Gareth Aird, Head of Australian Economics at CBA, has written insightful research on the impacts of lower immigration on the Australian economy resulting from the COVID-19 pandemic.

A key finding is that lower immigration will actually be good for Australian wages, since it will reduce labour overcapacity and improve the bargaining power of workers. Lower immigration will also enable Australia to partially catch-up on its infrastructure deficit, thus raising living standards.

Below is the full report.

Key Points:

Net overseas migration and in turn population growth is forecast to decline significantly due to the COVID-19 pandemic.

Lower net overseas migration will have a material negative impact on aggregate growth rates in the economy, but per capita outcomes will be less affected.

The drop in net overseas migration due to COVID-19 is an opportunity for policymakers to review thelong term strategy related to population growth and immigration in Australia.

Overview

One of the profound short to medium term impacts of the COVID-19 pandemic on the Australian economy will be lower net overseas migration (NOM). Indeed there will be a lot less migration and emigration taking place globally. But Australia will feel the impact more than most other jurisdictions because we have been more dependent on NOM as a growth driver over recent years. The more reliant you are on something the more you feel its absence. Residential construction and some parts of the education sector in particular will be hit hard. But it’s not all one way. There will be some benefits to the resident population, like stronger growth in public investment per capita.

The bottom line is that lower NOM has both an impact on the supply and demand sides of the economy. A large drop in population growth will have significant negative impacts on aggregate measures of the economy like GDP growth and employment. But it will have a much more muted impact on per capita measures of the economy like GDP per capita and the unemployment rate. It is per capita outcomes which ultimately matter for living standards.

In this note we take a look at what the drop in NOM because of COVID-19 means for the economy in the near term. And we also bring into the discussion what a lower level of NOM more generally would mean for the economy over the longer run.

The context

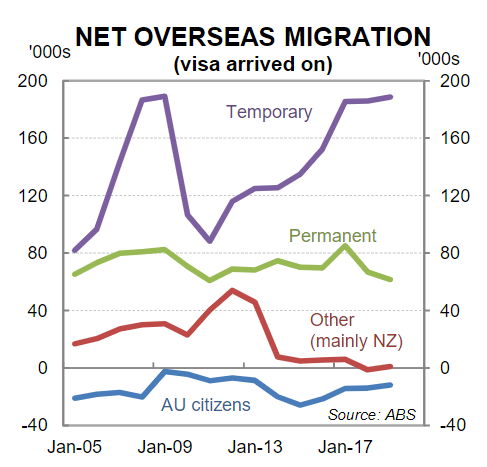

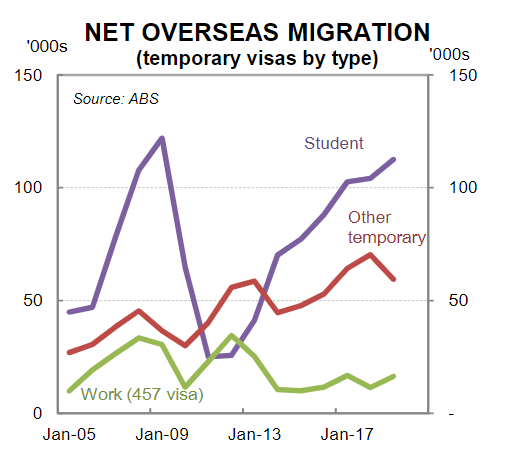

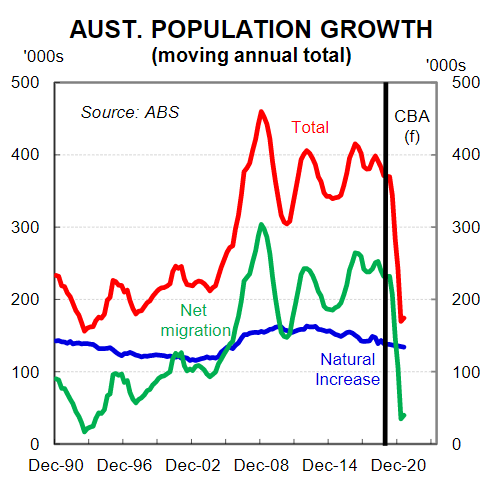

Australia’s population grew by a strong 1.5% (i.e. 373k) over the year to Q3 19 (latest available). NOM accounted for 62.5% of that increase. NOM differs from the permanent migrant intake although it is a big driver of immigration. NOM arrivals are international travellers, overseas students and temporary workers who stay in Australia for 12 months or more over a 16-month period (charts 1 & 2). Many travellers, students and temporary workers go on to be permanent migrants so there is a strong relationship between NOM and immigration.

