Executive summary. In this article, we explore some key concepts for understanding the unique plumbing of the Chinese monetary system, as well as some of our preferred tools for asset allocation. Our “deep dive” is motivated in part by recent policy announcements by the People’s Bank of China (PBoC) against the backdrop of the COVID-19 shock and escalating trade tensions. But more generally, we find that Chinese asset allocation signals are incredibly useful for Australian investors too, and unsurprisingly so given high business cycle correlations. Also, we note some remarkable similarities between Chinese and Western asset allocation tools, despite clear differences in monetary systems. At a high level, combining an understanding of financial plumbing with long-term valaution, momentum and yield curve signals, generates powerful investment insights in China, just like it does in the West. We conclude by suggesting that the signals are currently leaning against bonds, both in Australia and China, while favouring the commodities complex and AUD. Special thanks to our colleague and friend Michael Yu for his valuable contributions and insights.

Chinese quantitative easing? The PBoC is launching a new credit loan program. The central bank will start buying CNY 400 billion of bank loans made by local lenders to small businesses between 1 March and 31 December 2020, with maturities of at least 6 months. The move implies interest-free loans to small banks based on 40% of their lending to small firms, and is designed to encourage them to lend as much as CNY 1 trillion. Importantly, the new loans will not require collateral and guarantees, removing a key obstacle for such borrowers, although banks will need to buy back their loans when the program ends (unless of course the PBoC extends it). The PBoC will also provide 40 billion yuan in re-lending funds to conduct interest rate swaps with local banks through a special purpose vehicle, which it says will help banks extend loans with a principal value of CNY 3.7 trillion. Like the Fed’s commercial paper purchasing program, the PBoC will not be the ultimate bearer of credit risk. The overall program is small, and intended to be temporary. Yet many commentators are debating whether or not it represents quantitative easing (QE) proper in China, and doubt how temporary the arrangements will be. Certainly PBoC Deputy Governor Pan believes that the program is different from QE by “nature and scale”. But we think symbolically, it could be more significant, because it demonstrates that the PBoC is exploring creative options to deal with the COVID-19 crisis, trade war escalation and constraints on the Chinese monetary system from the exchange rate peg regime. Interestingly, after the announcement of the new program, we note that Chinese government bonds are selling off.

The wrong question to ask in the context of China. Clearly, Chinese authorities are prioritizing small business financing, to prevent a wave of defaults in this crisis, with all of the the job, production capacity, and bank loan losses therein. At the very least, the cost of financing for small businesses will fall and potentially, their access to finance will improve too. Because the program is small, finite and targeted, it looks like a “fine tuning” strategy to preserve businesses, rather than a “nuclear” stimulus option. Therefore, the new loan purchase program makes a lot of sense, and fits well within the parameters of President Xi’s current economic agenda. All of this said, we think there is potentially a lot more to the program than meets the eye. And related to this point, we also think that the question of whether or not the program represents QE is a largely irrelevant one to ask. For what it is worth, the PBoC package looks a lot more like the European Central Bank’s (ECB’s) targeted long-term repo operations (TLTROs), or the Bank of England’s (BoE’s) funding for lending scheme (FLS), where banks struggling to obtain liquidity are provided it through the effective securitization of their loan books and asset swaps with the central bank. But while TLTROs and FLS looked like rather limited or “half-hearted” easing options for the ECB and BoE, and were perceived by investors as well short of “full-blown” QE, the counterpart operation in China could actually prove quite effective. Note that in China, the central bank does not pursue a policy of targeting a cash rate, because it targets the exchange rate instead. And as a result of the exchange rate peg, foreigners are provided with any and all CNY liquidity they want and need, typically flooding the system. Consequently, domestic monetary policy is all about managing quantities of money in the system rather than prices. It always has been. There has been no sudden shift to quantity targeting from price targeting, like there arguably has been in the developed world, as central banks have hit the zero bound on rates. Traditionally, the PBoC has preferred to ration reserves through reserve requirement ratio (RRR) changes, with a view to controlling bank lending. But now that the PBoC has launched its credit loan program, we think there may have been a subtle extension to reserves management, reminding us that Chinese monetary policy makers have been very alert to plumbing issues in their system, and have been actively exploring different ways to alleviate otherwise binding constraints.

