Industry superannuation funds claim the Morrison Government’s early release policy has raised “sovereign risk” and will hamper returns in the future:

“Clearly the government has changed the rules and super funds now need to factor in sovereign risk [the danger of governments acting precipitously],” [HostPlus CEO David Elia] said.

“That means funds will carry higher levels of cash, resulting in lower returns.

“We will be less aggressive in terms of the allocation of funds to [the venture capital] sector and that applies to all asset classes”…

“Simply by virtue of [the government intervention] … we will see lower returns across the sector. I think that’s the significant conclusion you can draw,” he said.

However, David Knox from Mercer has played down the impact of the early release policy, claiming that “total funds withdrawals have been just over 1 per cent of funds under management”:

“Some funds will have seen withdrawals of more than that, with HostPlus experiencing around 2.5 per cent,” Mr Knox said.

“But even 2.5 per cent is not a big issue as far as liquidity goes”…

“I’m not sure all funds will have to hold more in cash, but some might,” Mr Knox said.

In any event, requiring superannuation funds to hold more liquidity would be a good result. Industry superannuation funds have leveraged too heavily into illiquid unlisted assets like ports, toll roads and airports, as well as private equity funds.

While this has allowed them to trade on a so-called “illiquidity premium”, thereby delivering better returns over both the short and long-term, it has also raised risks, as we have witnessed recently.

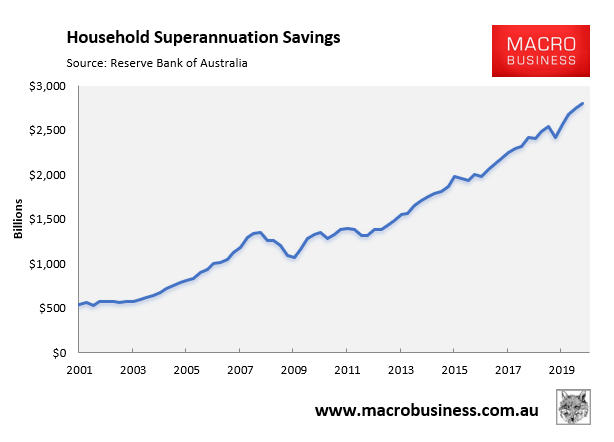

It is also rather galling to see industry funds complain of “sovereign risk” when government policy mandates that workers must direct 9.5% of their wages into superannuation, thus ensuring ever-growing funds under management:

Few other industries in Australia receive such generous government support.