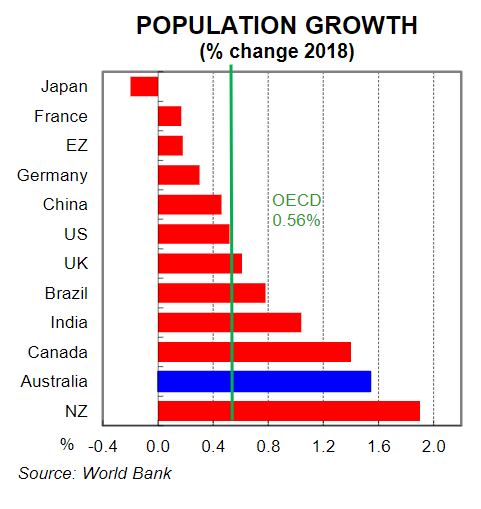

Australia’s strong rate of NOM means that our population growth rate has been significantly higher than most other OECD countries (chart 1). As we have remarked in the past, a high population growth rate means that making comparisons of economic performance between Australia and other OECD countries using aggregate growth rates like GDP can be misleading. As Governor Philip Lowe commented in 2017, “our strong population growth has flattered our headline growth figures.”

Having a strong population growth rate for a sustained period of time has had implications for the industry composition of the economy. More specifically, Australia has a larger construction sector relative to other developed economies that have slower rates of population growth. Strong growth in the number of people means that more needs to be built –dwellings, roads, schools, hospitals, ports etc. This means that a greater proportion of the workforce in Australia is employed in the construction sector than would otherwise be the case.

The Government recently announced that it expects NOM to fall by ~30% in 2019/20 and by ~85% in 2021/22. The 2019 Budget assumed NOM of ~270k so applying the Government’s expected reduction in NOM to its previous forecasts leaves NOM of ~190k in 2019/20 and ~40k in 2020/21. This means that there is an expected shortfall of around ~310k in NOM over the next 18 months compared to original estimates. Population growth will slow sharply from 1.5% to 0.7%/yr over that period (chart 4).

What does lower NOM mean for the economy

A material drop in NOM has both short and longer term economic impacts. These primarily relate to GDP, the labour market and the housing market. We cover each below.

GDP

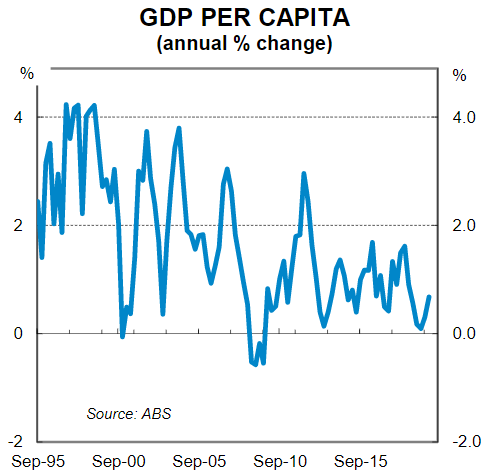

Lower NOM means less people spending and less economic activity than would otherwise be the case. This lowers potential GDP growth, which is a function of population growth, participation and productivity. Put simply, GDP will be lower than otherwise with a reduction in NOM. On our estimates we are looking at a reduction in GDP of 0.75%-1.0% over 2020/2021 due to the sudden drop in NOM (note that we are forecasting overall GDP to fall by 2.8% in 2020/21). Things don’t look as bad, however, on a per capita basis.

The drop in NOM over 2020/21 is only expected to shave 0.2% off GDP per capita. The reason that GDP per capita falls in the short run is primarily due to the big demand shock to residential construction (see below). But in the medium to longer term a permanent reduction in NOM each year should have no impact on GDP per capita once the economy has rebalanced. For example, NOM could be halved without any impact on GDP per capita over the medium to longer term.

