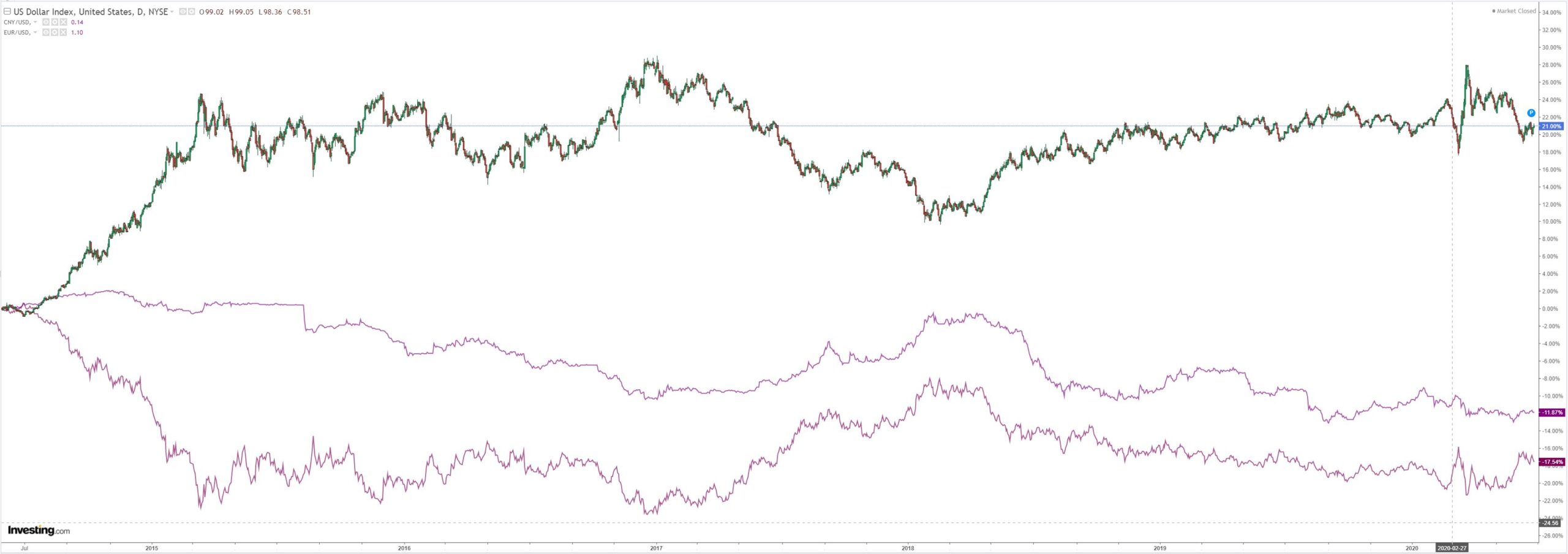

DXY was up last night:

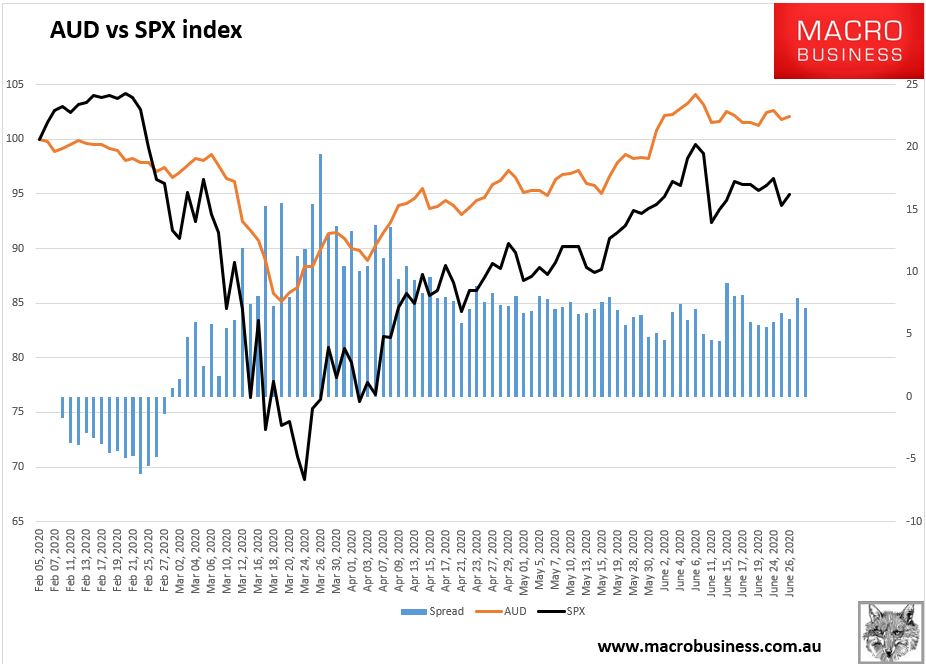

The Australian dollar jumped anyway:

Oil was up:

Gol held the break out…just:

Dirt now has a firming trend:

Miners were up:

EM stocks too:

Junk struggled:

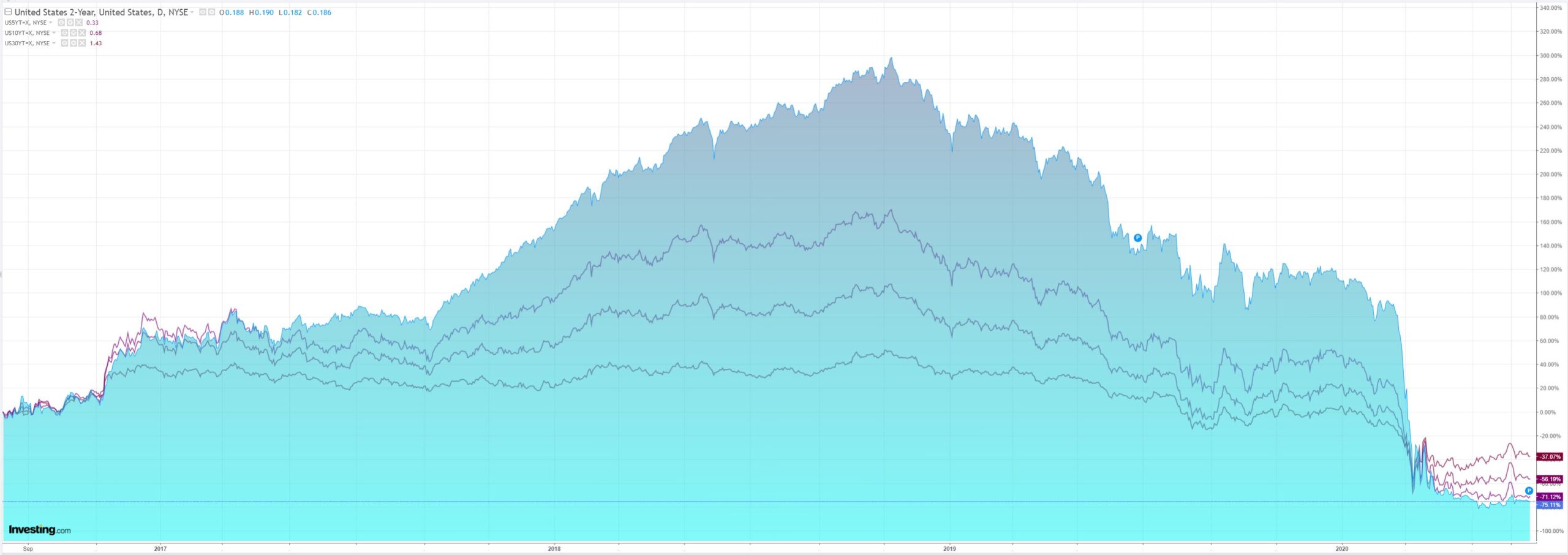

Bonds were bought:

Stocks jumped:

Westpac has the wrap:

Event Wrap

US weekly jobless claims rose 1.48m (vs 1.32m expected), but continuing claims slowed at 19.52m (expected 20.0m, prior 20.29m). May advance good trade deficit widened to -USD74.3bn (est. -USD68.1bn, prior -USD69.7bn). Wholesale inventories fell 1.2%m/m in May, and retail inventories fell 6.1%m/m (est. +0.4%m/m and -2.8%m/m respectively). Durable goods orders rebounded 15.8%m/m in May (est. +10.5%m/m), with ex-transport rising +4.0%m/m (est. +2.1%m/m). The third take on 1Q GDP was broadly unchanged (-5.0%q/q annualised, private consumption -6.8%q/q annualised), though core PCE did tick up slightly to 1.7% from prior 1.6%. Kansas City Fed manufacturing index for June rose to +1. Although the volume of orders rose to +6 (prior -25), new orders and employees remained negative (-8 from prior -25, and -6 from prior -13 respectively).

Event Outlook

New Zealand: Although ANZ consumer confidence has picked up on an easing of lockdown restrictions, the level remains low (prior: 97.3).

China: Negative industrial profit growth (prior: -4.3%yr) hints at further stimulus measures being necessary to support state-owned and private business.

Japan: The market expects a marginal weakening in Tokyo CPI from 0.4%yr in May to 0.3%yr this month as prices fall on subdued economic activity and oil price declines.

