US money markets pricing in negative rates for the first time. 2020 has been a year of firsts for the US economy. First negative oil prices. Then negative rate pricing. Overnight, the Fed fund futures curve priced in forecasts for negative interest rates by January 2021. The Eurodollar futures curve followed soon after. Interestingly, the prospect of large scale US Treasury bill issuance has not put upward pressure on short term yields to avoid negative rate pricing. But then again, quantitative easing from the Fed has been stepped up too, and primary dealers have had their capacity to buy US Treasuries increased by the removal of these securities from their measured leverage ratios.

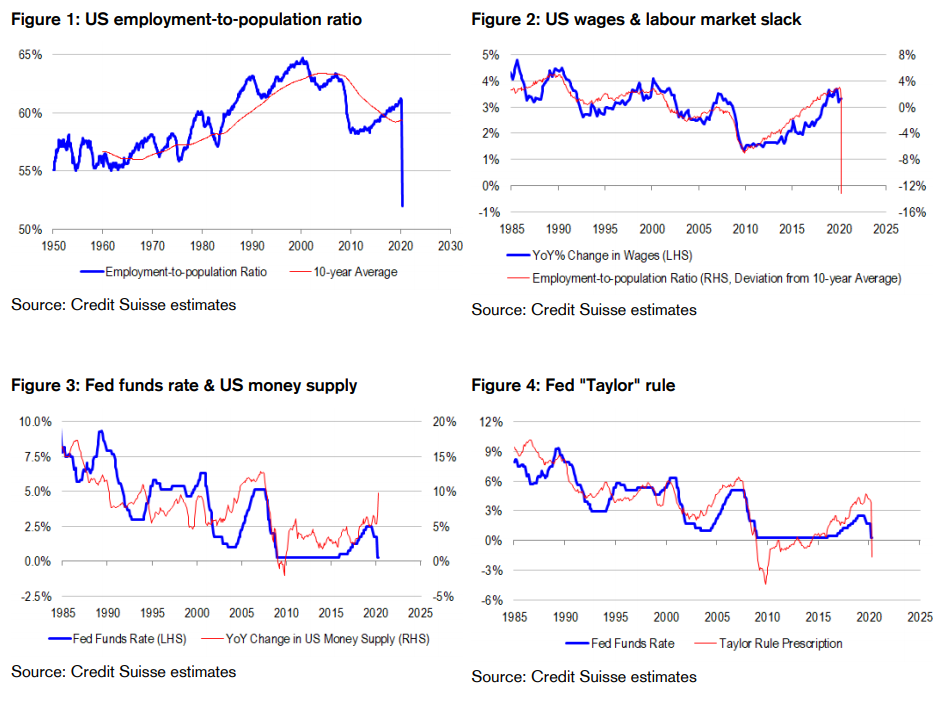

Sharp increase in labour market slack a catalyst for negative rates pricing. If the April ADP employment report is anything to go by, US labour market slack is rising sharply. Over 20,000K job losses will result in a sharp decline in the employment-to-population ratio to its lowest level in a generation of 52%, historically consistent with outright wage declines. Whether or not Americans actually take pay cuts is another matter—but if they do, it would represent yet another “first” for the economy. Regardless, “Taylor” rules will discount the risk of wage declines, prescribing negative rates as the solution to excessive labour market slack. For what it is worth, our proprietary US “Taylor” rule based on the deviation of the employment-to-population ratio from its 10-year average, and broad money supply growth is pointing to negative rates to the tune of -1.7%.

Perish the thought. We have seen “Taylor” rule prescriptions for rates turn negative before—but without the actual Fed funds rate turning negative. For example, during the 2008 global financial crisis (GFC), the Fed left its policy rate at 0-0.25% despite shrinking money supply and high and rising unemployment. But economists have argued that the Fed achieved a negative “shadow” rate by using quantitative easing (QE) to achieve the same thing as lower, negative rates. Surely, the same argument would apply this time around!? And indeed, Richmond Fed President Barkin has tried to quash any thought of negative rates immediately after the money market flagged them, arguing that the economy could be bottoming out, and that further easing may not be necessary.

