Via Goldman which sees the S&P500 minus 18% to 2400 by August:

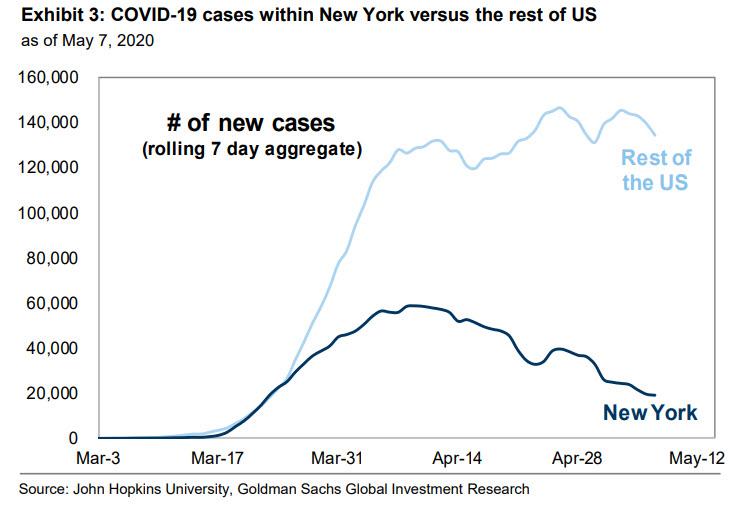

- First, COVID-19 infection rates outside of New York continue to grow. While New York has thankfully been able to flatten the curve and the rate of growth of new cases had decelerated, new infections in the rest of the US are increasing. Cases of infection may accelerate as states begin to relax shelter-in-place rules.

- Second, the re-start process will take time. As IDEX Corp. noted on its call: “And just to be clear, our expectation here is that this is going to be fits and starts. I am not someone who has bought into a super aggressive, everything gets fine in the fall sort of thing. I think that’s crazy talk. And I think we have to face the reality that’s in front of us. And you know what, if we get lucky, and for some reason, this goes away with weather or something else or a vaccine is found more quickly than we think or you have very, very effective treatments, great news. I don’t think anybody should bank on that, and I certainly wouldn’t manage the company expecting that.”

- Third, bank loan loss reserves in 1Q totaled $46 billion vs. $49 billion for full-year 2019. All of the banks “marked to market” their provision estimates assuming a 9.5-10% unemployment rate. The jobless rate spiked to 14.7%, with Goldman analysts forecasting $115 billion in provisions in the next four quarters. Banks and other firms have cancelled repurchase plans, and recently Goldman forecast that buybacks will fall by 50% in 2020. And while this step delights credit investors, Kostin warns that “equity investors should be concerned because buybacks have been the only source of net demand for shares in the past decade.”

- Fourth, dividends are also at risk. In an effort to preserve liquidity, more than 40 stocks have suspended or reduced their dividends YTD. Goldman expects dividends to fall by 23% this year. Growth plans are frozen and capex spending will drop by 27%.

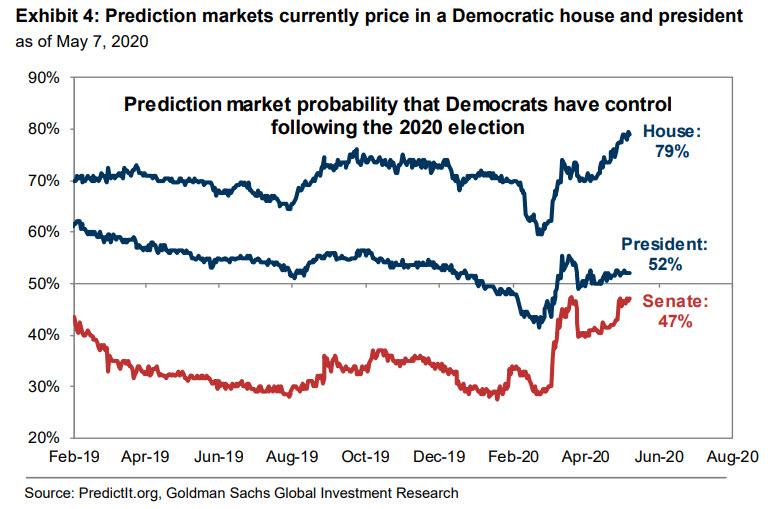

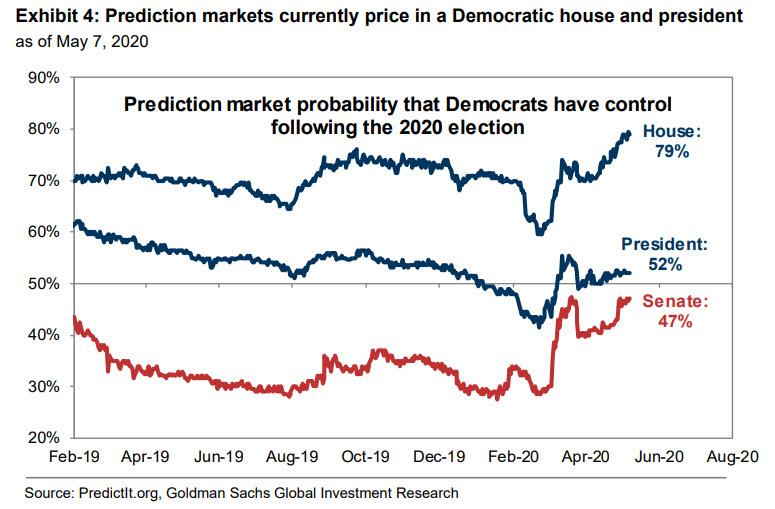

- Fifth, domestic politics. The presidential election is six months away. If the economy is on a path to normalization by early 3Q, investor focus will shift to the election. The 2017 tax reform act lowered the effective corporate tax rate to 18% from 26%. However, the tax law could be reversed depending on the election result, i.e., if Biden wins. If so, 2021 EPS would fall by $19 and imply a P/E multiple 15% higher than the already stretched valuation (assuming anyone still cares about fundamentals).

- Sixth, global politics. Investors may need to contend with another twist in US-China trade/strategic development, which was at the forefront of investor concerns for much of 2019. The nature of the tension seems multi-faceted going beyond conflicts in merchandising and service trades, with the US administration’s rhetoric and actions towards China turning more hawkish in the past month across various issues and strategic domains.

Seven, now that Goldman is bearish it is almost certainly front-running its call.