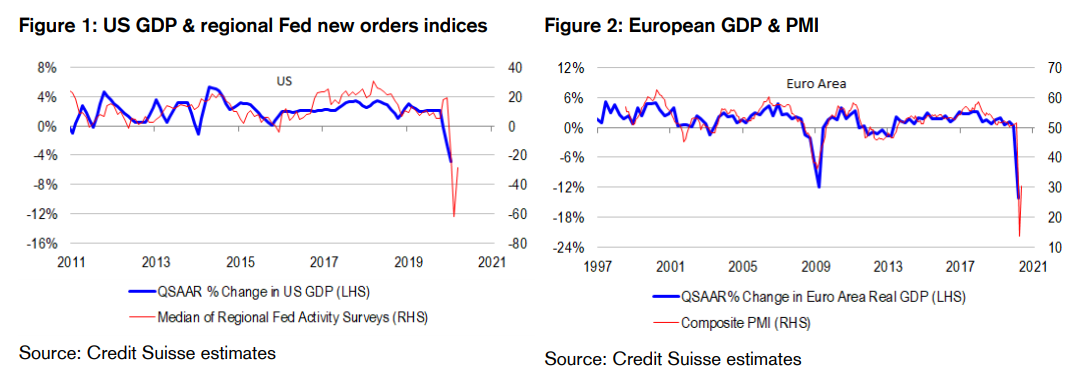

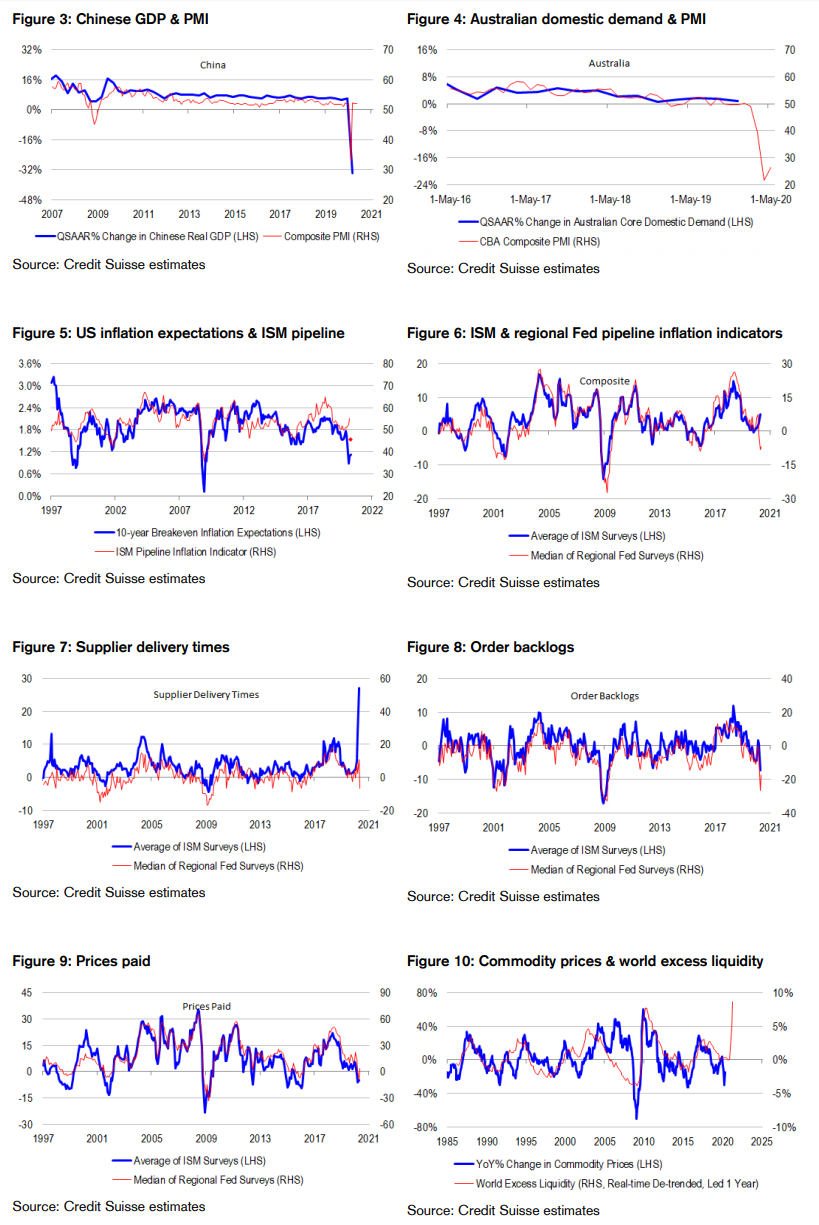

Activity bottoming out. May purchasing managers indices (PMIs) for Australia and major economies reveal a bottoming out process in train. PMIs everywhere are rising sharply off their historical lows. To be sure, PMIs are diffusion indices, meaning that their level corresponds with a rate of change in activity, and sufficiently high readings are necessary to get outright expansion. And right now, they are all pointing to less contraction, rather than to outright expansion with the exception of China. But broadly based and positive deltas are hard to ignore considering how much bad news investors have had to bear, and how hard policy makers around the world are trying to re-open economies.

US surveys reveal less supply chain disruption, but slightly more cost pressures. Regional Fed manufacturing surveys reveal that supplier delivery times could actually be in the process of shortening, consistent with less supply chain disruption from business and border closures in the wake of the COVID-19 outbreak. But they also point to a bottoming out in input prices, probably reflecting the recovery in oil prices from negative levels.

Inflation pipeline indicator may dip, but still expect higher break-even pricing. Our proprietary inflation pipeline indicator is a powerful anchor for inflation pricing in bonds. It takes into account all the inflationary components of business surveys – supplier deliver times, order backlogs and prices paid – to understand what pipeline inflation pressures are doing in real time. The most reliable inputs come from the ISM surveys – but in between these survey releases, we can use regional Fed manufacturing surveys as a rough guide. And if regional Fed surveys are anything to go by, we should expect to see the pipeline indicator dip. All other things being equal, this would be consistent with lower bond market inflation expectations. However, all other things are not equal, because actual “break-evens” have been persistently undershooting since the crisis broke out, and have room to rise in order to catch up to our pipeline indicator.