Negative rates ultimately evil. By now, most people are aware of the “evils” of negative rates. They occur against the backdrop of excess reserves in the banking system. Excess reserves cannot be shed by the banks collectively—they can only be transferred between different banks, or drained from the system by the central bank or sovereign through bond issuance. When negative rates are imposed on excess reserves, effectively the banks are hit with an unavoidable tax. They either bear the tax at the cost of profit margins, or pass it on to savers. In the end, the results are perversely deflationary. And the experiences of Europe and Japan support this view.

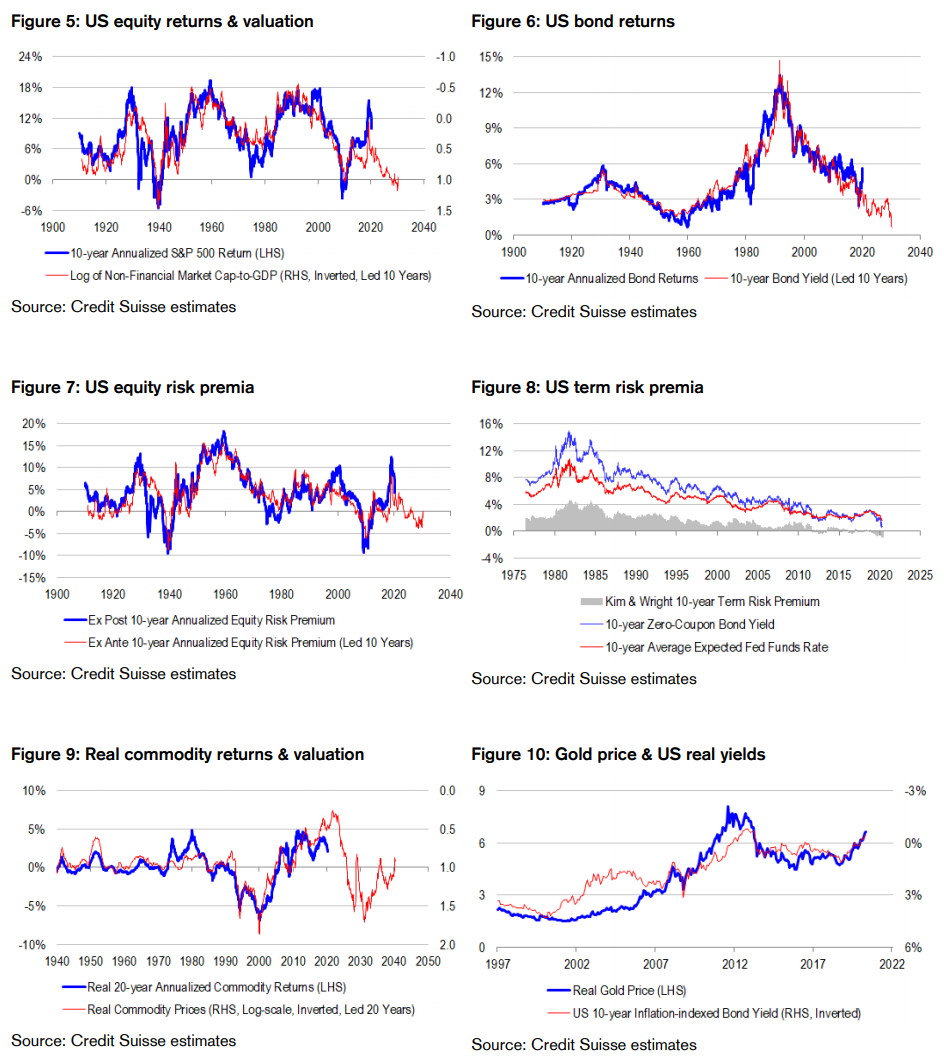

This time could be “differently the same”, because of stretched asset pricing. We all know that in theory, negative rates are “evil” and do not work. But this knowledge has not stopped central banks in Europe or Japan trying them. And the ultimate driver of negative rates in these economies is the same as the “would be” driver of negative rates in the US—stretched asset pricing. On long-term horizons, equities are priced for negative returns, and bonds are priced for lower returns than cash. Equity and term risk premia are both negative, meaning that investors are not getting compensated to take on equity and duration risk, and indeed, are paying for the privilege of doing so. This all leaves us vulnerable to a scenario where both bonds and equities sell off, without the right intervention in markets. And in this context, the tempting way out is to cut rates to negative levels in an attempt to make bonds more attractive than cash, and to stave off an equity market sell off.

“Triffin” dilemma perhaps incentivizes negative rates in short term. When analyzing the Great Depression, commentators argue that Fed officials back then mistakenly allowed money supply to shrink to preserve the integrity of the gold standard. They also argue that on the flipside, the Fed could have chosen to expand the money supply without fearing the consequences of USD devaluation, because the US was such a large player in the global economy, that interest rates abroad would have fallen, and interest rate differentials would have ultimately supported the USD. Clearly, times have changed. We are not on a gold standard anymore, and investors obviously celebrate a weaker, rather than stronger USD. But yet, there are lessons we can still borrow from history. The so-called “Triffin” dilemma refers to the idea that the Fed needs to set monetary policy for the world, and not just for the US, because the US is such a large and influential economy in the world, and the USD is used extensively in offshore jurisdictions. A negative Fed funds rate could help to bring down interest rates in other economies that are linked to the US, yet also have positive rates. China and the emerging markets (EMs) clearly fit this bill. But other developed economies have no more room to cut rates, and would suffer in the event that they were to follow the Fed into negative territory.

