By Gareth Aird, Head of Australian Economics at CBA

Key Points:

- CBA credit & debit card spend indicates that spending momentum has improved over the last two weeks.

- Total spending is still well down on year ago levels, but the most recent data suggests that the pulse of spending has picked up across a range of goods and services and across all states and territories.

- Online sales have lifted sharply over the past few weeks, particularly for retail items.

Insights on spending from CBA credit & debit card data:

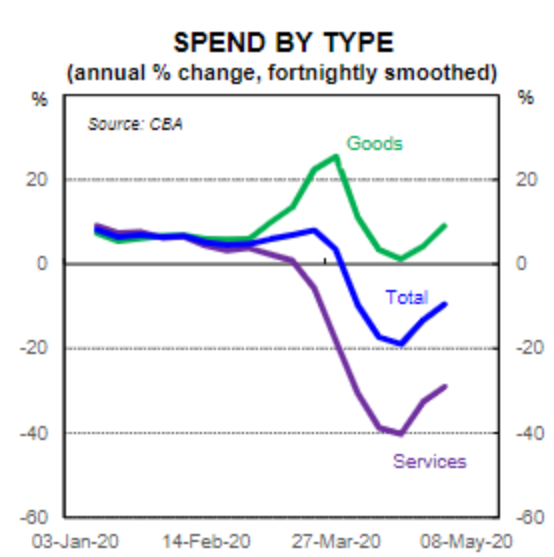

Analysis from our CBA credit & debit card spend data to the fortnight ending 1 May offers a glimmer of hope that we may be past the low point in terms of the contraction in household expenditure. Total credit and debit card spend is still well down on year ago levels. But the annual rate of change has stepped up. Put another way, the second derivative has turned positive which means that the overall level of spending is now ‘less bad’.

Total spending over the fortnight to 1 May is down by 10% on year ago levels. That’s an improvement on spending to mid-April which was down by almost 20% on year ago levels. It is still early days and our data is somewhat volatile. But it looks to be the case that households have stepped up their rate of expenditure over the second half of April compared with the first half of the month. Our latest data predates any easing in restrictions. So it may be that households have responded positively to the slowdown in the rate of transmission of COVID-19. The improved news on the medical front may have given them a boost in confidence to go out and spend at those businesses that have not had to close their doors as a result of the shutdown.

