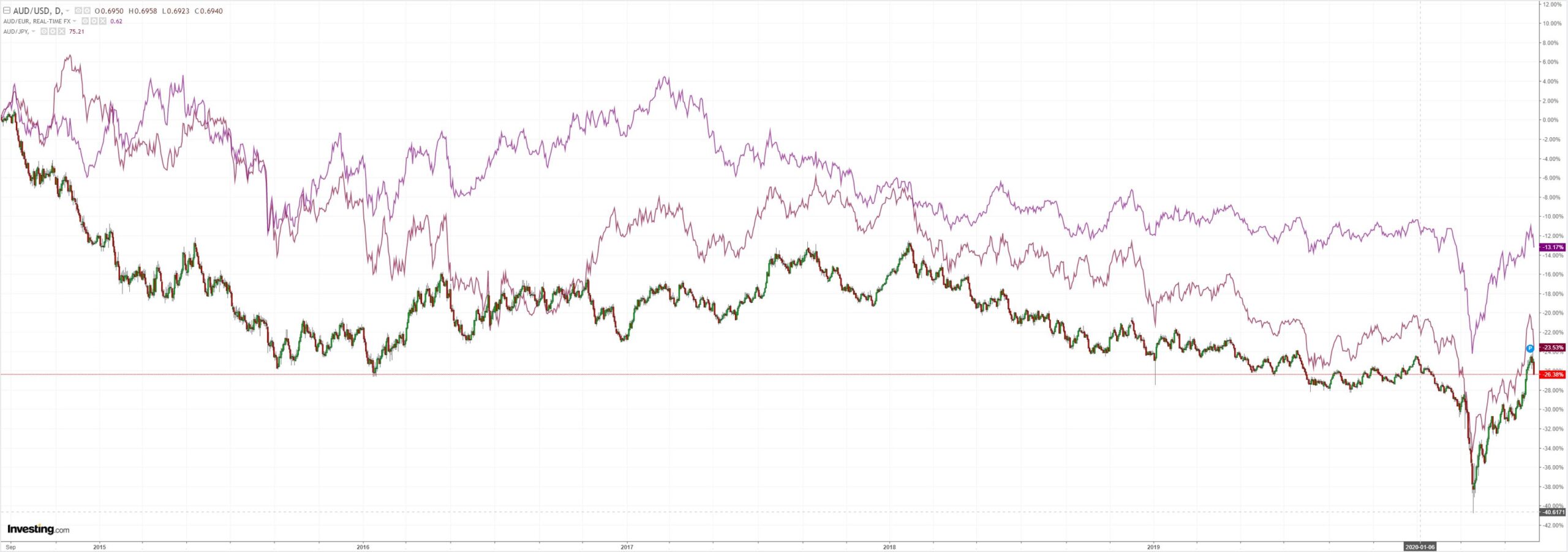

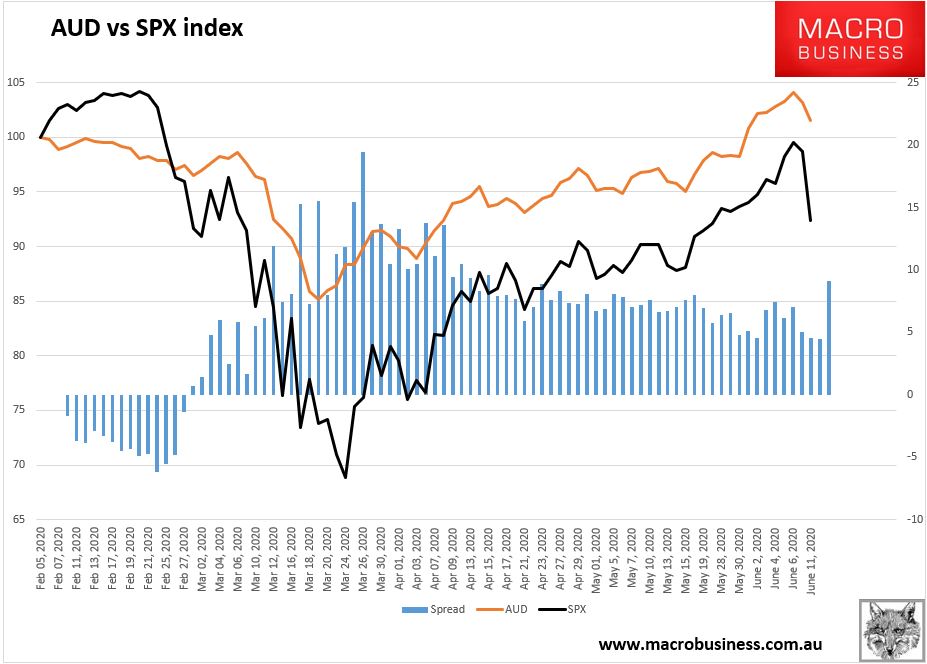

The Australian dollar was thunderstruck:

Gold was firm and is still poised for break out:

