CBA has released debit and credit card data showing that Australian consumers are increasing their expenditure on a range of household goods following a big slump during the COVID-19 lockdown:

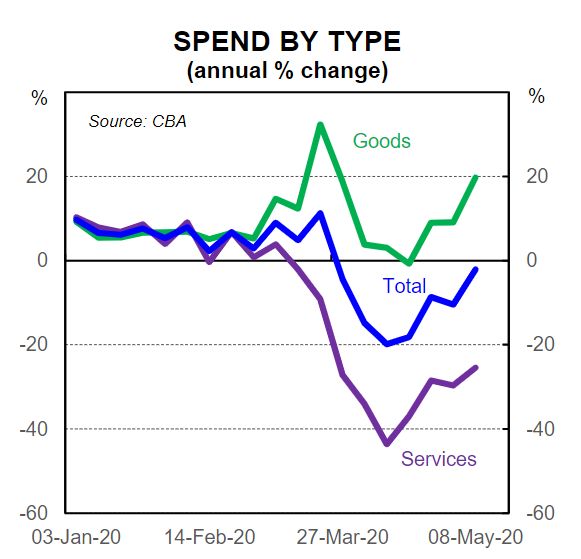

Analysis from our CBA credit &debit card spend data to the weekending 8May continues to suggest household expenditure has shifted gears. Total credit and debit card spend is still down on year ago levels and the levels prior to the COVID-19 outbreak and economic shutdown measures. But the annual rate of change has improved again. Put another way, the second derivative has turned positive, which means that the overall level of spending is now ‘less bad’.

Total spending over the week to 8 May is down by around 2% on year ago levels. That is a clear improvement on spending to mid-April, where spending was down by almost 20% on year ago levels. It is still early days and our data is somewhat volatile. But it looks to be the case that households have stepped up their rate of expenditure over the second half of April and now the first week of May compared with earlier in April. Some pent up demand in the lead up to Mother’s Day may also be behind the latest result.

There are three points to note on the latest data:

The comparison to one year ago suggests only a small fall in expenditure. In reality though household expenditure in April and May 2019 was very lacklustre. There was considerable uncertainty in the lead up to the Federal Election held on 18 May, house prices had been falling for close to 18 months and the unemployment rate was rising. The RBA cut the cash rate in June 2019,but speculation was rife of an earlier rate cut.

Instead we suggest comparing current momentum to pre-COVID-19,where the Australian economy had started to show a gentle turning pointat the start of the calendar year. In the first eight weeks of 2020 household expenditure was running around 8% higher than a year ago. Based on this household expenditure is currently 10% lowerthan this pace.Within this fall therehave been clear spending pattern changes.

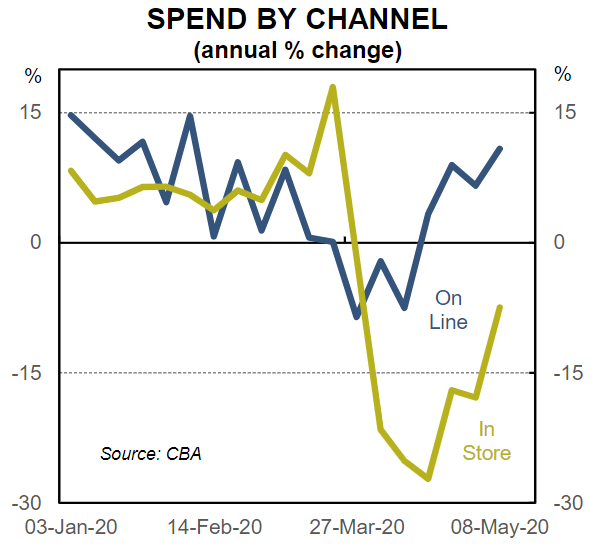

A preference for contactless payment and spending on-line rather than cash and instore spending to help control the transmission of the virus, could also be overestimating the improved momentum.