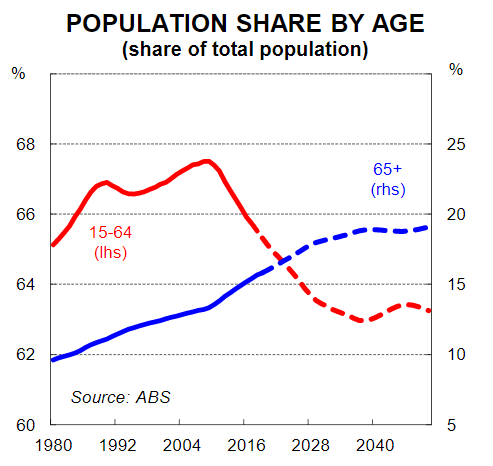

It is often argued that that a higher rate of NOM helps to offset the impacts of the growth in the dependency ratio (the age-to-population ratio of those typically not in the labour force). And this should lead to higher GDP per capita. That is true in the short run. But it makes no difference in the long run. As the Productivity Commission argued in April 2016, “the continuation of an immigration system oriented towards younger working-age people can boost the proportion of the population in the workforce and, thereby, provide a ‘demographic dividend’ to the Australian economy. However, this demographic dividend comes with a larger population and over time permanent immigrants will themselves age and add to the proportion of the population agedover 65 years.”

In other words everybody gets old and so a higher rate of NOM cannot boost GDP per capita in the medium to longer term (chart 6).

Housing

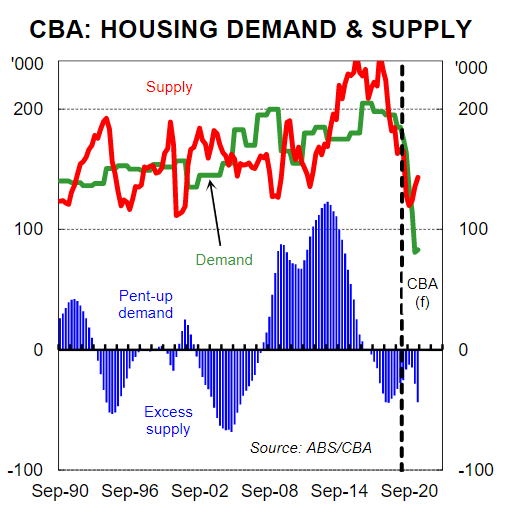

Lower NOM will have an impact on the demand for housing. Lower growth in the population means less demand for new housing and less residential construction than would otherwise be the case. In Australia’s case the impact of lower NOM on new dwelling construction will be very significant. Australia’s population has grown by ~380k per annum over the past two years. That means underlying demand for new housing has been running at ~185k dwellings per year (i.e. on the assumption of 2.1 persons per dwelling).

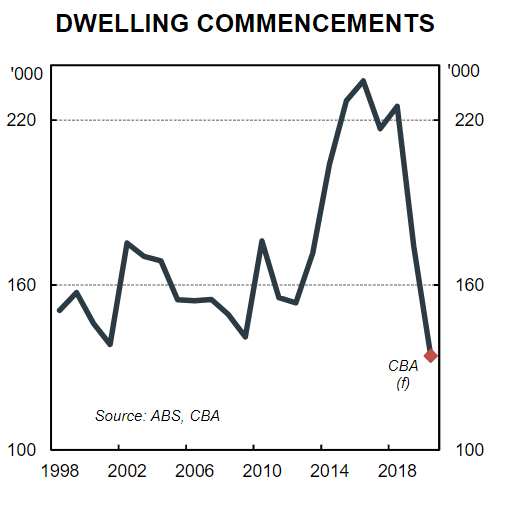

But with population growth set to drop to 185k in 2020/21 the underlying demand for new housing plummets to 90k. As such, we recently materially downwardly revised our forecasts for dwelling commencements in 2020 and 2021 (see here and charts 7 and 8). This means that we expect a big drop in residential construction (down ~9% in 2020/21)and we do not expect dwelling investment to return to pre-COVID-19 levels until Q1 22 when NOM is assumed to lift towards the budget assumption. Over this period the fall in dwelling construction will have a big impact on the number of people employed in the residential construction sector.

We also downwardly revised our outlook for dwelling prices and expect a 10% fall in prices over the next 6 months. While lower NOM is not the primary reason we did that, it did feed into our view on house prices because everybody needs a roof over their head. Strong NOM keeps a lid on vacancy rates as well as puts upward pressure on rents and prices. As the Productivity Commission also noted in their April 2016 report, “high rates of immigration put upward pressure on land and housing prices in Australia’s largest cities. Upward pressures are exacerbated by the persistent failure of successive state, territory and local governments to implement sound urban planning and zoning policies.”

