Well that escalated quickly! Over the past few weeks, tensions have simmered among global leaders over the causes of and responsibility for the COVID-19 outbreak. Despite collective efforts to find a cure or vaccine for the virus, it seems that a comprehensive medical solution has not yet been found, and politicians have sought out different lines of inquiry instead. Adding fuel to the fire over the past few days, we have seen some significant developments in China and for US-China relations. First, the Chinese Communist Party (CCP) announced at the National People’s Congress (NPC) that they were abandoning a numerical GDP growth target for 2020, breaking with decades of party planning habits. Second, they announced that they were preparing to launch more fiscal stimulus, with deficit spending to eclipse 3.6% of GDP. Third, authorities announced intentions to “perfect” Hong Kong security laws. Specifically, they planned to bypass the Hong Kong legislature, and to impose laws to ban “treason, secession, sedition and subversion” to deal with political dissent, “terrorism and foreign influence”. In response to China’s plans, US lawmakers have threatened retaliation. For example, US Secretary of State Pompeo has delayed an annual report on whether the city of Hong Kong still enjoys a “high degree of autonomy” from Beijing, stating that he is “closely watching what’s going on there”. White House economic adviser Hassett has insisted that the US government is “absolutely not going to give China a pass” and is already considering any and all forms of economic punishment. Hassett has also warned about the risks of Hong Kong ceasing to be a regional financial centre, and of significant capital flight from the city to the detriment of economic growth. Several US senators have put forward legislation to punish Chinese entities involved in enforcing the proposed new security law in Hong Kong and penalizing banks that do business with those entities. The Department of Commerce has said that it will sanction 33 Chinese firms and government institutions over the treatment of minority groups in Xinjiang. And finally, US President Trump has suggested that he will address the Hong Kong situation “very strongly” if China actually does follow through with new security laws.

Extremely challenging times for China. Chinese President Xi and his regime has had to contend with some serious challenges of late. First, economic growth has weakened to its worst cyclical pace since the 1960s, and to a slower trend pace than observed during the combined Deng, Jiang and Hu eras. Indeed, growth has become so volatile and weak recently, that the CCP has abandoned a GDP growth target for 2020, and replaced it with an unemployment target, breaking with decades of party planning tradition. Second, non-economic targets like health security have been jeopardized by the emergence and spread of COVID-19. Third, international relations with countries like the US have deteriorated significantly amid trade and technology wars, increasingly hawkish policy makers, and more recently, the pandemic. Fourth, Hong Kong protests have gone on for more than a year, interrupted only by the threat of COVID-19, becoming the longest period of civil unrest in broader China since the Mao era.

Battleground Hong Kong. In the circumstances, we can see how a quick win for the CCP in Hong Kong, against a perceived threat to sovereignity would be a welcome development. But the US is not acquiescing. On the contrary, hawkish US officials seem to be doubling down on their positions from recent trade and technology disputes. But in so doing, they could well force a situation where China walks away from Phase I of the trade deal with justification, setting the world down a path of more uncertain and volatile economic growth and geo-politics.