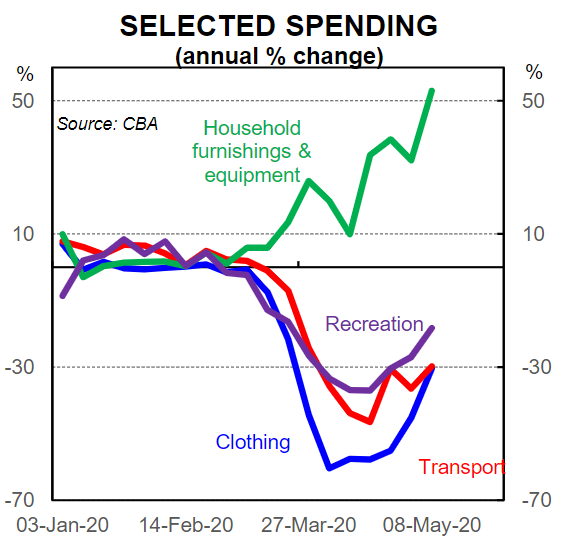

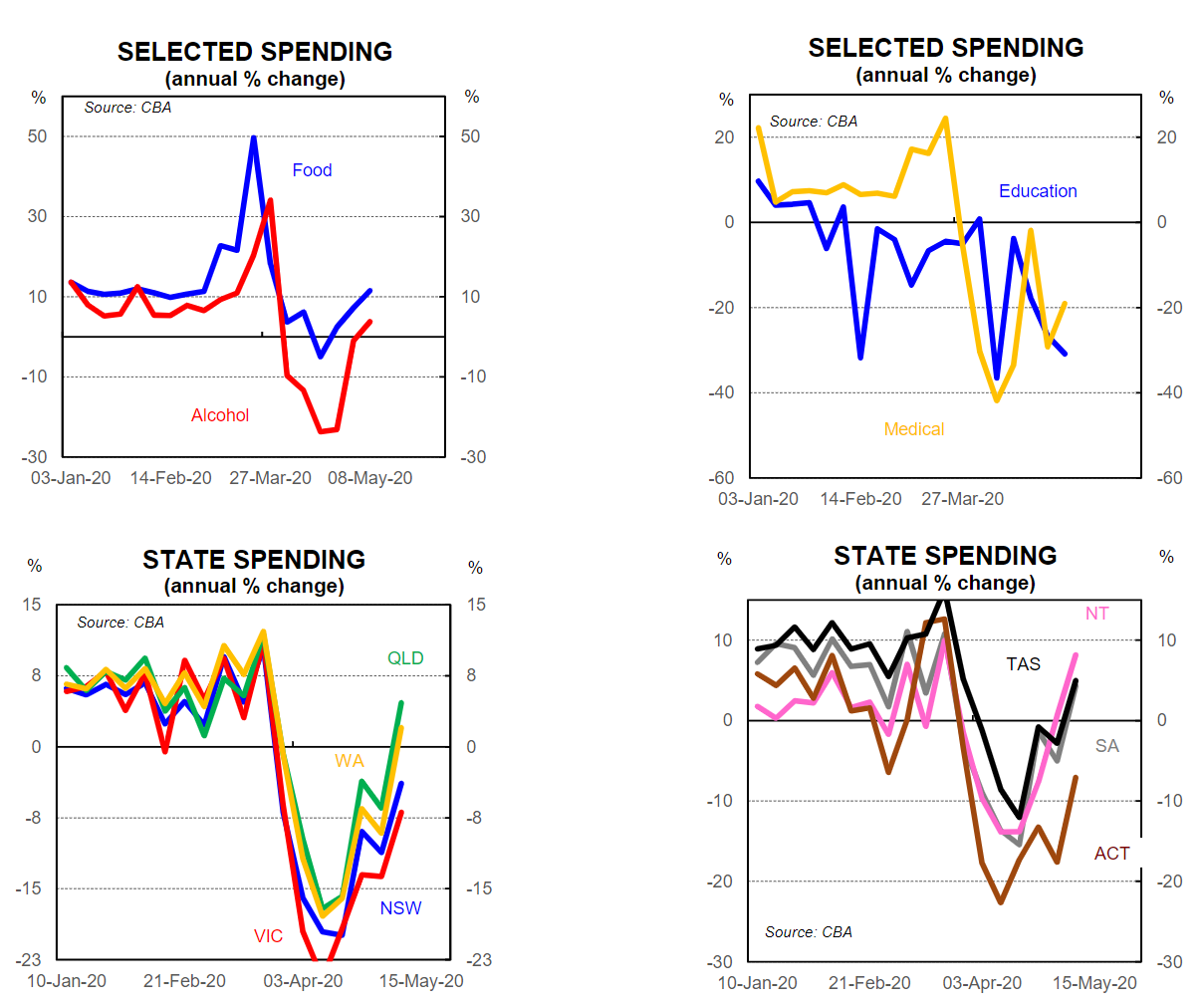

By spend category, there has been broad-based improvement in momentum over the past week. Spending is still down sharply on transport (-30%), clothing (-30%), education (-31%) but each is less bad than in mid-April. Spending it still weak on personal care (-29%), recreation (-18%) and medical (-19%). Food and alcohol card spending is now rising, up 12% and 4% respectively on a year earlier. The real outlier though is spend on household furnishings & equipment. Spending is up 53% compared to levels a year earlier. The more time we spending at home it seems the more we want to make changes to it.

The smaller states and territories were the outliers for the week ending 8 May, recording positive growth compared to a year ago. Queensland also turned positive, in line with an earlier rollback from shutdown measures. The ACT and Victoria continue to underperform most across the board and were down 7% compared to a year ago. NSW is still underperforming the national average, down 4% but continues to outperform its southern neighbour.

We do expect to see more spending shifts as some restrictions are being lifted in each state. There are differences as to what is allowed in each state and we would expect to see this represented in this data. Particularly we could see a further lift in in-store purchases as more major shop-fronts are reopened and consumers build back some confidence to spend. Some states are reopening cafes & restaurants for limited use. Any further easing in restrictions coupled with more positive news on the transmission of COVID-19 could be expected to further support household expenditure in the near term.

Obviously these results need to be viewed with caution, given more transactions are going through via card with a lot of businesses not taking cash.

Nevertheless, the change in momentum is welcome and signals that we are well past the bottom.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.