Nothing we don’t know given the move in the ANZ measure:

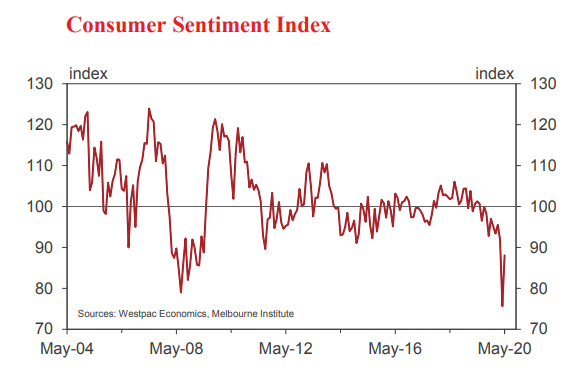

• The Westpac-Melbourne Institute Index of Consumer Sentiment rebounded 16.4% to 88.1 in May from the extremely weak 75.6 read in April.

The survey spanned the period 4-8 May, which covered the lead up to and actual announcement of the Commonwealth Government’s Three Stage Plan to ease restrictions.

This represents an impressive recovery in Confidence.

Consumers are clearly heartened by Australia’s success in containing the Coronavirus which has justified the easing of some of the social restrictions that have been so painful for individuals and the economy over the last two months.

The May turnaround marks the biggest monthly gain in the Index since the survey began nearly fifty years ago. That has gone a long way towards reversing the record monthly fall (17.7%) we saw last month.

The Index is still relatively weak by historical standards – May being the second lowest read since the Global Financial Crisis and firmly in pessimistic territory. The despair apparent a month ago, when Australians were bracing for a severe outbreak and a prolonged shutdown has lifted materially, but consumers are still justifiably cautious.

Nevertheless the Index is now only 7.6% below the average level over the six months covering September to February despite the clear challenges still confronting the economy.

It is also important to note that the component of the Index that captures the longer term view is around 50% higher than we saw in the recession years of 1989 –1991.

Consumers can understand and envisage the recovery whereas in recessions the feeling of hopelessness takes over.

Developments around the Coronavirus have been positive.

While the number of confirmed cases globally has doubled since the April survey, the rate of growth has slowed markedly in both Europe and the US. Australia has seen particularly good outcomes with the total number of confirmed cases rising just 10% over the month, and showing signs of levelling out altogether. The resulting

pressure on our health system is much milder than had been feared two months ago.

The survey detail confirms that these developments sit at the centre of the turnaround. Sentiment in WA (up 29%) surged as the state performed well on containment and respondents prepared for a significant easing in restrictions. In NSW there was also an outsized boost (up

23%) probably reflecting an earlier than expected easing of restrictions. On the other hand confidence in Victoria (up 8%) only lifted moderately as news of recent outbreaks and uncertainty around restrictions weighed on confidence.

Sentiment also posted extraordinary gains amongst those employed in key sectors hit hardest by the social distancing restrictions – up over 30% for those working in the hospitality, health and consumer services industries.

Arguably, the age group detail suggests the return to ‘face to face’ operations for schools in most states has also been a positive – sentiment posting notably stronger gains amongst those in the 35–54 year age range (up 23%).

The component detail showed gains across the board but was led by the sub-indexes that are most sensitive to the direct effects of the shutdown and showed the heaviest falls in April.

The ‘economy, next 12 months’ sub-index recorded a spectacular 32.6% rebound to 71.2 in May, coming from an extremely weak 53.7 read in April (comparable to the lows seen during the GFC). The prospect of an earlier than expected reopening for the economy has soothed some of the worst fears around the economy although readings imply consumers still do not expect a return to growth any time soon.

The other big mover was the ‘time to buy a major item’ sub-index which surged 26.7% to 96.6 in May from 76.2 in April. Reduced concerns around health risks; the prospect of easing social restrictions and more certainty around incomes look to have had a direct impact here. The response suggests retailers can expect more foot traffic as restrictions ease although the overall level of the index still suggests most consumers will be looking to keep spending on a tight rein.

Other components also rose in the month but showed more muted gains.

The ‘economy next 5yrs’ sub-index rose 10.7% gain but was much more resilient last month. It is very interesting that this Index has touched a nine month high. Respondents are clearly confident that the economy will cope with this short term crisis and emerge in good shape to deal with future challenges. This is a stark indicator that the current economic crisis cannot be compared with a recession, when respondents despair for the future. The current reading for this component is 50% higher than the average seen during the deep recession in 1989-1991.

Around family finances, the ‘finances vs a year ago’ subindex rose 5.5% to 74.3, partially retracing last month’s fall.

The lift may be a sign that support from a range of measures – including the JobKeeper and JobSeeker policies as well as temporary relief for mortgage and rental payments – may be providing more help at the margin. A recent statement from the Treasurer points out that 835,000 businesses employing 5.5 million workers have benefitted from the JobKeeper

Payments while 1.4 million have received the increased payments linked to JobSeeker.

Responses to an additional question on rents indicate that one in five tenants have negotiated a temporary reduction in rental payments (most being reductions 25% or less).

The forward view on family finances showed a more promising improvement, the ‘finances next 12mths’ subindex rising 12.2% to 102 – a twelve month high and a reading that implies more consumers expect their finances to improve than deteriorate over the next year.

The Westpac-Melbourne Institute Unemployment Expectations Index also improved dramatically in May, a 13.4% decline unwinding almost all of the 17.4% jump over March-April (recall that higher readings indicate that more consumers expect unemployment to rise in the year ahead). Respondents are much more confident about job

security and/or prospects than might be the case given the gloomy outlook for the jobs market that still dominates the media. There is clearly an expectation that a return to more normal conditions will allow many workers displaced by the Coronavirus shutdown to return to their jobs. Indeed it is notable that Consumer Sentiment amongst those unemployed and actively looking for work is actually higher than that for the wider population (93 vs 88.1).

Sentiment around housing also rebounded in May, although price expectations remained an exceptional weak spot.

The ‘time to buy a dwelling’ index jumped 31.8%, reversing most of April’s 26.6% drop. At 108.2, the index is back in positive territory indicating optimists again outnumber pessimists. The rebound was across all states, although WA (up 68%) deserves special mention as Perth looks to resume the recent recovery we have seen in its housing market, which has under-performed for many years.

Consumer expectations for house prices posted a much milder 4.6% gain – only a slight reversal from last month’s very large 50% drop. It is extremely noteworthy that in the midst of this exuberant rebound in confidence prospects for house prices have hardly budged. Notably, expectations in Victoria bucked the modest national trend posting a further deterioration (–11.8%). The Melbourne housing market looks vulnerable to the sudden slowdown in foreign student and migrant inflows and has already seen some early price slippage. The situation clearly bears watching closely.

The Reserve Bank Board next meets on June 2. In the Bank’s Statement on Monetary Policy it forecast a grim outlook for the Australian economy. However it also included a ‘faster recovery’ scenario where it envisaged the unemployment rate returning to 5% by mid-2022. Today’s survey results provide genuine reason for optimism that the Australian economy can surprise forecasters on the upside in these highly uncertain times.

With the overnight cash rate at the effective lower bound and the Bank standing in the market to buy three year bonds at the cash rate further confirmation of a faster than expected turnaround in the Australian economy will spark some life into the markets.

Jeez Bill, way to oversell it. We’ve been let out of jail and the sun looks good is all.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.