Labour market and wages

A drop in NOM slows the rate of demand for labour, while also lowering the growth in the supply of labour. It means that a lower level of employment growth is required to keep the unemployment rate from rising because growth in the labour force is slower than otherwise. A drop in NOM means that headline employment growth will be lower, but the impact on the unemployment rate is negligible in the long run. In Australia’s case, however, there is likely to be a negative short run impact on the unemployment rate coming from job losses related to residential construction and some parts of the education sector that are impacted by lower NOM (students who stay more than a year are counted in NOM but not those that stay less than a year. Note that we do not include tourism here as most tourists do not stay for more than a year – NOM and short term arrivals are two different things).

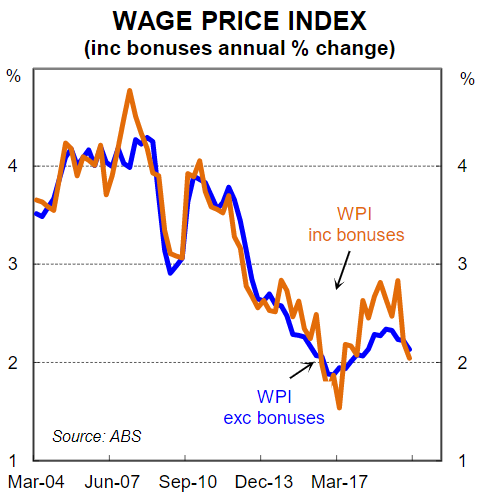

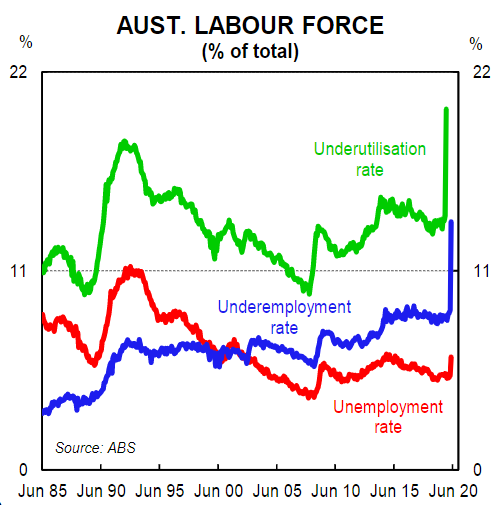

From a wages perspective, a high level of NOM augments the supply of labour beyond what would have naturally occurred. That intensifies the competition for existing jobs, while of course also adding to the demand for labour. The bigger the supply side shock, the more that the competition for existing jobs intensifies. This puts downward pressure on wages initially, but its effect should only be temporary. However, if the supply side shock continues when slack is elevated the temporary impact may not prove to be so short lived. This has been the pre-COVID-19 case in Australia since the end of the mining boom. We have essentially run a high immigration program via elevated NOM based on the notion of skills shortages even when there has been plenty of slack in the labour market (chart 9).

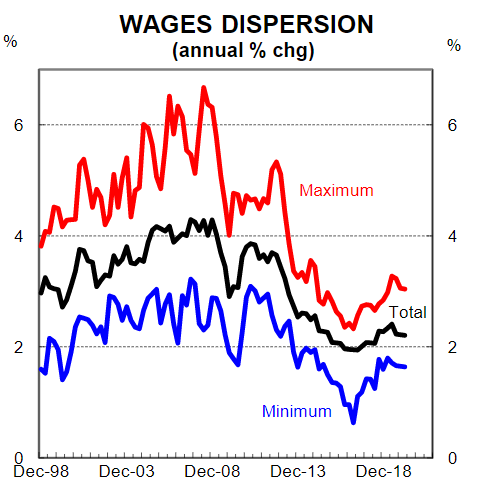

In 2018/19, the “Skill Stream” accounted for ~70% of the total migration programme outcome. From the perspective of an employee, working in an industry that has a skills shortage means that the labour market in that profession should be tight. In industries with skills shortages, bargaining power between the employee and employer should move more favourably in the direction of the employee and higher wages should be forthcoming. But in Australia’s case there has been a lack of evidence of widespread skills shortages based on the broad-based weakness in wages growth (chart 10 & 11).

The relatively high intake of skilled workers in the past looks to have been a pre-emptive strike on the expectation that there will be skills shortages in the future. If NOM is lowered on a permanent basis then “skills shortages” are likely to manifest themselves over time because employees will find it harder to hire from abroad. This means that employees may see a boost in their bargaining power that is independent of the level of slack in the local labour market. Essentially talent is a scarce resource if firms cannot hire from a global pool of labour as they may have previously done.