Loan purchase program is like a targeted reserve requirement ratio cut. In modern monetary systems, bank loans create deposits – not the other way around. In Western systems, the availability of interbank reserves to satisfy regulatory requirements is not a binding constraint on lending, because the central bank targets a cash rate, and therefore promises to provide any and all reserves that banks need to defend their target rate. In other words, loans create deposits and banks seek out reserves afterwards with the understanding that they will always provided by the central bank if needed. Banks do not first check whether or not they have adequate reserves before lending. When Western central banks run conventional QE, they engage in an asset swap with the banks, giving them excess reserves in exchange for bonds on banks’ balance sheets. However, providing excess reserves to the banks does not alleviate a binding constraint on lending, and therefore does not directly stimulate lending. Indeed, banks cannot, and do not lend out reserves. At best, QE lowers long-term bond yields, boosts asset prices and may indirectly stimulate borrowing to the extent that long-term bond yields matter. In China, the plumbing of the system is quite different to the West. The PBoC does not promise to provide any and all reserves that banks want, because it does not target a cash rate. Consequently, banks need to think twice about reserve availability before lending. Loans still create deposits, but reserves are not guaranteed by the central bank. The availablity of reserves is a binding constraint on lending unlike the case in Western economies. Indeed, reserve rationing through RRR changes is a very effective way for the PBoC to control bank lending. And with the introduction of the credit loan program, we see an effective easing of reserve constraints, because loans create deposits, and the loans themselves can be swapped back with the PBoC for reserves if banks so require them.

The context of capital outflows. The PBoC’s effective loosening of reserve supply is especially meaningful against the backdrop of capital outflow and constraints on the monetary system imposed by the CNY/USD exchange rate peg. When the Chinese economy experiences a capital outflow, the PBoC is the only entity on the other side of the transaction. It can either choose to let the price of money – the CNY/USD exchange rate – drop, or the quantity of money – CNY denominated deposits – drop instead. If it chooses the former option, the risk is that capital outflows intensify on the signal that the CNY/USD is overvalued. On the other hand, if it chooses the latter option, it reduces both money and reserve supply in the system. Foreigners no longer want CNY denominated deposits, and so the PBoC effectively deletes them from the system. But the cost is that reserves are also drained, with negative flow on effects for system liquidity and credit availability. In this context, we believe that the PBoC’s credit loan program is an attempt to break the exchange rate nexus amid escalating trade tensions and increasing capital outflow. Note that trade tensions are not just causing a shortage of USD liquidity for Chinese entities (ie if the US is a smaller net importer of goods and services from China, it is also a smaller net exporter of USDs to pay for them). They also exert downward pressure on the CNY/USD which in turn causes a shortage of CNY liquidity if the PBoC attempts to sterilize. But if the PBoC can engineer a simultaneous uplift in CNY liquidity and bank lending in the system through RRR cuts or the credit loan program, it can counteract these effects, while the Fed via its special repo facility can help the PBoC with China’s immediate USD liquidity shortages. To be sure, it is possible that attempts by the PBoC to expand money supply could be perceived as dilutive of the CNY, exacerbating valuation concerns among investors and therefore capital outflows. But the good news for the PBoC is that whatever it and fiscal policy makers are doing to boost Chinese money supply, the Fed and US Treasury are doing even more of to boost US money supply. Therefore, there is simultaneous dilution of CNY and USD money supply, and we think that the effects are ambiguous, rather than outright negative for the CNY/USD. Put differently, the PBoC can get away with a certain degree of money supply expansion.

Look through to inflation, or the bad news driving the policy change? The PBoC says that the new credit loan program is small, finite and temporary. But if it ends up bigger than stated parameters, it could actually be quite supportive of growth and inflation, provided that there are sufficient credit worthy borrowers in the system. On the other hand, sceptics will argue that either the program is too limited to cause a meaningful difference, or that if certain small banks are finding themselves short of interbank reserves, such that the PBoC needs to explicitly deal with the problem, these banks could well be seeing substantial deposit flight because of public concerns about solvency. The question therefore is whether we should focus on the reflation potential of the new measures, or the bad news sitting behind them. History tells us that more often than not, we should look through stimulus to the reason behind it, largely because of the complicating effects of capital outflows. But this time could be different, because Chinese policy makers are not alone in their attempts to engineer stimulus.

