The Reserve Bank of New Zealand (RBNZ) yesterday released its bi-annual Financial Stability Report (FSR), which stated that the nation faces its sharpest economic contraction in 160 years:

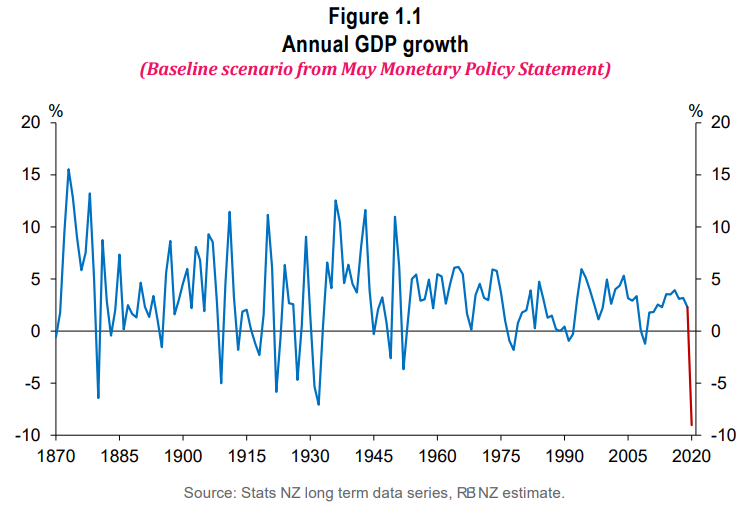

In New Zealand, border closures and economic lockdowns have led to an unprecedented decline in economic activity. Even accounting for an expected recovery in the second half of the year, this year’s projected decline in annual GDP is the largest in at least 160 years (figure 1.1). The associated losses in income will cause financial distress for a significant number of households and businesses…

The RBNZ also warned that the banking system’s “resilience will be tested in the coming months” as businesses fail, household incomes fall, and house prices fall:

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.