Wages growth is going to very weak in Australia for several years now regardless of the drop in NOM because of the big increase in the unemployment and underemployment rates and resultant increase in labour market slack. But we wouldn’t be surprised to see some pockets of wages growth due to the sudden drop in NOM as firms cannot hire workers from abroad. Fruit picking is an obvious example that illustrates the point. It may be the case that local primary food producers will need to offer higher wages for fruit picking to attract local workers to the jobs. The bottom line is that there will be opportunities for local workers to push for higher wages if the demand for labour exceeds its supply.

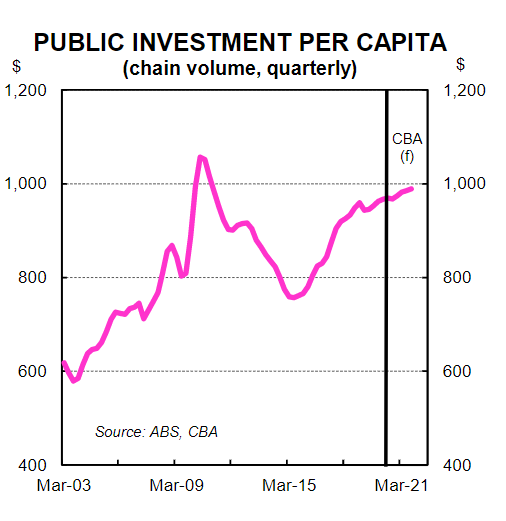

Public Investment

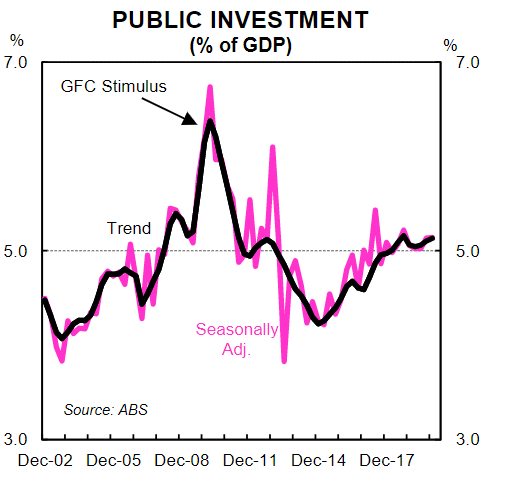

Public investment has risen as a share of GDP in recent years as many state governments as well as the federal government have focussed on relatively large infrastructure programs (chart 12). The COVID-19 pandemic is not expected to result in any material changes to the public works programs. This means that as NOM declines public investment per capita will rise (chart 13). This should be considered a positive development for all Australians as more public investment per person means a lift in living standards, all else equal.

As a basic rule of thumb, public investment should at least be sufficient in size to both replenish the capital stock and match the lift in population. If the population is growing rapidly then underinvestment in the number of schools and hospitals, as well as public transport and a host of other vital public facilities, leaves households worse off. The drop in NOM will allow infrastructure to partially “catch up” to the growth in population.

Time for reflection?

Australia is one of the most desirable places in the world to live, work, holiday, retire and raise a family. The major cities of Australia are almost always near the top of the various lists that rank cities by “quality of life” metrics. Australia usually scores very well on measures that relate to the political and social environment, economy, healthcare, education, public services and climate. In addition, Australia is blessed with an endowment of natural resources that is second to none. It is indeed the ‘lucky country’ and policymakers should seek to preserve the things that make Australia such a great place.

There has been a lot of discussion around policy reforms that may result from the COVID-19 pandemic – the phrase ‘never waste a good crisis’ has been thrown around frequently over the past two months. The push for productivity enhancing reforms is the correct one because improvements in productivity raise living standards. Indeed living standards should take centre stage in the policy debate.

The drop in NOM due to COVID-19 is an opportunity for policymakers to review the long term strategy related to population growth and immigration in Australia. The targeted level of NOM and immigration over the medium to longer term should strike the right balance between fostering growth in the economy while preserving and indeed enhancing living standards of the existing population. A full appraisal of the benefits and costs of various levels of NOM and by extension immigration should be undertaken to determine the optimal level of NOM for Australian residents.

This is a brilliant report that supports MB’s arguments around immigration over the past eight years.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.