Singapore: Industrial production has defied expectations by withstanding the global economic deterioration until now. The market anticipates a fall from grace to -7.1% (prior: 3.6%).

Europe: Recent ECB actions have primed money supply for strong growth. The market expects growth to increase to 8.6%yr in May from 8.3% in April.

US: Income was temporarily boosted by federal payments under the CAREs Act resulting in a strong gain for personal income of 10.5% in April. Both the market and Westpac expect a reversal in May (-6.0% and -4.5% respectively). The opposite is anticipated for personal spending, a robust gain to follow the collapse seen in April under lockdown (-13.6% in April). PCE deflator measures are likely to be flat as oil prices remain soft and economic slack is felt. The final estimate for Uni. Michigan Consumer Sentiment will confirm the uplift reported by the flash estimate for June, as employers restored jobs (prior: 78.9, market f/c: 79.0).

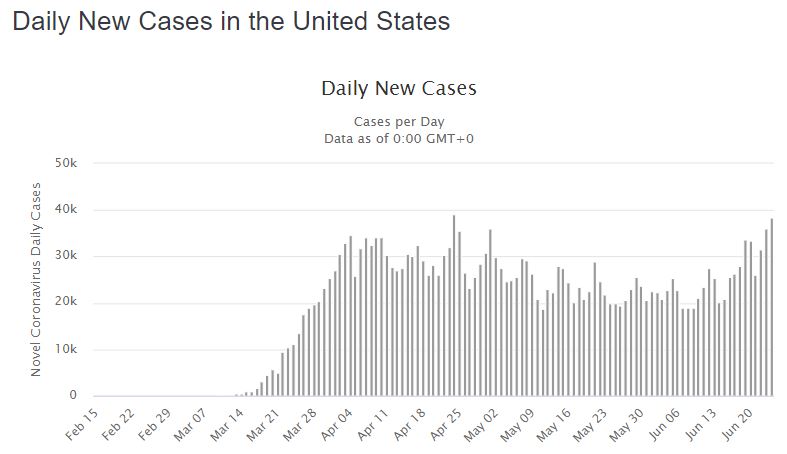

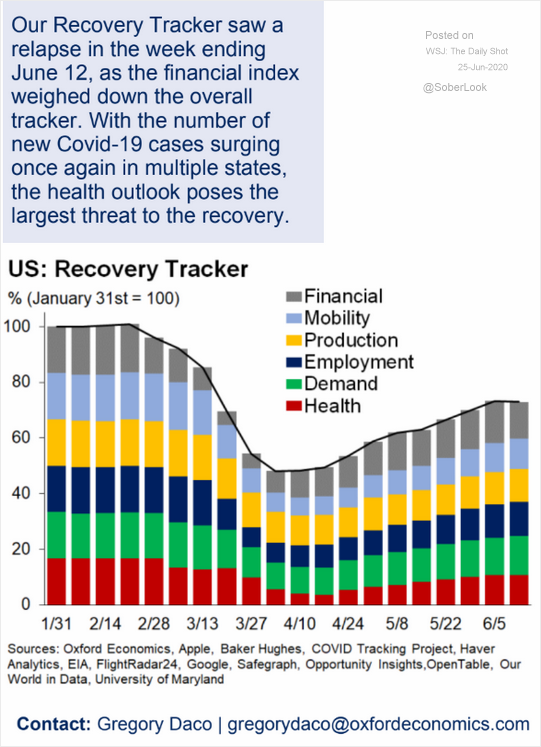

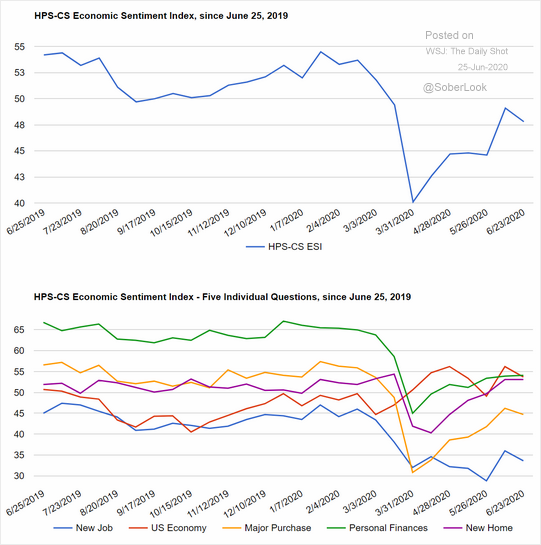

The US recovery has started to slow as the virus runs riot, Apple closed more stores, Florida and Texas “paused” their reopenings:

Let’s not kid ourselves that any of that mattered to the Australian dollar. Only this did:

The depression is worsening so buy MOAR stocks and Australian dollar!