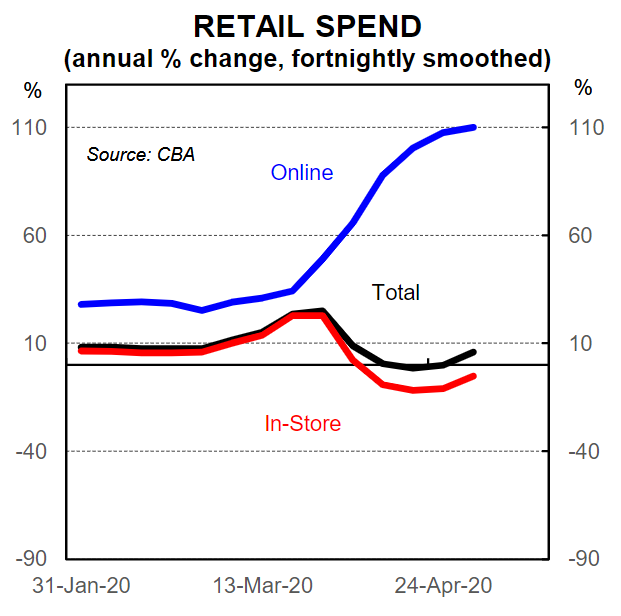

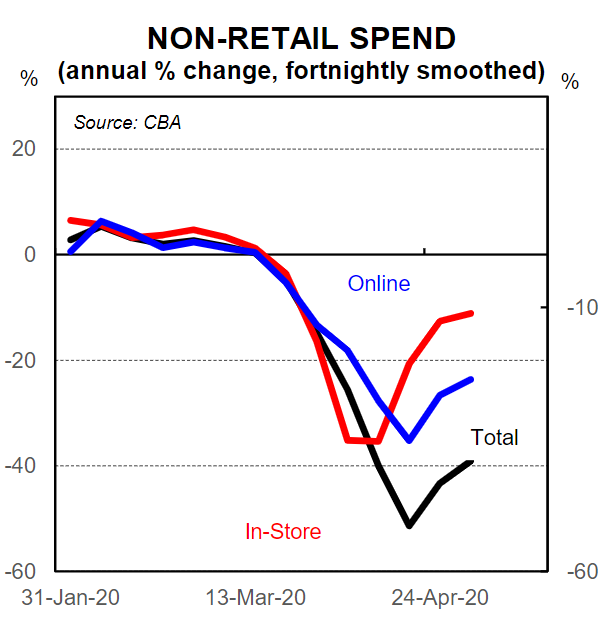

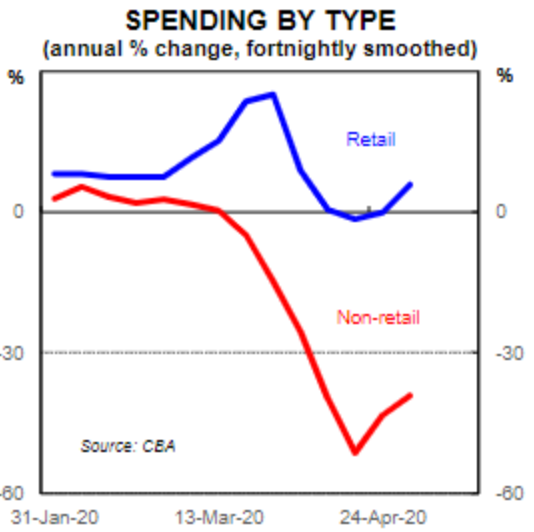

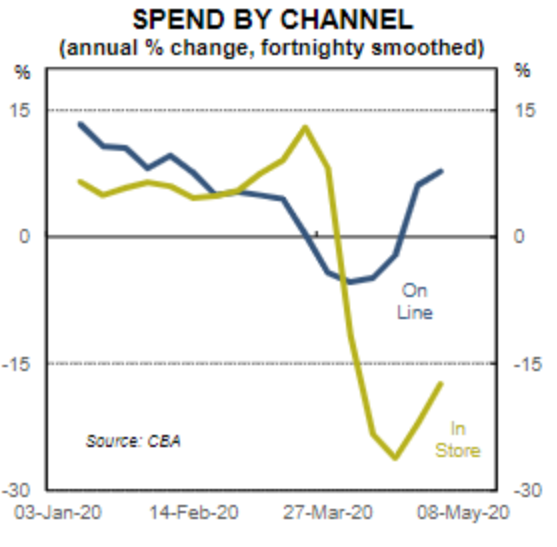

It also looks like households have been more eager to get online, click the mouse and fill up the virtual shopping basket. Spending online has picked up materially over the past few weeks. Indeed spending on retail items online is up by 110% over the past fortnight compared to the same period a year earlier. Spending both online and instore remains down over the year on non-retail goods and services. But the rate of decline has eased over the past fortnight. Our data indicates that the ABS measure of retail trade will look a lot better than total household consumption over Q2 20. The main reason is that supermarkets comprise a much greater share of retail trade than they do of total household expenditure.