Oil copped it:

Dirt too:

Miners were smashed:

The EM gap into madness slammed shut:

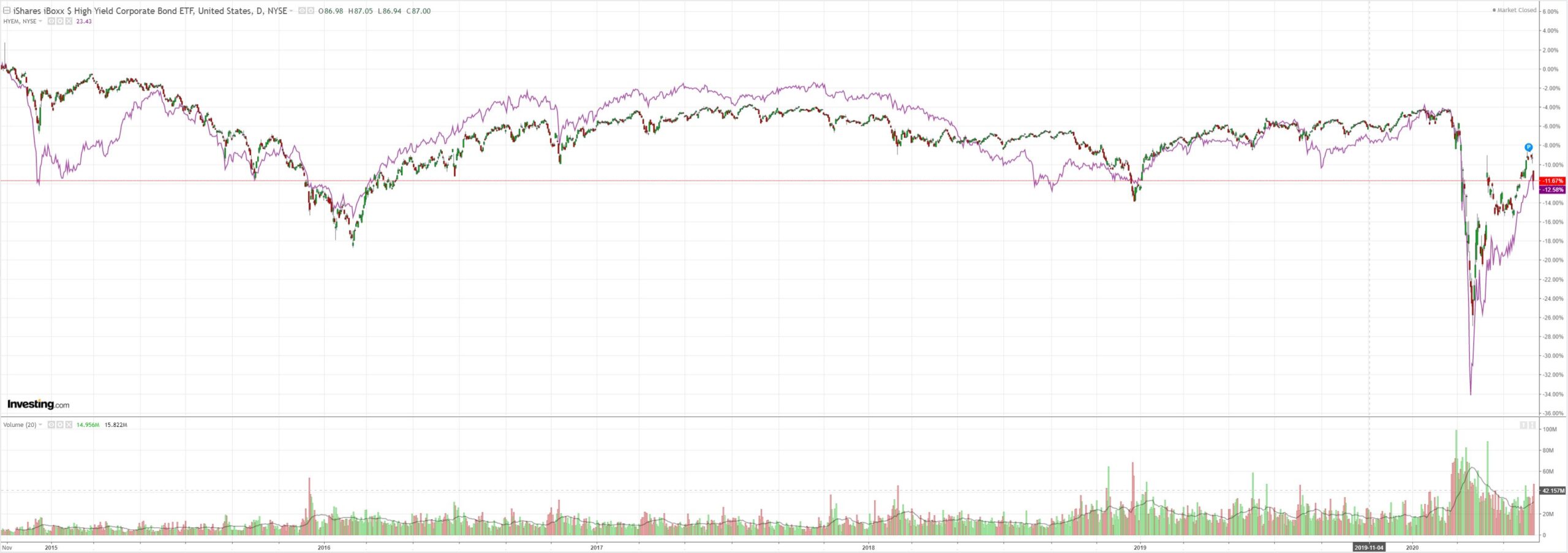

Likewise junk:

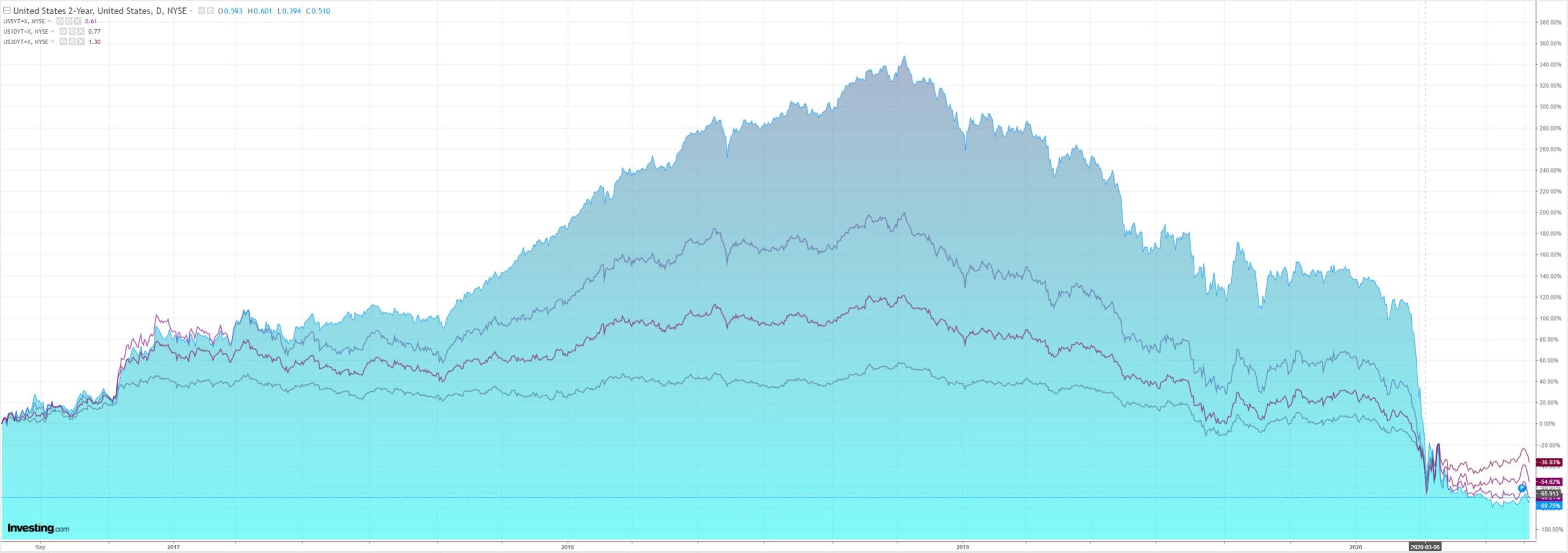

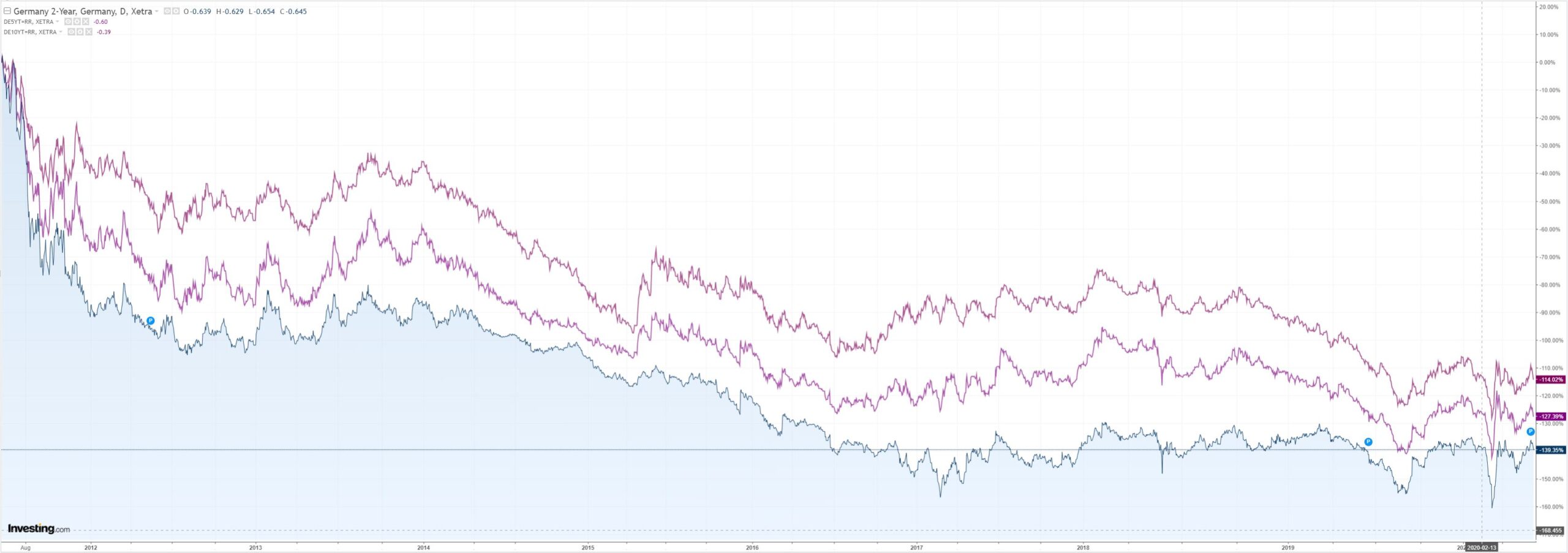

Bonds lit up:

Stocks drove straight off a cliff:

Westpac has the wrap:

Event Wrap

US weekly jobless claims of 1.54m were close to the 1.55m estimate, while and continuous claims at 20.9m were slightly higher than the 20.0m expected. May PPI inflation appeared a touch firmer than expected at 0.4%m/m and -0.8%y/y (est. +0.1%m/m and -1.2%y/y) but the core measure was in line at -0.1%m/m and +0.3%y/y.

Event Outlook

New Zealand: Although the May manufacturing PMI was still at a low level of 26.1, it is expected to lift in June as the economy opens further. Following this, Westpac anticipates that the food price index will be shown to have been flat in May, though measurement may be hampered by COVID-19 restrictions.

Euro Area: Industrial production is set to crater in April, reflecting what has arguably been the worst single month in the history of the Eurozone economy. Germany, the bloc’s strongest economy, has already seen industrial production collapse by 17.9% over April.

US: The May import price index is expected to lift after a fall in April, led by the recovery of energy prices (market f/c 0.7%). Mirroring the broader improvement in conditions, the University of Michigan Consumer Sentiment Survey is expected to tick up to 75.0 in June – the index remains well above its GFC low of 55.3.

And so ends the Great Fakeflation. Killed by an uber-bullish Fed that was so accommodating that it couldn’t deliver the boost that stocks needed. Remember that the Great Fakeflation has been a bizarrely accelerated full capital markets cycle with a boom, bust, USD safe haven, EM choke, stimulus, momo, fomo, USD unwind, EM dash for trash, bond back-up and rotation to value. A cycle that would normally take three years played out in the fantasy world of competing macro algos in three months with zero reference to the real economy. All egged on by an army of greedy retail investors with nothing better to do.

For the fantasy to continue the Fed had to support the bond back-up and rotation to value which, of course, it couldn’t given it does look at the disaster that is the real economy. Dreaming markets were pricing in higher interest rates when the Fed probably needs a cash rate somewhere around -5%.

And so, the Great Fakeflation ended with the last in being the first out, value, absolutely destroyed. We might theorise that the crash has to play out until at least that leg of the fantasy fully reverses. Basically all of May’s gains.

But if reality is going to creep back in as a factor for price discovery, there has to be an uncomfortable risk now that the entire rally reverses. And goes to new lows to boot.

For the Australian dollar, the Great Fakeflation simply made it a US equity proxy:

And so it remains until reality fully returns.