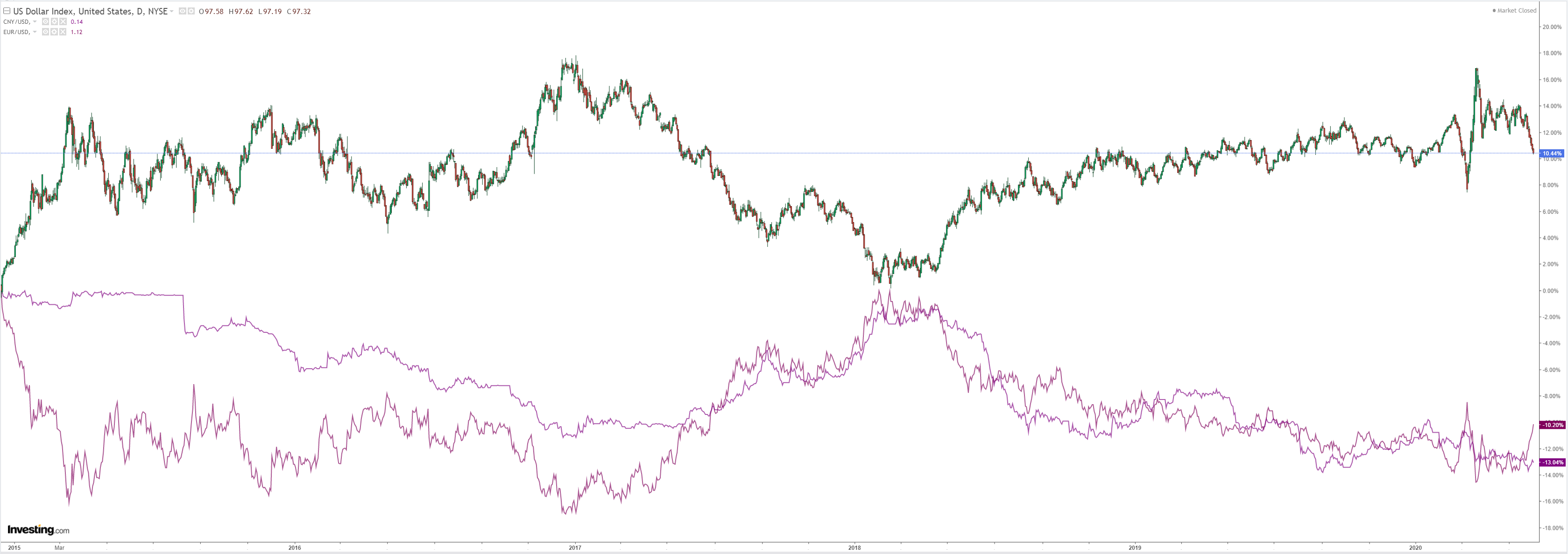

The Australian dollar finally flamed out but it’s not over:

Gold was bashed despite DXY falls. Odd:

Advertisement

Oil took a breather:

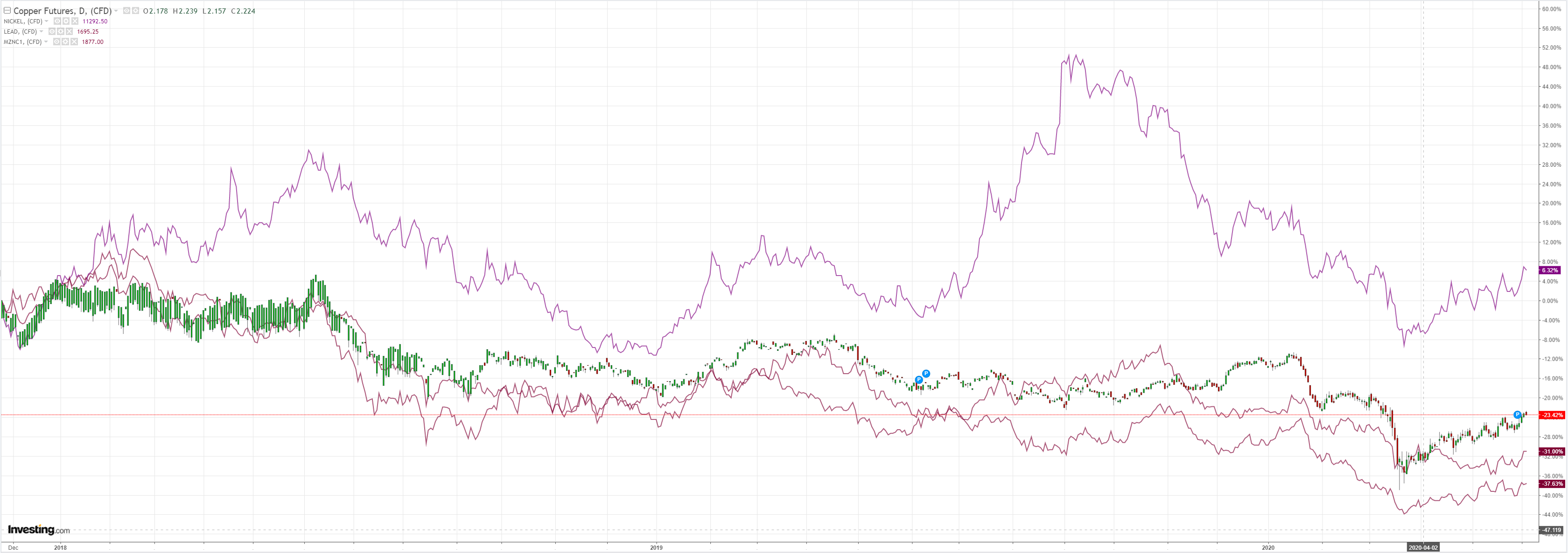

Dirt is still largely uninterested:

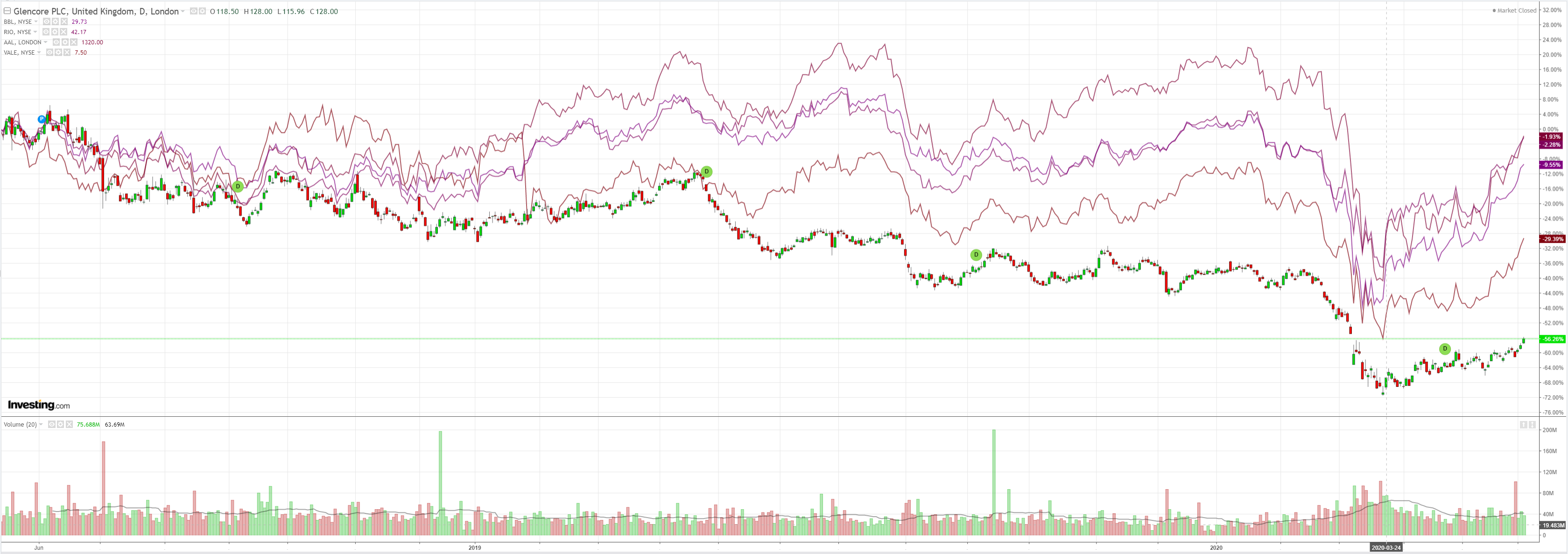

Miners flew on:

Advertisement

Check out EM stocks. Bizarro world as stocks gap towards Nirvana even as they plunge into the virus:

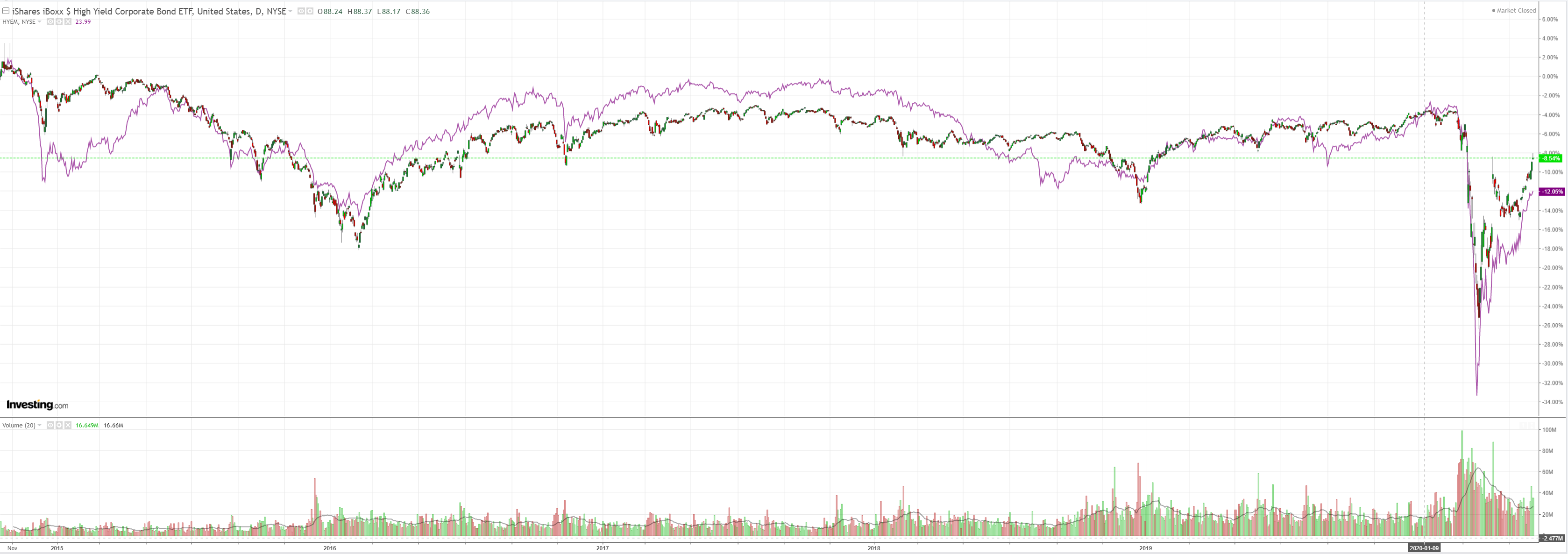

Same for junk:

Advertisement

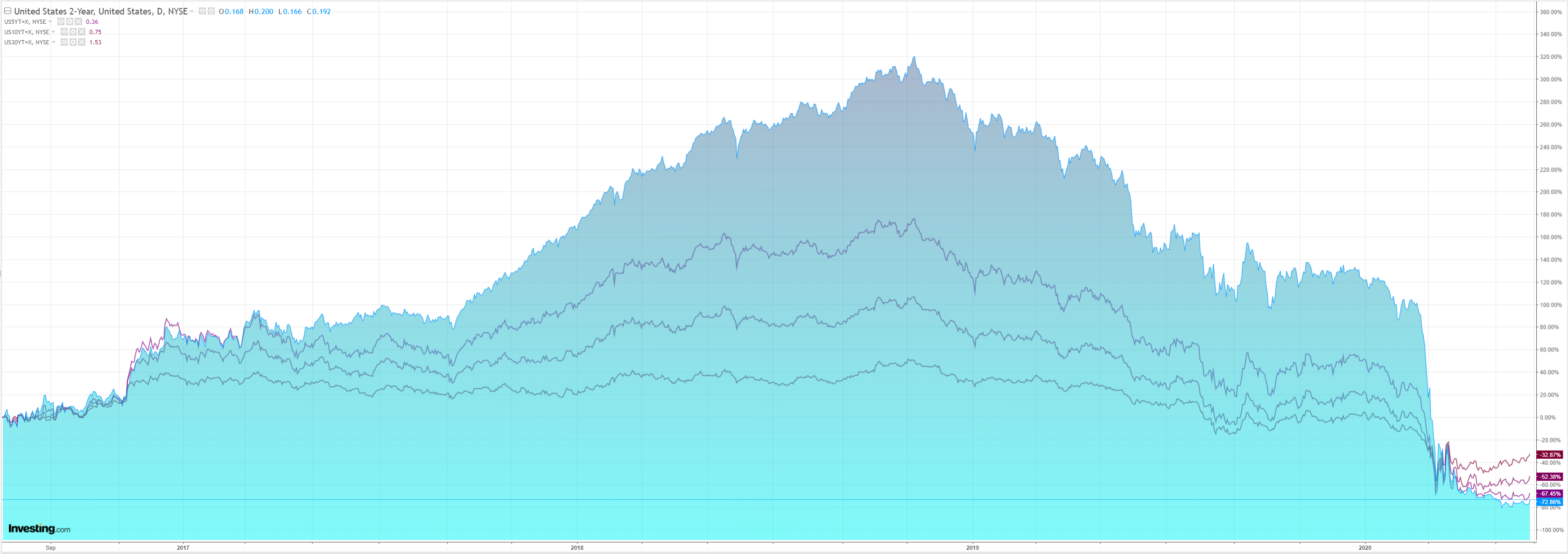

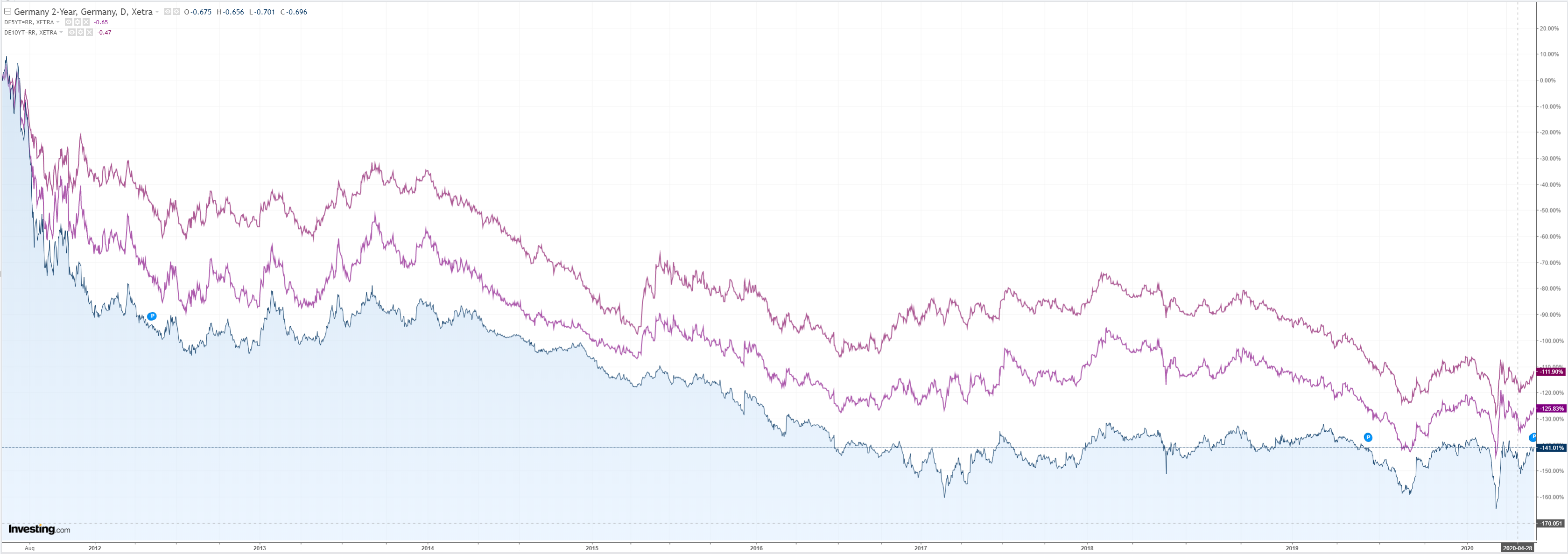

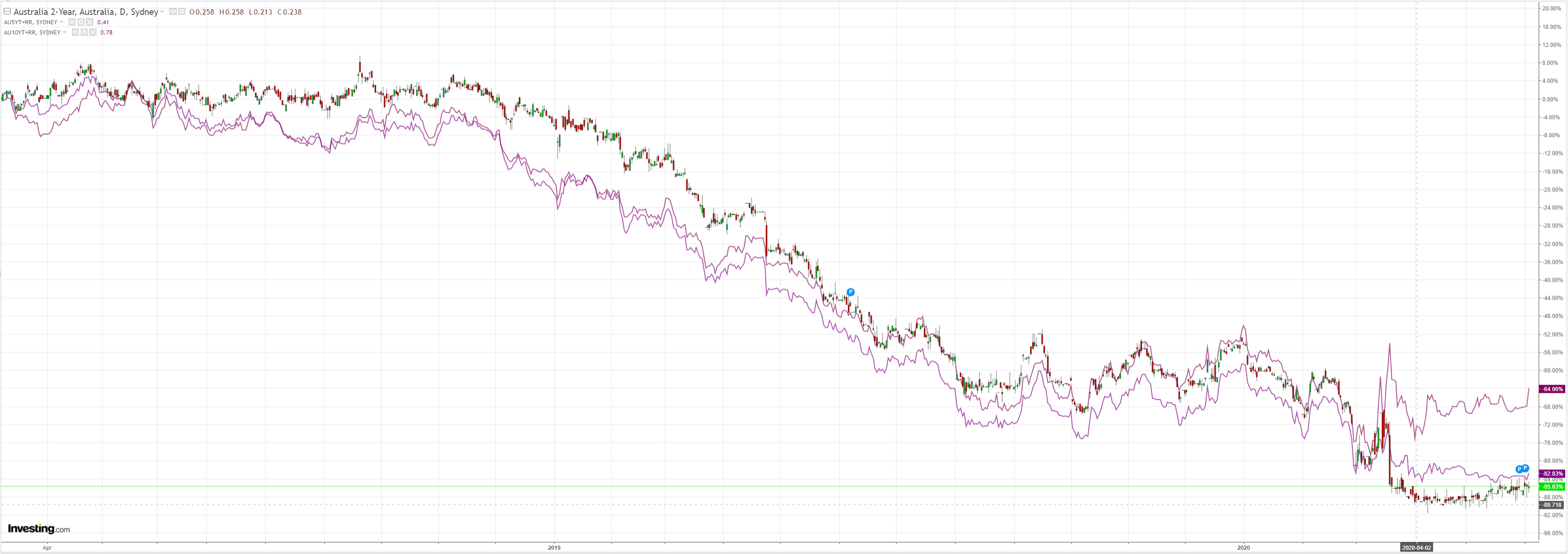

Fakeflation is delivering the bond back-up as expected:

With stocks headed anywhere they like:

I’ve never seen anything like it. We’re accelerating through an entire financial markets cycle in three months.

