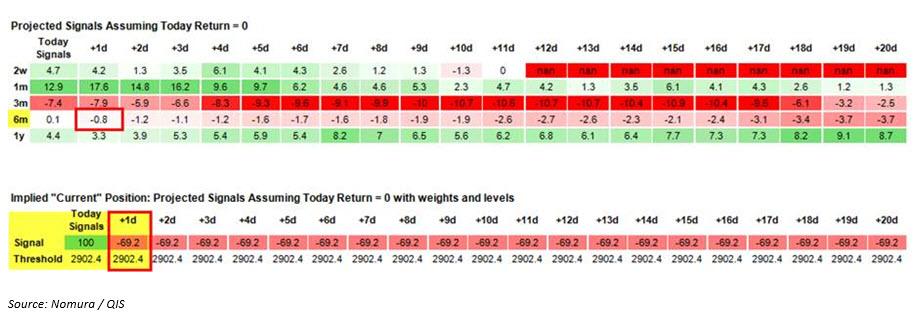

The gap-down tripped the just-established CTA “+100% Long” signal back into “-69% Short” territory (ref 2845 last in spot, well-below the 2926 trigger on-close required for the “flip short” and actually now proximate to the 2805 “-100% Short” signal trigger level)

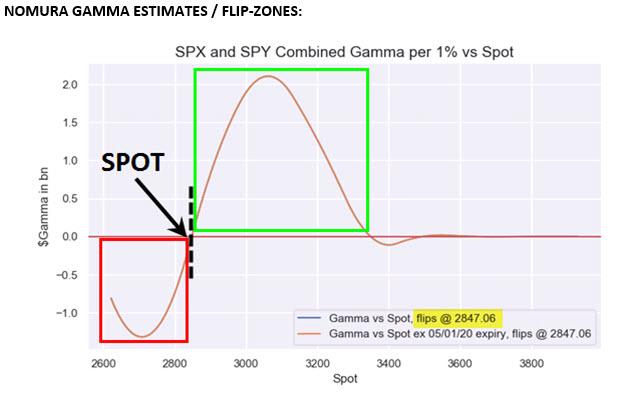

The gap also shocked the also just-established Dealer “Long Gamma” position (when ref was ~2940 yday morning) now all the way back down to the exact “Neutral Gamma” level (2847, basically right where spot is now)—while any push lower from here then risking a move deeper into outright “Short Gamma” territory which would elicit heavier-handed Dealer hedging flows that likely dictate “selling-into lows”

it has sent the S&P back below the trigger level where CTAs would again pivot back -“short” as the 84.6% loading in the 6m window would “flip” (a close below 2926 has signal to -69% short, while below 2805 goes back -100% short—albeit all on smaller gross $ exposure)’

this current spot ref ~2840 level is actually back (lower) to the “Gamma Neutral” level from yesterday’s typically insulating “Long Gamma” position for Dealers…but certainly now capable of slipping into outright “Short Gamma” on another surge lower

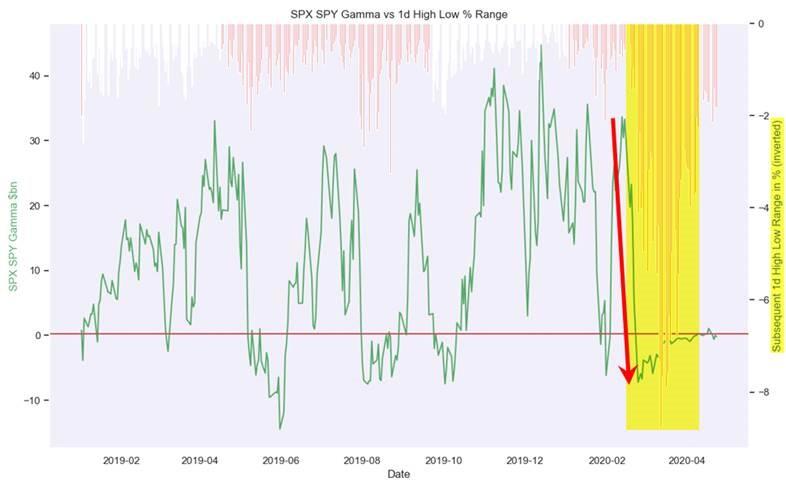

To the second point above, McElligott adds that impulse shifts lower in the Dealer “long gamma” position – think of its a third derivative of prices – tend to corroborate with larger trading ranges, especially as we get deeper into “short gamma” territory and Dealer hedging behavior is altered, having to “sell into the hole.”

…a bleed deeper into “Short Gamma” territory now that we are slightly below the “Gamma Neutral” level at 2847 (with $1.1B $Gamma at the 2850 strike)…things get especially frisky into an approach of 2805 (CTA’s going deeper short from “-69% Short”- to “-100% Short”- signal) and the “Short Gamma” more aggressive options Dealer hedging flows (selling into lows), all of which could conspire and accelerate this market reversal–particularly in light of weaker holiday volumes.

One of the lessons of recent market price action is how extreme robots have made volatility. We’ve had the fastest crash down in history. Followed by one of the fastest and largest “crash up” movements in history.

Advertisement

Over the stretch, the market should still revert to being a “weighing machine” versus a “voting machine” – in the Graham/Buffet model – but with robots doing the voting, the pace and amplitude of moves is accelerated. To wit, at Bloomie:

Warren Buffett has been waiting years for stocks to look more attractive. He apparently didn’t think the first-quarter plunge was that opportunity.