Supply chain disruption is fluid, and liquidity abundant. We suspect that regional Fed surveys are understating the degree of supply chain disruption, as their measures of supplier delivery times never really reached the heights of the ISM surveys. And going forward, we could see trade war escalation take over from COVID-19 as the driver of disruption. To be sure, the “deflationistas” will worry about USD funding shortages for emerging markets (EMs) in such a scenario. Indeed, we worry about these shortages too. However, we also note that the Fed is providing any and all USD liquidity the world needs through portfolio channels, even if the US as a whole is not providing it via trade channels. The Fed is injecting USD liquidity to most of the world via foreign exchange (FX) swap lines with counterpart central banks. And for economies with non-convertible currencies like China, the Fed is offering the next best thing via its Foreign and International Monetary Authority (FIMA) repo facility, which allows foreign central banks to swap the USDs they hold in Treasuries for instant USD cash with the Fed rather than with markets.

Too early to fade the reflation trade. Supply chain disruption may be fading – but demand is picking up. We have not yet seen the destructive effects of corporate insolvencies and permanent business closures on productive capacity. And central banks, with fiscal policy makers are doing their level best to create “helicopter money” through unconventional balance sheet usage and large deficits. In this environment, we think that it is too early to fade reflation trades. We remain overweight commodities at asset and sector allocation levels. We are also short on (defensive) momentum at a factor level.

Unless we get MMT, the only inflation we’ll see is in asset prices, as usual.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.