USD could avoid deflation and scarcity traps for a little while. Related to our point about the “Triffin” dilemma, it is possible that the Fed could weaken the USD through negative rates. In Europe and Japan, negative rates policy perversely lifted the EUR and JPY, via the channels of deflation and currency scarcity. But the case of the USD could be different, because of the world’s dependence on the USD and the “Triffin” dilemma. Indeed as it stands, real yield differentials are moving aggressively against the USD. Fiscal deficits are large, creating USD deposits, and diluting the currency. To be sure, subsequent bond issuance could easily drain USD liquidity. But as our money markets expert Zoltan Pozsar highlights, the Fed is dealing with this through its balance sheet expansion efforts. Also, the Fed is doing a lot to directly inject USD liquidity to the broader world via foreign exchange (FX) swap lines, or in the case of central banks with non-convertible currencies, the next best thing in repo land.

Seek protection from de-leveraging risk and value destruction in gold and commodities, as well as quality and momentum reversal factors. Negative interest rates are ultimately deflationary and consistent with de-leveraging, because they make financial conditions tighter, and reveal how vulnerable economies and markets are to asset price bubbles bursting. De-leveraging pressure undermines the efficacy of value investing, because asset prices drive fundamentals rather than the other way around. Shorter-term, financials favoured by value factors usually underperform because of negative rates. Yet despite the familiar side effects from the medicine of negative rates, they can prove to be a morsel too tasty for central banks to resist. Bond yields could fall for a little while. In the Fed’s case, the USD could weaken for a little while. Quality stocks within the equity market could outperform on the initial bond bid. Gold and arguably cheap commodities could well match or better bonds in the short-term—and if yields actually turn negative, they could easily outperform on better carry. Our problem with chasing bonds and related exposures within the equity market however is that ultimately, negative rates bring with them higher uncertainty about policy, which in turn could feed into higher volatility. And higher volatility is almost always bad for momentum trades, because it either signals a turning point in the cycle that wrong-foots trend followers, or brings about de-leveraging and de-risking in the passive investing community.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.