The Australian Prudential Regulatory Authority (APRA) has released its weekly update on the Morrison Government’s early release policy, which reveals that another 1,650 million funds were withdrawn in the week ending 17 May, with total withdrawals topping $10.6 billion:

As shown above, just over 1.4 million applications have been paid averaging $7,322.

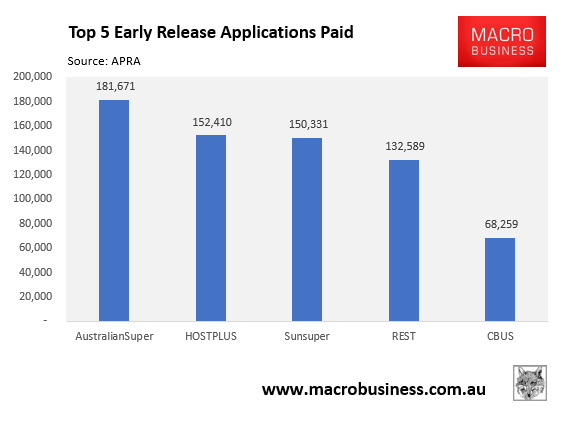

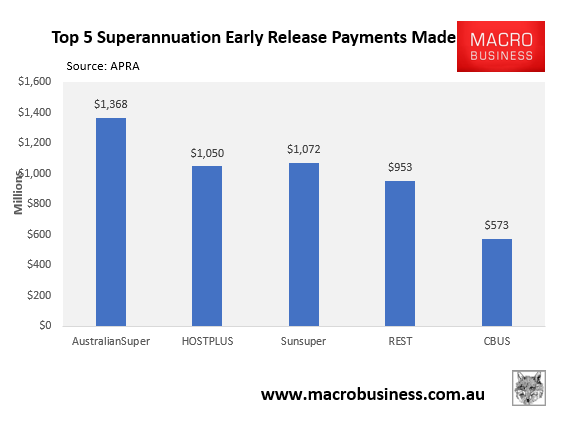

Looking at the fund breakdown, we can see that industry funds suffered the five biggest draw downs, with the below five funds alone accounting for half of total early superannuation withdrawals:

Separate data from the Australian Treasury shows that younger Australians have dominated superannuation withdrawals in number terms:

A third of people tapping their superannuation accounts to get through the coronavirus pandemic are under the age of 30.

…of the almost 1.4 million people to have accessed up to $10,000 of their superannuation, more than 463,000 of them were under the age of 30…

While accounting for more than half of all people accessing their super early, people under the age of 35 took out 46 per cent of the cash that has so far been distributed.

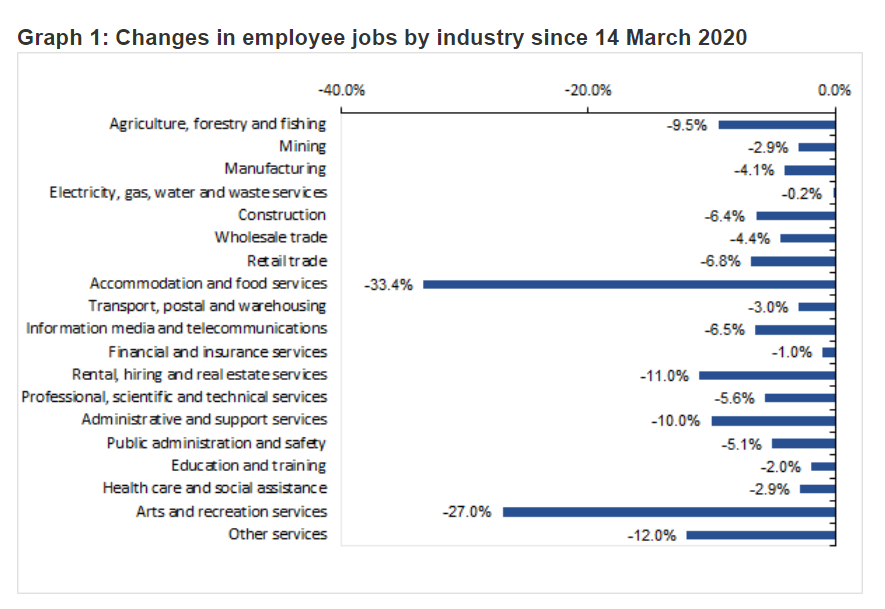

The disproportionate impact on industry funds and younger Australians makes sense given they are most exposed to areas hardest hit by COVID-19 job losses, such as Accommodation & food services, as well as Arts & Recreation:

We are likely to further heavy withdrawals given superannuants are permitted to withdraw an additional $10,000 from their funds from 1 July.