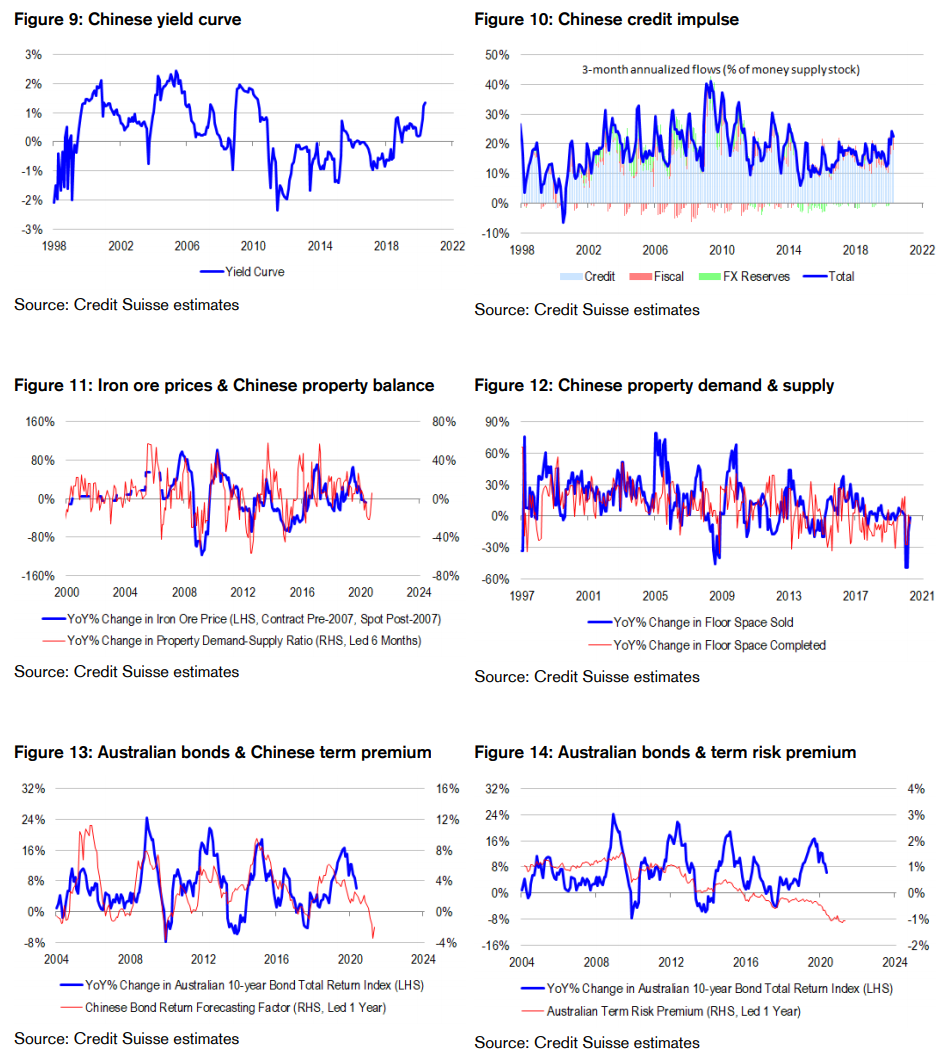

Bonds poised to sell off regardless. We are taking a “glass half full” approach to Chinese stimulus for now. But whether stimulus works, or capital outflows prevail, we think that Chinese government bonds are poised to sell off. Effective stimulus could trigger reflation, which bonds are not necessarily priced for. On the other hand, heavy capital outflows could drain the system of liquidity to the point that interbank rates spike and bond yields with them. Either way, there are fundamental reasons for bonds to sell off. But we err on the side of optimism, because the Chinese yield curve – defined here as the spread between 10-year bond yields and 3-month interbank rates – is one of the steepest in the world, consistent with growth and recovery ahead. And part of the reason why the curve is steep is because the PBoC is succeeding in combating the liquidity drain from capital outflows, as evidenced by the low and controlled level of short-term interbank rates.