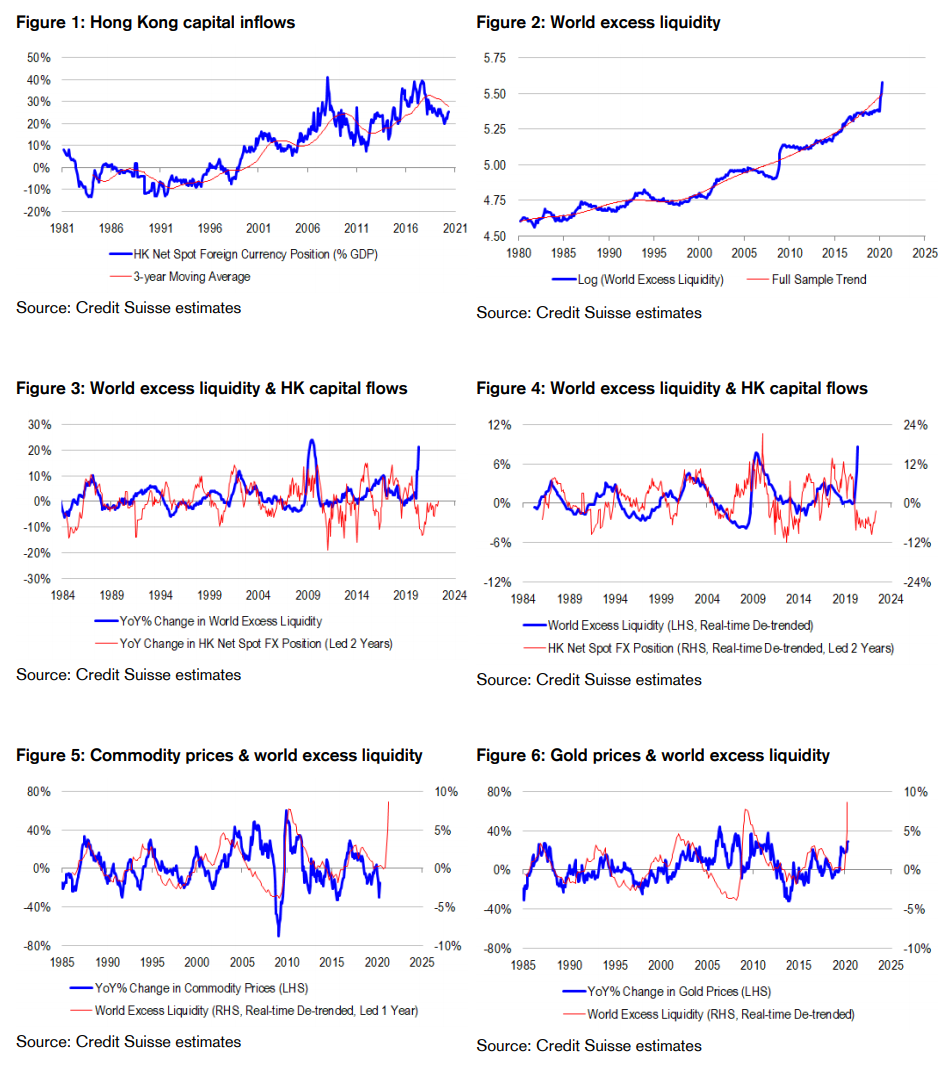

Those who forget history are doomed to repeat it. The history books teach us that trade wars and currency devaluations are “beggar thy neighbour” strategies. They might make sense from the perspective of individual countries, but nevertheless represent a co-ordination failure among countries, achieving inferior collective outcomes. It seems that policy makers everwhere are caught in this “prisoners’ dilemma” in a post-global financial crisis (GFC) world where mutual growth seems either unachievable or unattractive or both. They are responding to incentives the same way as their predecessors, even though they have the benefit of hindsight. To be sure, the global monetary architecture is quite a bit different now to what it was a generation or so ago. But even so, trade wars are not a positive development for the world. And this is where Hong Kong and recent developments are particularly interesting. We note that while Hong Kong is small in GDP terms, its significance as a financial and trade hub is far greater. The port city is at the pinnacle of trade, geo-political and capital flow developments around the world, and arguably, always has been since colonialism. What we find particularly noteworthy is that capital inflow into Hong Kong, as measured by the banking system’s net foreign currency spot position, is not only correlated with world excess liquidity – but actually leads it by several years. Indeed, since the early 1980s, year-ended growth in Hong Kong’s net foreign currency spot position is 30% correlated with year-ended growth in world excess liquidity in up to two year’s time! The tail seemingly wags the dog. This lead-lag, back-to-front relationship suggests that should Hong Kong experience large capital outflows after a brief period of recovery in recent months, we should also expect to see a peak in the global liquidity cycle, to the detriment of world growth. Surely no one really wants this outcome, potentially so soon after a very rough start to 2020! But alas, incentives are what they are, historical lead-lag relationships take time to work themselves out, and there will always be those that argue that “this time is different”. There are always reasons to ignore or defer our history lessons.

Revisiting the Asian “savings glut“. The first thing that comes to mind, when examining the link between Hong Kong capital inflows and world excess liquidity is the Asian “savings glut” theory famously enunciated by former Fed Chair Bernanke in 2005. According to this theory, the supply of saving constrains the credit creation process. Within the US, there is not enough saving to fund loan demand. Therefore, the saving needs to come from elsewhere. And because Asian economies have policies and demographics consistent with excess saving, they can provide a source of financing for the US economy. More specifically, Asian central banks channel excess saving into US Treasury and mortgage-backed security (MBS) purchases, artificially lowering bond yields and borrowing costs, and funding US household borrowing. The more the US consumer spends and borrows, the more Asian exports rise and the more Asian savings rise to fund the US consumer in a virtuous circle. To the extent that Hong Kong’s net foreign currency spot position is a proxy for excess Asian saving, and world excess liquidity is really a proxy for global debt-to-GDP adjusted for certain forms of central bank behaviour, we can see why one might lead the other – why the tail seemingly wags the dog. More saving in Asia eventually fuels more borrowing in the West, supporting global growth with a delay.

