The Australian Prudential Regulatory Authority’s (APRA) weekly update on the Morrison Government’s early superannuation release policy reveals that another $1.2 billion was pulled from Australia’s superannuation pool, raising total withdrawals to $17.1 billion:

As you can see, 2.3 million applications for early release have been paid averaging $7,492 per withdrawal.

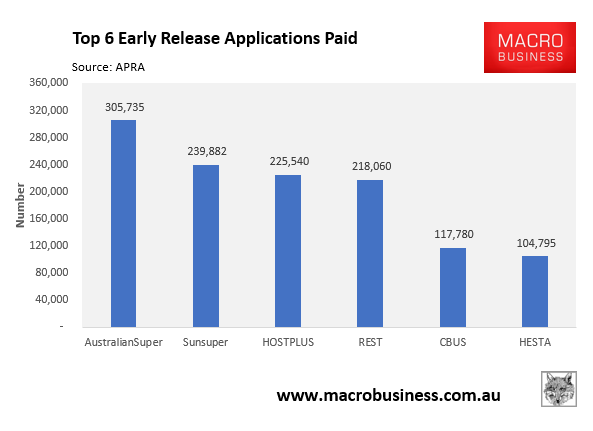

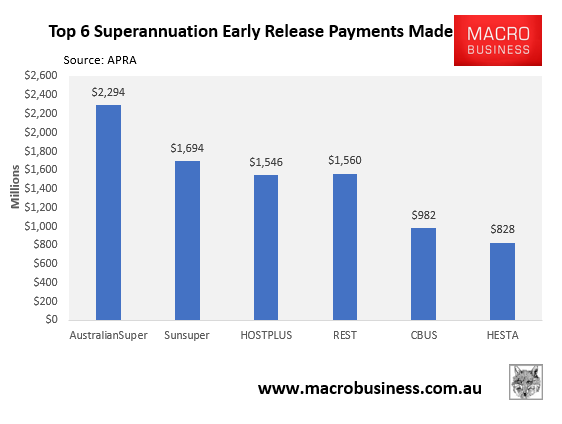

Looking at the breakdown, you can see that industry funds comprised the top six for withdrawals, accounting for just over half ($8.9 billion) of total early redemptions:

Advertisement

Under the early super release policy, another $10,000 is permitted to be withdrawn from accounts from 1 July. Accordingly, overall withdrawals could balloon.