Chinese term risk premium is deeply negative. Mathematically, we think that Chinese government bonds are predisposed towards a sell off, because the term risk premium in bonds – the spread between long-term bond yields and the neutral rate – is negative. Never mind how we process the newsflow – the issue is that bonds are simply too overbought and too expensive. We model the term risk premium in China the same way we model it for G3+ economies. The seminal work of Cochrane and Piazzesi (2002) teaches us that it is possible to predict a meaningful proportion of year-ahead returns on long duration bonds (ie capital growth and running yield), using only today’s cross section of bond yields. More specifically, a non-linear ,or tent-shaped combination of today’s 2-, 5- and 10-year bond yields, that places maximum positive weight on the 5-year yield and low or negative weights on 2- and 10-year yields, is able to predict more than 40% of year-ahead bond returns across all major markets over very long sample periods. Non-linear factor loadings are critical to make the bond return forecasting factor sufficiently uncorrelated with the level of interest rates and the slope of the yield curve. And subsequent research from Kim and Wright (2005) reveals that the Cochrane and Piazzesi bond return forecasting factor is very highly correlated with their estimates of the term risk premium, and indeed, is functionally equivalent but for scaling. We find that Western modelling frameworks of the term risk premium carry over very well to China. A tent-shaped combination of today’s 2-, 5- and 10-year Chinese bond yields is able to predict more than 70% of the variation in year-ahead bond returns since 2004. Some might be surprised at this result considering how different Chinese and Western monetary systems are. But nevertheless, the data and historical relationships speak for themselves. And right now, the Chinese bond return forecasting factor, or variant of the term risk premium, is deeply negative. It is coming off its most negative levels since the 2008 global financial crisis (GFC). Bonds are priced to sell off, and potentially quite sharply. Therefore, it does not surprise us either fundamentally, or technically, to see bond investors react negatively to recent PBoC policy announcements.

Risk on for Chinese asset allocators? A bond sell off, curve steepening event should be positive for equities over bonds, especially if growth recovers in earnest. However, the problem is that at current through-the-cycle valuations, Chinese equities are priced for lower returns than bonds over 10-year horizons – that is, the Chinese 10-year equity risk premium is negative. If it is always the same uncertain future we are buying, the only thing that really matters for long-term returns is the “through-the-cycle” valuation starting point. High (low) valuation should be consistent with low (high) future returns – and indeed, we find this to be the case fo China when we value the A-share market using the market capitalizaton-to-GDP ratio. At current levels, the A-share market is priced for 0.7% annualized returns on a 10-year horizon, while bonds are priced for 2.9% annualized returns. From this valuation starting point, GDP would need to rise significantly to erode the valuation premium and make equity risk more palatable. So for a little while, it might pay to play the narrative that higher yields are a sign of good growth – but ultimately, valuaton will become a binding constraint. Much like the US, China has the dubious privilege of negative term and equity risk premia – a highly vulnerable starting point for passive investors and asset allocators, because both asset classes are at risk of selling off together, creating correlation risk. The question then becomes one of whether there are alternative asset classes with positive risk premia, or superior return outlooks to both bonds and equities. We think that there are. Property and commodities naturally come to mind – but commodities probably have the edge. If property does well, and reflation takes hold, commodities will likely do well too. And if property does poorly, in part because of liquidity drain from capital outflows, commodities may still offer some protection against currency devaluation risk.

Follow Chinese investors seeking protection against a bond sell off. We find that Chinese asset allocation signals are highly relevant for Australian investors, in part because of strong business cycle correlation. One of the most fascinating historical relationships we come across suggests that the Chinese term risk premium does a better job of predicting Australian 10-year bond returns than the Australian term risk premium, as measured by policy makers! And of course, Australia is a major beneficiary of any upturn in the commodities cycle. We think that Australian investors should follow Chinese asset allocators to a degree by selling long-duration bonds, and taking constructive positions in the commodities complex and the commodity currency AUD/USD. To be sure, RBA QE is a complicating factor for bonds – but we simply do not see much more upside to bonds from current valuation levels. And on the long side of the trade, even if we encounter the bear wing of China’s bond sell off related to illiquidity, the risk could be absorbed by currency. USD-denominated commodity prices could be volatile pending CNY/USD movements, but the AUD/USD could also fall acting, as a buffer for Australian investors. Or alternatively, the AUD/USD could simply rise as Chinese residents seek out alternative safehavens. Either way, there is some protection for Australian investors in a bearish scenario from holding long commodity and AUD/USD positions together, and clear payoffs in a reflation scenario. If nothing else, the optionality is valuable. Finally, it is an open question as to whether or not Chinese investors take a more constructive view of Australian property in the circumstances. But even if they do, COVID-19 border restrictions could limit the upside potential for now. To position for this set of risks within the ASX 200, we advocate an overweight resources position funded out of crowded quality and defensive names including selected A-REIT, consumer staple and healthcare stocks.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.