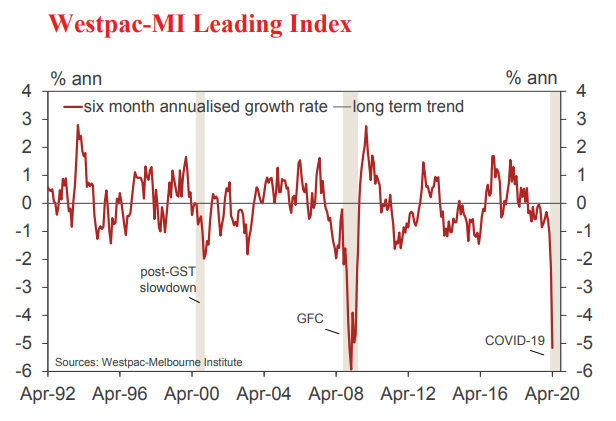

• The six month annualised growth rate in the Westpac– Melbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, fell from –2.34% in March to –5.16% in April.

The signal points to a broad-based economic contraction.

This is easily the weakest reading since the GFC and is comparable to readings seen prior to Australia’s recessions in the 1990–91, 1982–83, 1974–75 and 1960–61.

The speed of the collapse in the Index is unprecedented.

Previous lows in the Index growth rate were: March 1961 (–4.61%); August 1974 (–7.50%); February 1982 (–4.44%); January 1991 (–2.63%); and February 2009 (–5.93%).

In those previous cycles the deterioration gathered momentum over six to twelve months whereas in this cycle the growth has collapsed from –1.06% to –5.16% in just two months.

Our standard procedure is to assess the movement in the growth rate over the last six months, over that period it has fallen from –0.53% in November to the current –5.16%.

Two components account for the bulk of the 4.63ppt slump: US industrial production (–3.23ppts) and aggregate monthly hours worked (–1.72ppts). Both recorded startling declines over the last two months as the full impact of the COVID-19 health emergency and associated shutdowns

showed through. US industrial production plunged 15.3% between February and April, the biggest decline since World War 2. Meanwhile, lockdowns in Australia triggered a 9.2% drop in hours worked in April, more than two and a half times larger than the biggest monthly variation seen in

the forty years the data has been collected.

Other components have been more mixed, showing a slight improvement on a combined basis. Equity markets have regained some of their initial losses but are still down sharply for the year, the 19% drop in the S&P/ASX 200 component taking a further 0.79ppts of the Index growth rate since November. Other components have seen net improvements though: commodity prices (in AUD terms) adding 0.43ppts to the growth rate over the same period with some additional support coming from a widening yield spread (+0.23ppts); a modest lift in dwelling approvals (+0.19ppts); and less negative reads on Consumer Unemployment Expectations (+0.19ppts); and Consumer Expectations more generally (+0.08ppts).

In particular, the resurgence in Confidence we reported last week around the Westpac Melbourne Institute of Consumer Sentiment boosted the contributions from two components in the Index by 0.62ppts in April from March compared to a reduction of 0.36ppts in March.

The Leading Index growth rate is likely to recover as Coronavirus restrictions are removed. However ongoing public health concerns are likely to see restrictions continue to disrupt economic activity for many months to come.

We do not expect the economy to return to preCoronavirus levels of activity before 2022.

The Reserve Bank Board next meets on June 2. As we saw in the minutes for the May meeting the Board is committed to maintaining its significant support for the economy for the foreseeable future.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.