DXY was soft last night:

The Australian dollar was a raging bull:

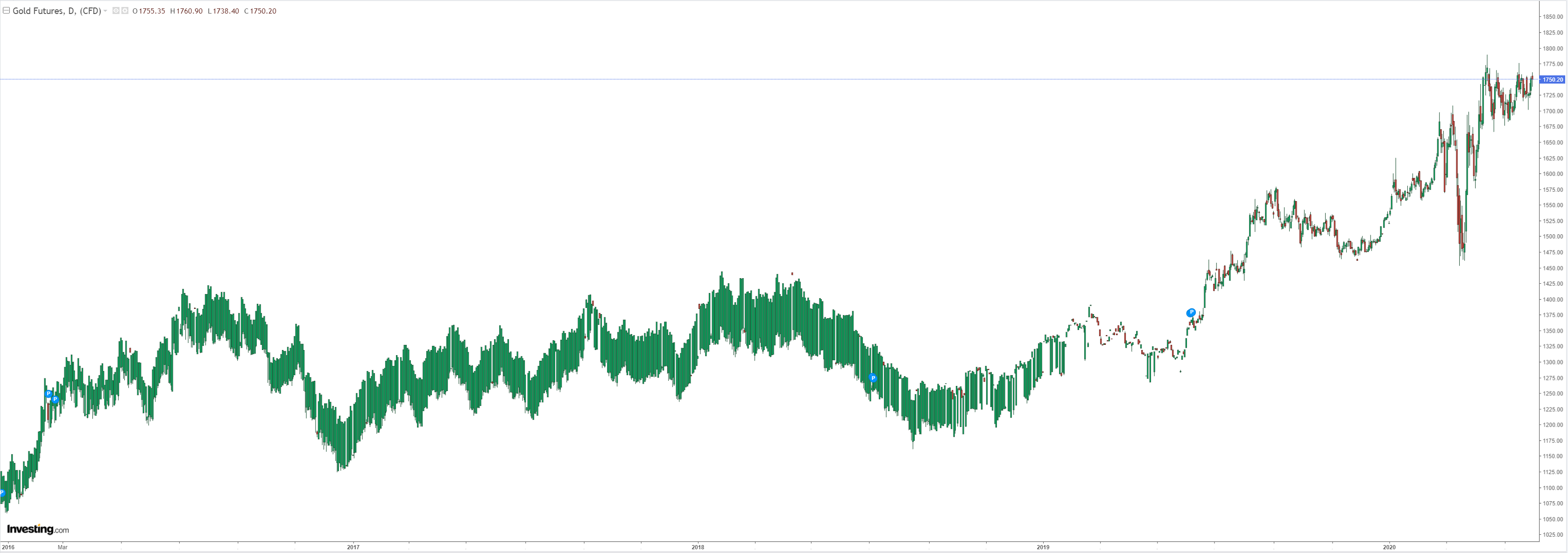

Gold is poised at the break out line:

Oil piles it on:

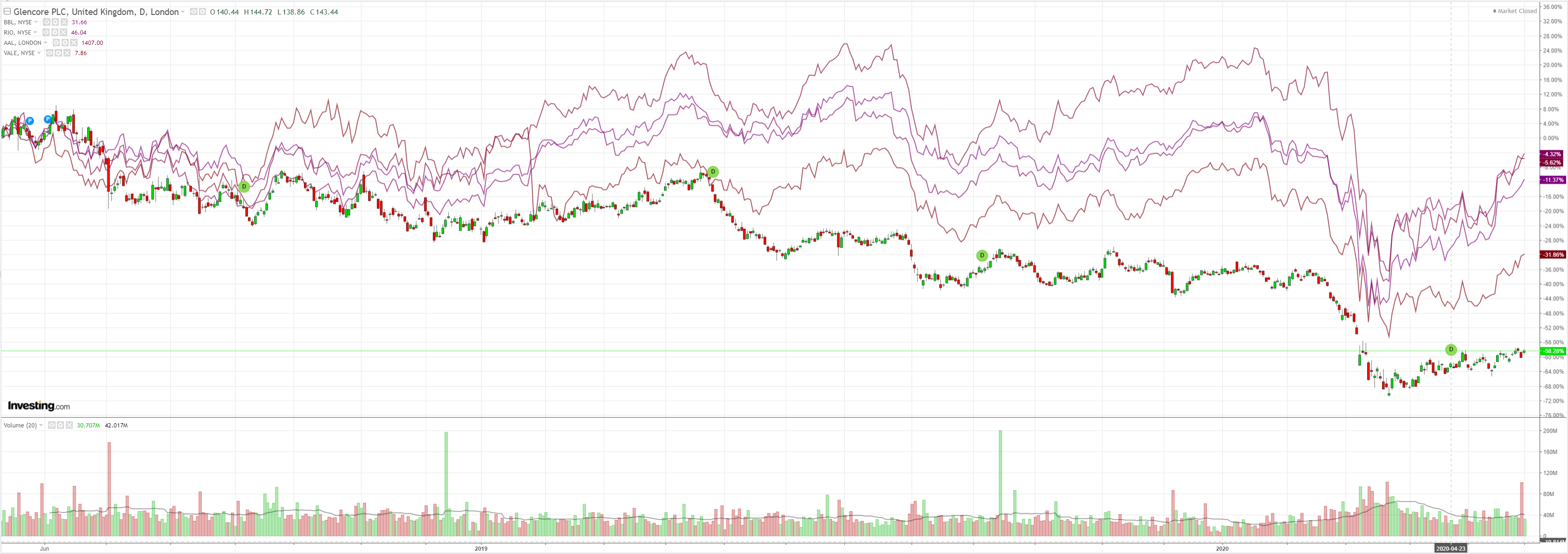

Dirt popped but it is rubbish:

Unless it is Pilbara magic dirt:

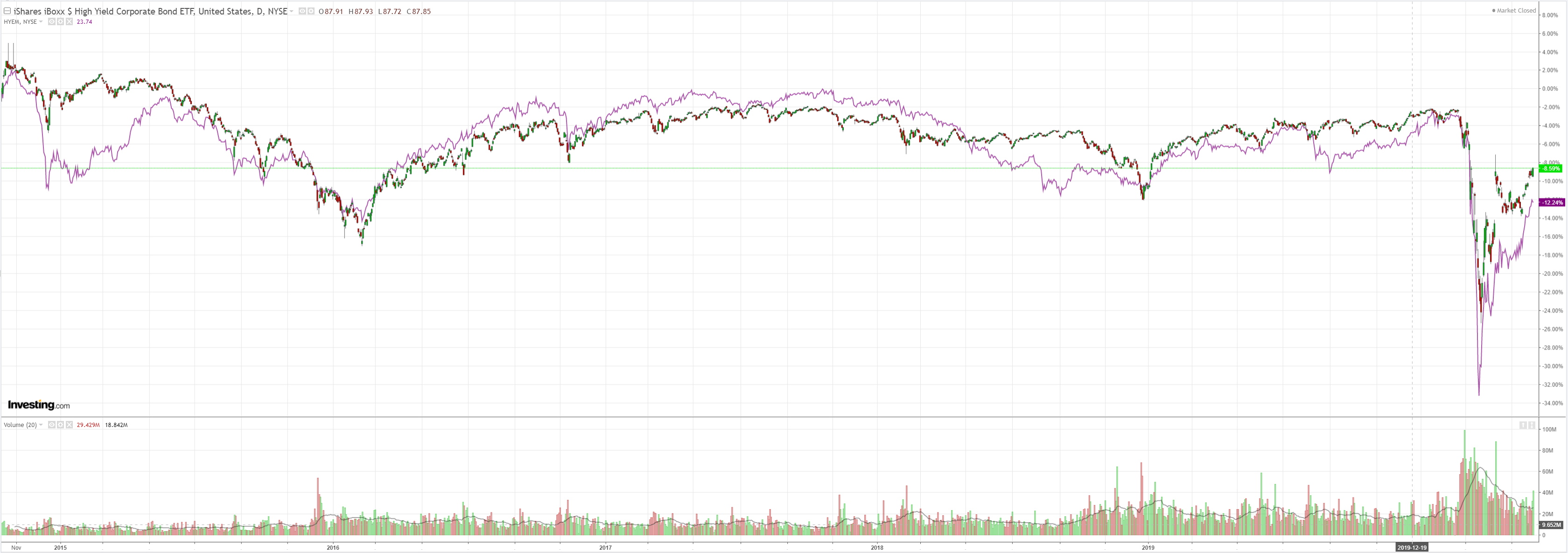

Junk is wildly bid:

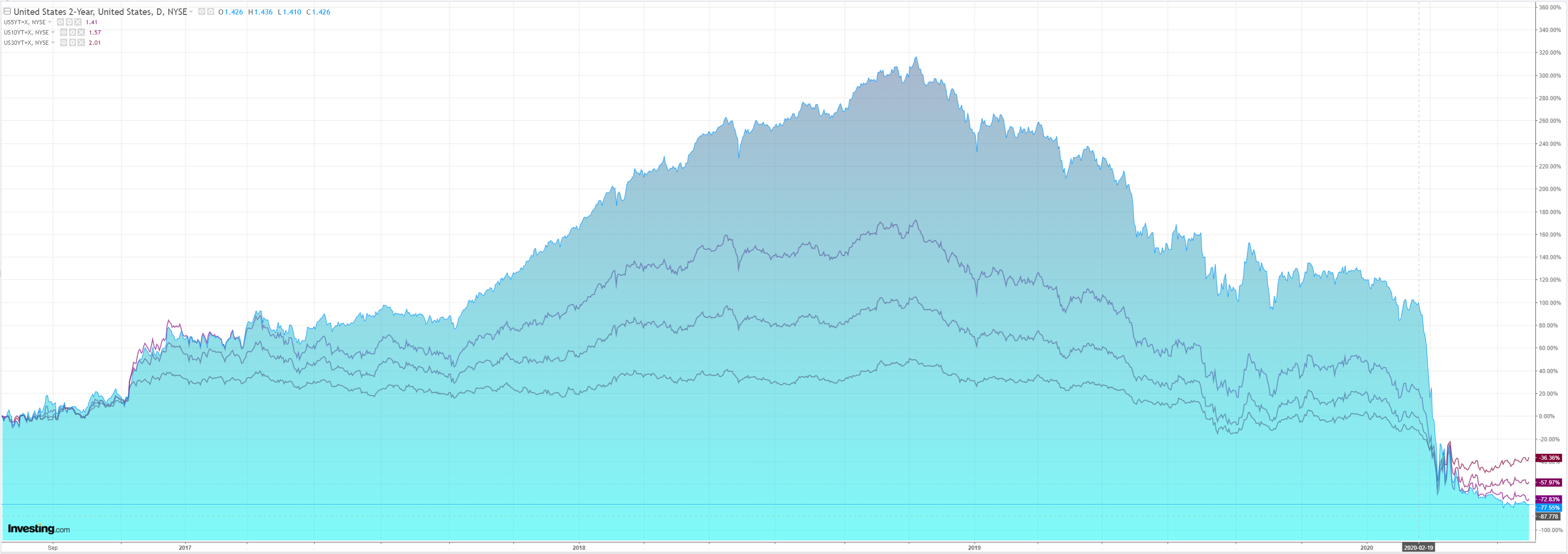

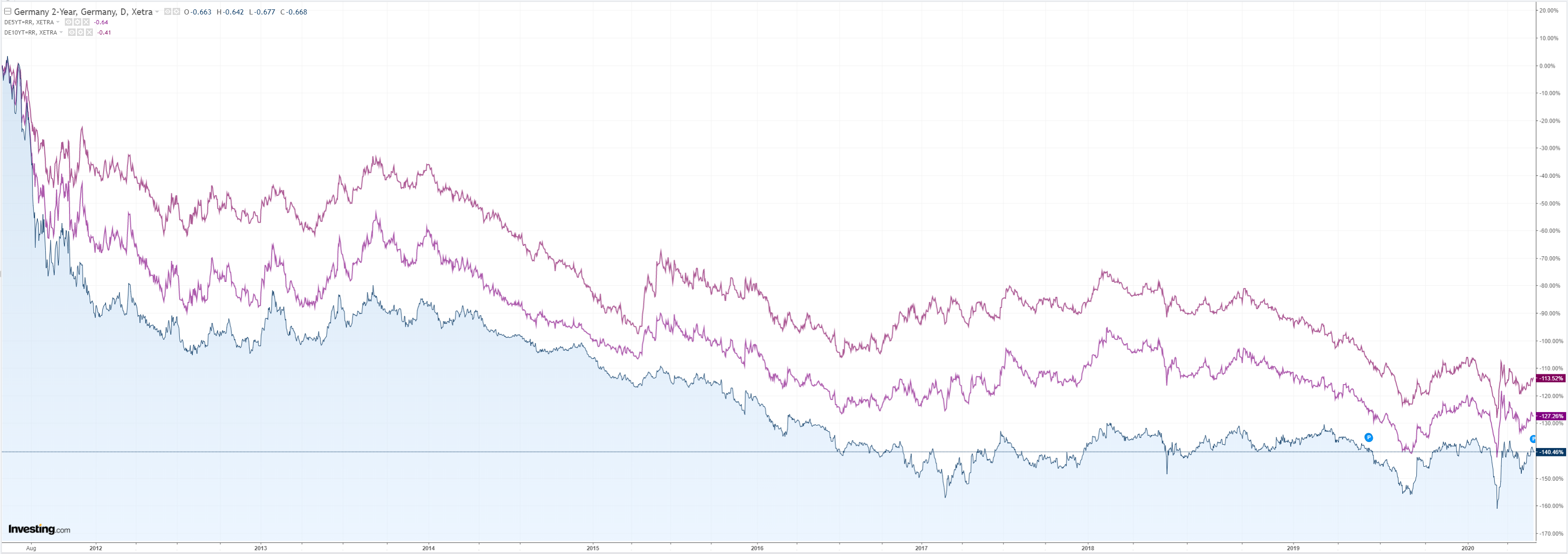

Bonds were soft:

Stocks power on into the great fakeflation:

Westpac has the wrap:

Event Wrap

US May manufacturing ISM at 43.1 was close to expectations (estimate 43.8, prior 41.5); with moderate rebounds in employment (32.1 from 27.5), new orders (31.8 from 27.1) and prices paid (40.8 from 35.3 in April), albeit to still weak levels. Cautious outlooks outpaced positive responses by a factor of two to one.

Eurozone May final Markit PMI was marginally lower at 39.4 (flash 39.5), though Italy showed a more marked rebound to 45.4 from 31.1 in April (est. 36.8). UK rose to 40.7 (est. 40.8, flash 40.6).

Event Outlook

Australia: There are several important releases today, starting with Q1 company profits. The picture for profits is mixed for the opening quarter of 2020. Mining profits are up on higher commodity prices, but non-mining profits have been crunched by the COVID-19 shutdowns. With these effects broadly offsetting each other, Westpac is looking for a flat print. Q1 inventories are also out. Hoarding and panic buying saw suppliers unable to keep up with demand, and it is likely that firms ran-down their inventories in response to the pandemic. Westpac expects a sharp fall of 2.0%, which would subtract 0.7ppts from activity in Q1. Q1 Net exports will follow, and Westpac anticipates that the abrupt drop in import volumes outstripped the fall in exports. On balance, net exports should contribute 0.5ppts to Q1 GDP. For the Q1 current account, higher terms of trade should see the surplus widen to an estimated 6.5bn – however, the net income deficit is a potential wildcard given the large swings in global markets. The final major release will be Q1 public demand, and Westpac expects an increase of 0.6%. In upcoming quarters, spending on health will rise further in response to the pandemic. Apart from data, markets will be watching the RBA’s policy decision announcement. With the RBA continuing to rule out negative rates, the cash rate is set to remain at its current level until at least 2023, but we assess that the bond target will be lifted during 2022.