Advertisement

We’ve had the blow-off, crash and DXY surge, stimulus, reflation and now bond back-up, value rotation and push into EMs as DXY falls all in three months when it should all take three years.

The real economy has absolutely nothing to do with it. This is an entire financial market cycle played out on methamphetamine thanks to the nationalisation of capital markets.

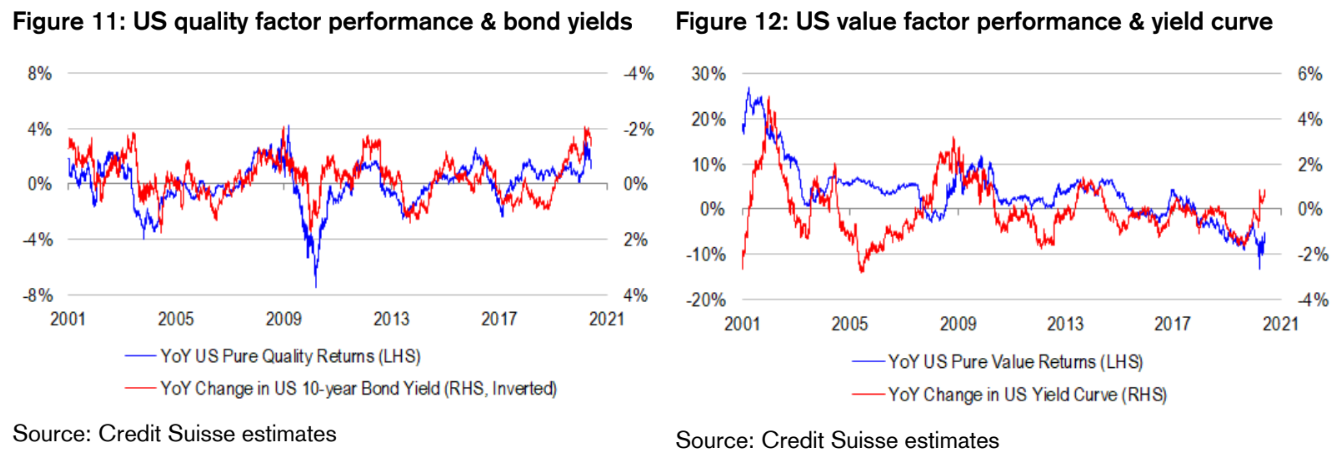

Damien Boey at Credit Suisse sums it up:

Advertisement

Historically, the (real) yield curve is a powerful inverse indicator of correlation risk, and a useful leading indicator of hard landing risk. Specifically, an inverted real yield curve typically signifies heightened correlation risk because of asset price bubbles suppressing bond yields, and this correlation or bubble risk is often “triggered” by an external shock or central bank overtightening, leading to large drawdowns in passive portfolios and corresponding with (if not causing) weakness in the real economy. Only 8 out of 10 times when the real yield curve inverts, do we see a recession around the corner. But 10 out of 10 times do we see correlation risk in portfolios and the real economy rise to dangerously high levels. With all of this in mind, we note that the real yield curve is inverted, but in the process of steepening. The curve is suggesting that correlation risk is dangerously high in part because of central bank intervention, but possibly receding because of hopes that stimulus will work and economies will re-open in earnest. And of course, the global economy is experiencing a recession right now, a low starting point. Typically, when bond yields rise and the curve steepens, we tend to see quality factors underperform with defensive assets and value factors outperform on the improving outlook for cyclicals. But curiously, quality is lagging the net decline in bond yields this year, while value is failing to catch up to the steepening yield curve more recently. Factors are not behaving quite as they should with respect to commonly-followed asset allocation signals, perhaps suggesting that risks are higher than we might think and that crowding remains a problem. Diversification in factors is indeed hard to find. And we are finding it by shorting, rather than buying conventional factor risk premia.

Prompted by the all-powerful electrodes of the Fed, financial markets are dreaming their way through the twitches of a muscle memory financial cycle as the real economy lies broken in a coma.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.