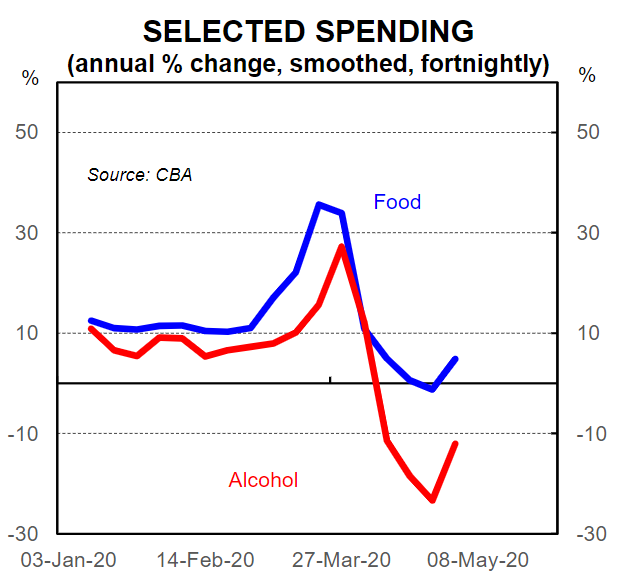

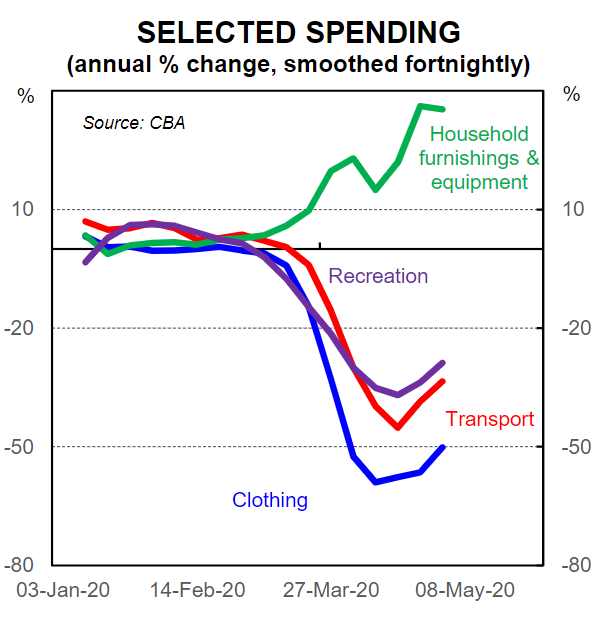

By spend category, there has been broad-based improvement in momentum over the past fortnight. Spending is still down sharply on clothing (-50%/yr), transport (-34%/yr), recreation (-29%/yr), personal care (-41%) and medical care and health (-16%/yr). But rates of change have improved. Spending is still up strongly on household goods and furnishings (+35%/yr).

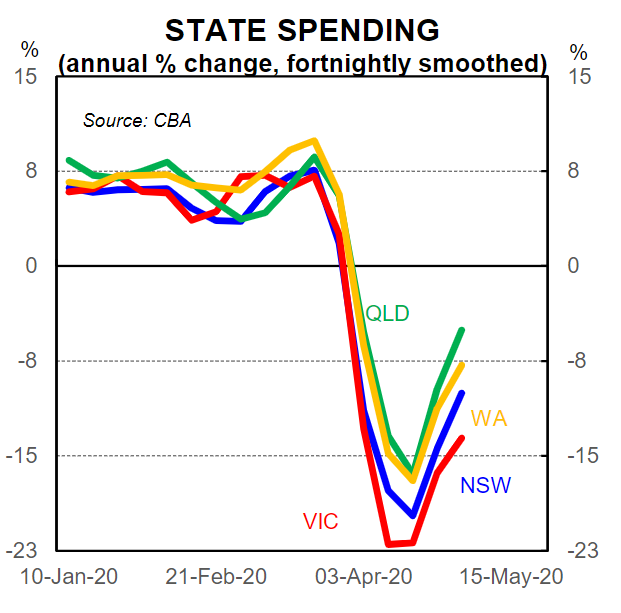

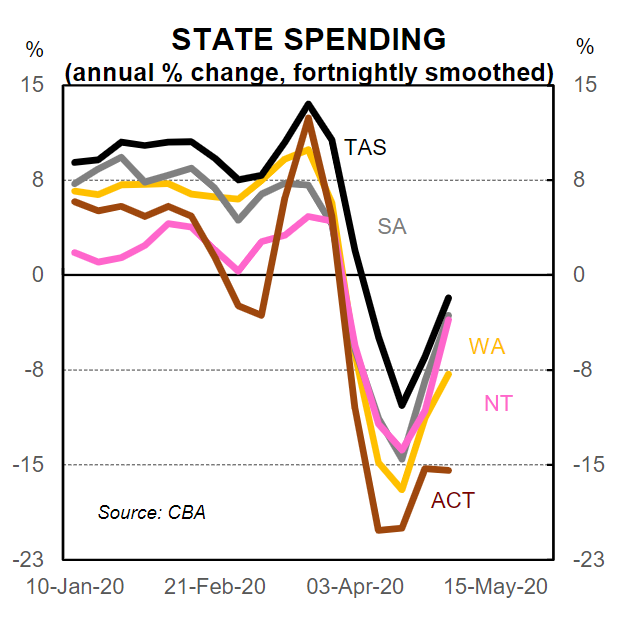

Credit and debit card spend by state paints a similar picture. The spending pulse looks to have picked up in all states and territories over the past fortnight. Tasmania is the outperformer with spending down ‘just’2% on year ago levels. NSW and Victoria continue to underperform against the other states. Spending is down by 10% in NSW and by 14% in Victoria on year ago levels. QLD, WA, SA and the NT have all done better than the national rate.

Our latest data bolsters our view that the contraction in Q2 20 household expenditure will not be as big as the 20%/yr fall in goods and services spend that our credit and debit card spend was tracking at mid-April. We expected to see some degree of rebound in card spend and it looks like that is occurring right now. Any easing in restrictions coupled with positive news on the transmission of COVID-19 could be expected to further support household expenditure in the near term. Our forecast is for household consumption to contract by12% over Q2 20 and for GDP to fall by 8.5%over the same period.

See below for a variety of charts that capture the latest changes in spending from our CBA credit & debit card spend, including data by state.