New Zealand: Westpac expects that dwelling consents fell by 60% over April, a result of the lockdowns that remained in place over most of the month. The Q1 terms of trade are also out, and whilst dairy prices saw a small rise, there were sizeable price falls for meat, seafood, logs and crude oil. Overall, Westpac is looking for a decline of 1.0%.

Europe: May Markit manufacturing PMIs for Germany and the Euro Area will be released.

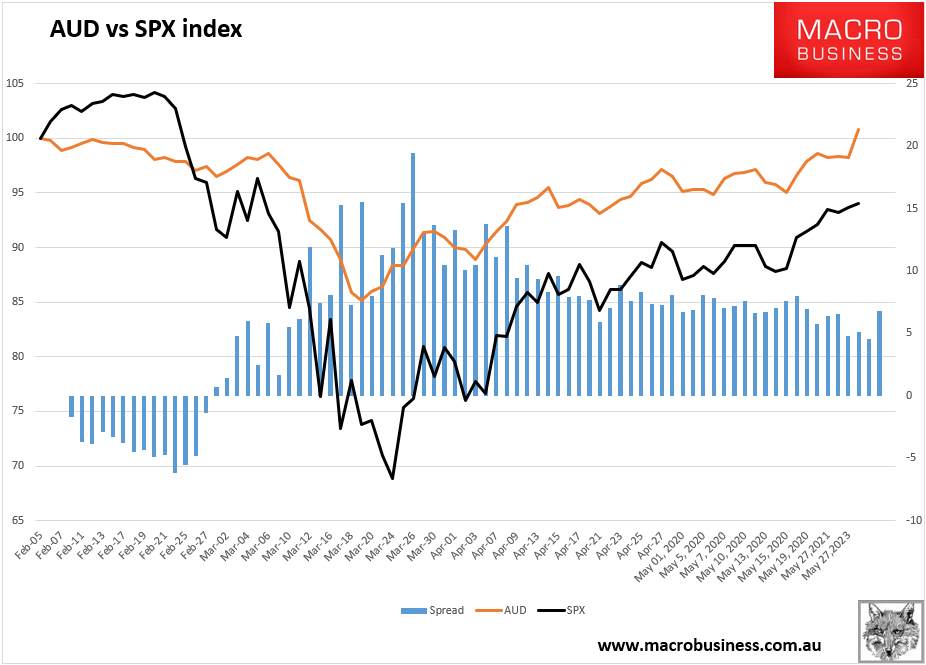

Here’s my SPX vs AUD updated chart:

Alas, what was a reassuring declining trend in the spread has blown out again. The causes are pretty obvious:

- virus outperformance;

- waves of fiscal, and

- iron ore going bananas.

It’s the last point driving things at the moment. Iron ore is off the hook and there is no immediate end in sight. Brazil is sinking into the virus at an alarming rate. Its lockdowns are haphazard so will only prolong the agony, Trump-style. So its iron ore supply will be at risk all year. Despite all of the balderdash claiming the opposite, Chinese growth is once again building-centric with little else likely to take its place as the global economy suffers.

It may look like a post-GFC rerun but it’s far from it so there is only so far that the AUD can get. The local economy is not going to rocket out of the virus. Unemployment is huge. Iron ore flows into the country won’t prompt any investment and precious little income growth. As well, the developed economy growth rebound is going to be to recessionary levels so beyond iron ore and the great fakeflation the global economy is going to stink, which is not AUD favorable. In a way, Australia is being punished for its virus success.

But it is what it is. Australia has the cleanest dirty shirt and iron ore is widening the gap so, for now, it’s all the way with the AUD.