De-bunking the Asian “savings glut” in favour of a “capital glut” story. We respectively disagree with the Asian “savings glut” thesis at a conceptual level. We think that the story is not about Asian saving enabling US credit creation, but rather, US credit creation enabling Asian saving in USDs. Some might argue that we are “splitting hairs”, but in our view, the nuance matters in understanding how the Hong Kong situation might or might not have immediate global implications. In the first place, note that in a world without trade, Asian entities do not bring USDs to the table to fund the US Treasury or US private sector borrowing. They only bring with them their CNYs, JPYs, HKDs, SGDs and the like, which are not useful to Americans in need of USD financing. Secondly, note that deposits do not create bank loans or finance fiscal deficits in Western economies. Rather, bank lending and fiscal deficit spending create deposits. Thirdly, USDs are commonly used outside the US to settle trade transactions and even finance borrowing. And when we factor trade into the equation, whenever Asian exporters sell goods and services to the US, they are paid in USDs. Putting all of the pieces of the puzzle together, Asian trade surpluses reflect the accumulation of foreign currency saving, first enabled by the credit creation process in the West. This foreign currency saving might be parked into US Treasuries, supporting lower bond yields. It might just be parked into cash. Alternatively, it might be used to purchase US assets, such as stocks, credit and property. But regardless what choices the Asian holders of USDs make, someone has to hold USD cash, because the banking system and fiscal policy makers force it upon the system. In the first instance, it is excessive credit creation in the US which creates a glut of capital which then contributes to higher asset prices directly, and lower bond yields as private sector debt serviceability becomes a bigger concern. In the second instance, Asian holders of USDs might exacerbate some of these effects in their portfolio choices – but they are certainly not the primary cause of them. This said, perhaps the second round effect is becoming larger through time as Asian economies grow significantly larger, perversely enabled by the USD hegemony. And perhaps this helps to explain why USD foreign currency saving in port cities like Hong Kong leads the cycle in world debt-to-GDP and our preferred measure of world excess liquidity.

The myth and reality of “crowding in”. Anotherone of the implications of Asian “savings glut” theory is that without excess saving from Asia, US government, household and corporate sectors would effectively compete for funds, crowding each other out. We think that crowding out is a myth, because saving is not a constraint on borrowing in modern monetary systems. But this is not to say that there is no such thing as crowding in, and crowding out effects in different systems. Specifically, when a country chooses to peg its exchange rate to another currency, it adds a different set of constraints to its system and monetary policy. Its central bank has to give up control of interest rates in favour of the exchange rate target. And in giving up on interest rate targeting, it has to pursue quantity targets for reserves and money supply instead, using reserve rationing to constrain bank lending because banks are no longer guaranteed that the central bank will provide any and all liquidity they need to defend a cash rate target. In the case of China, from the 1994 devaluation to the 2008 financial crisis, the CNY/USD was consistently below its longer-term equilibrium. Accordingly, China received significant capital inflows from investors positioning for CNY/USD appreciation. Confronted with these inflows, the People’s Bank of China (PBoC) had to choose – either let the CNY/USD – the relative price of money – appreciate, or let the quantity of money expand instead, printing the extra CNY deposits demanded by investors to dilute the currency. More often than not, the PBoC chose the latter option, meaning that capital inflow translated directly to money supply expansion, which in turn helped to fuel extremely strong domestic borrowing and growth – a virtual crowding in effect. But since the financial crisis, the CNY/USD has been perceived by investors as marginally overvalued, leading to persistent capital outflows and money supply contraction – a virtual crowding out effect. History has told us that for the emerging market (EM) complex pegged to the USD, capital inflows (outflows) have resulted in money supply-to-GDP expansion (contraction). In the case of Hong Kong, capital inflows (outflows) into the gateway city have eventually flowed into (out of) the rest of emerging Asia and been accommodated (fought) by central banks, contributing to growth (contraction) in world excess liquidity.