As the coronavirus slowdown started to grip the U.S., the famed investor’s Berkshire Hathaway Inc. was building its massive cash pile to a record $137 billion by the end of March. The company said that figure climbed even higher as it dumped more than $6 billion of stocks in April, making Buffett a net seller of equities so far this year.

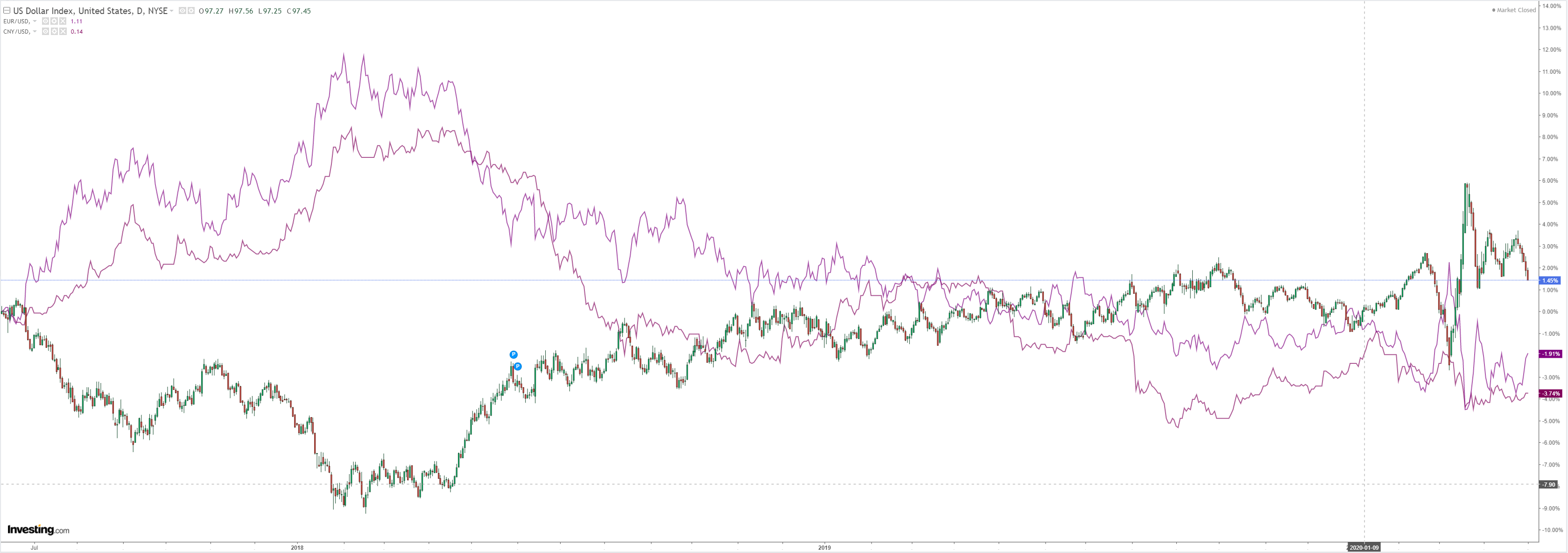

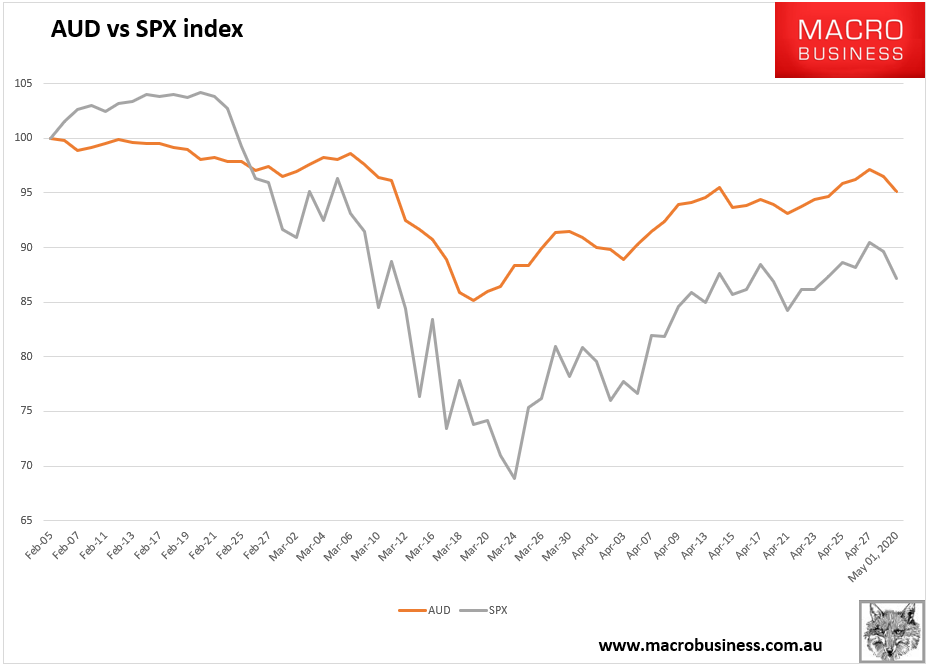

For forex, this volatility is normal but the correlation with robot-driven stocks right now is very high:

Advertisement

So, in the medium term we expect fundamentals to prevail for both stocks and the AUD.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.