This scenario assumes that most of the current domestic containment measures remain in place for most of the June quarter. Most of the restrictions are assumed to have been lifted by the end of the September quarter, aside from the limits on very large public events and gatherings, which are assumed to remain in place for longer. International border closures are assumed to be in place until the end of the year, consistent with recent statements from the Australian Government.

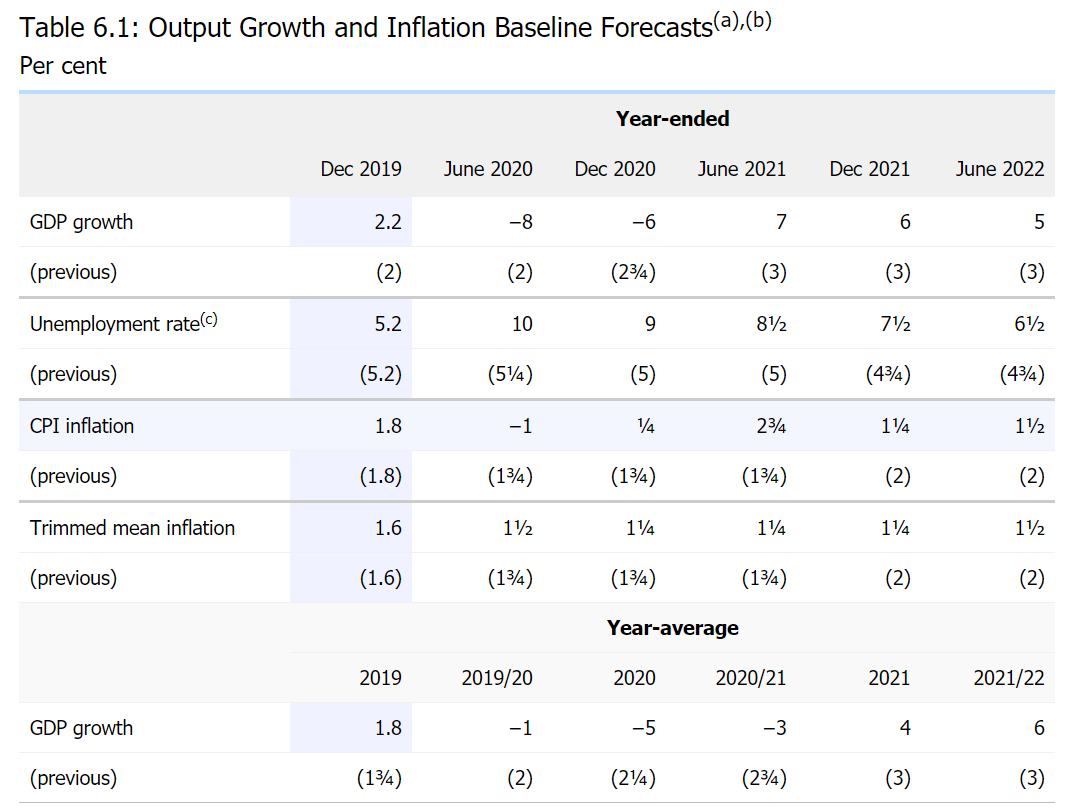

In this scenario, GDP growth is expected to start recovering in the second half of 2020, led by consumption, although the very large contraction in the March and June quarters would still result in a year-ended decline over 2020 (Table 6.1; Graph 6.3). Growth would then be stronger over 2021 as business and dwelling investment gradually recovered, although the level of GDP by mid 2022 would still be below the level expected at the time of the February Statement. Under these conditions, the unemployment rate is expected to decline substantially from its June 2020 peak of around 10 per cent but to remain above its pre-COVID-19 level in two years’ time (Graph 6.4). In underlying terms, inflation is expected to remain below 2 per cent over the next couple of years.

Scenario 2: faster recovery

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.