Revisiting the 2008 crisis against the context of savings and capital glut theories. What we have found particularly interesting about the Asian “savings glut” theory was its inability to explain the dynamics of the 2008 GFC. If Asians caused excessive borrowing in the US leading up to the crisis, it certainly was not apparent in the way the crisis unfolded. Indeed, European banks were very much at the centre of the turmoil. Pre-GFC, Europe was running a roughly balanced external account. But far from being a sign of stability, the balance was actually masking incredible imbalance, because European banks were borrowing USDs in short-term money markets and using the proceeds to purchase long-term mortgages and their derivatives. They were merely recycling USDs rather than genuinely creating credit and deposits. But because they were engaging in such wholesale maturity transformation – borrowing extremely short and lending extremely long – they were generating a liquidity effect almost indistinguishable from credit creation. On the flipside, when US mortgages started to default and investors started to question the value of “toxic securities”, European banks found themselves with significant USD asset-liability duration mismatches, and were confronted with frozen money markets, forcing the Fed to intevene. But at no point in the crisis was there any real hint of Asian banks or central banks driving or contributing to the unwind.

History might not repeat immediately, but it could rhyme … eventully. We take a trip down memory lane and revisit the plumbing textbooks, because it all matters in understanding what could happen next in the US-China-Hong Kong saga. The correlations say that Hong Kong capital outflows could eventually weigh on world excess liquidity – but they are unlikely to weigh immediately. Some might even argue that the events in Hong Kong might be specific to Hong Kong rather than the broader EM complex, and that flows out of the city might simply show up in another gateway city instead. We are not necessarily this optimistic given Hong Kong’s links to China, and China’s significance to the global economy – but nevertheless we do recognize that the argument is out there. We think that in order for the Asian USD “savings glut”, or more precisely, its unwind, to present a clear and present danger for the world, it has to do so via emerging market “crowding out” in the first instance, and then, via reductions in purchases of USD assets, whether property, bonds or stocks. But we really question whether the unwind will work out by causing US Treasury yields to imminently spike higher and US mortgage demand to fall. In part, this is because reported mortgage demand in the Fed’s Senior Loan Officers’ Survey is actually quite robust at present, unlike its very weak state pre-GFC. But more fundamentally, on the issue of higher yields, we note that the US Treasury does not need China or any other Asian central bank to finance its borrowing. Rather, the US Treasury is funded by the Fed, with or without quantitative easing (QE). To be sure, China is a large holder of US Treasuries, and any selling by such a large owner could cause price dislocations in the short-term. But if there is any doubt, we should note that China is not a forced seller of US Treasuries. If the PBoC needs USD liquidity, it can repo its USDs held in Treasuries with the Fed via the Foreign and International Monetary Authorities (FIMA) repo facility, effectively bypassing the broader market. And even if the PBoC were to fire sell its Treasuries on market, the Fed is present as a buyer of last resort via QE.

Still positioning for a world awash with excess liquidity. We are very concerned about degeneration in US-China relations longer-term. But near-term, we are focusing on the state of world excess liquidity, stoking inflation risk and higher demand for inflation hedges like commodities. We think that there is a lot going on in the world with fiscal stimulus and central bank balance sheet expansion to drive world excess liquidity higher in the core, if not the periphery. For example, even the Europeans are taking emergency measures to stimulate distressed economies using funds raised through large scale and mutual German and French bond issuance, in a European Central Bank (ECB) QE environment – effectively approaching a temporary fiscal union. And for all the negativity surrounding China’s scrapping of a 2020 growth target, it is easy to miss the announcement of more fiscal stimulus. But specifically on USD funding conditions, we are comfortable that the Fed is doing a lot to supply the world with the USD liquidity that it needs via portfolio channels, notwithstanding the threat of US-China tensions turning off the spigot via the trade channel. Indeed, the Fed could be doing enough to defer the adverse consequences of deteriorating US-China relations for a bit longer, especially if it can take advantage of a unique opportunity to devalue the USD. We are also wary of the risk that trade wars will move out of the deflationary, illiquidty phase into an inflationary, supply chain disruption and re-organization phase. Within the ASX 200, we are overweight resources. Interestingly, although Hong Kong equities initially sold off aggressively on reports of China’s plans to revise security laws, there was little follow through to US markets. And in any case, if we are wrong about the potentially negative effects of US-China tensions on world excess liquidity and commodity prices, we are likely to be equally wrong about the harmful effects on Chinese demand for property, and related exposures. In other words, there is a degree of protection from China risks at an alpha, rather than beta level.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.