For nearly 30 years, Australia’s compulsory superannuation system has provided strong tailwinds for the Australian share market.

Since compulsory superannuation was first introduced in 1992, mandatory contributions have grown from 3% of employee wages to 9.5% currently.

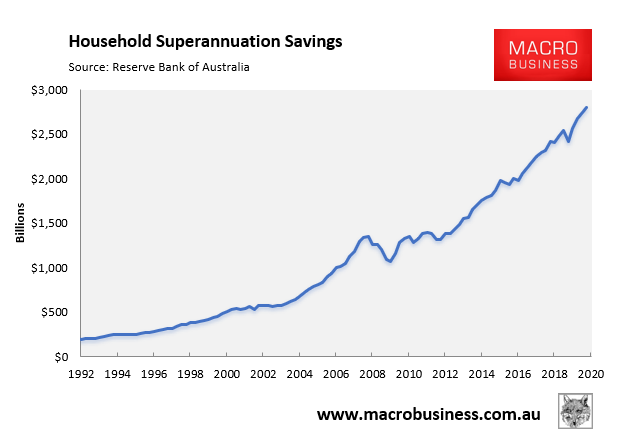

In turn, this strong inflow of contributions caused superannuation funds under management to grow almost exponentially, as evidenced by Australia’s total superannuation savings pool ballooning from around $200 billion in 1992 to $2,800 billion as at December 2020:

The lion’s share of these superannuation funds have flowed into Australia’s share market, thus increasing demand and inflating share valuations.

However, the Morrison Government’s early release policy, alongside falling inflows as Australians lose their jobs due to the COVID-19 shutdown, means that net inflows into superannuation could turn negative. This would place significant downward pressure on share valuations, according to investment bank UBS:

Workers who have lost their jobs or been stood down are eligible to withdraw up to $20,000 from their super by the end of September under emergency coronavirus crisis measures. The federal government estimates 2.3 million people will withdraw $29.5 billion from their super.

UBS equity strategist Jim Xu said this figure represented 1.1 per cent of total super balances.

Local funds had 27 per cent of their assets tied up in Aussie stocks before COVID-19 struck, indicating that about $8 billion in shares listed on the Australian Securities Exchange will need to be sold, he said…

Such an outcome, combined with slowing contributions due to lower employment and emergency withdrawals, would halve the amount of money from contributions and dividend income that super funds had to invest from $89 billion last financial year to $44 billion this financial year, Mr Xu said.

“Funds’ ability to purchase assets could fall significantly,” he said. “Super funds are the only sector to have increased their ownership of Australian shares over the past 20 years.

“Hence, any decline in the ability of super funds to purchase Australian shares could be negative for demand for Australian equities.”

The long-run outlook is also negative. Baby boomers hold the lion’s share of Australia’s savings. Therefore, as they retire they are likely to become net sellers of financial assets in order to fund their retirements. This would place downward pressure on valuations, other things equal.

These dynamics may help to explain why Australia’s superannuation industry lobbies so hard to have the superannuation guarantee lifted from 9.5% to 12%. Not only would this increase funds under management (other things equal), lifting superannuation management fees. But it would also help put a floor under share valuations by offsetting withdrawals from the large baby boomer generation.

Put another way, raising the superannuation guarantee to 12% is a guaranteed way of maintaining positive net superannuation inflows, thus keeping Australia’s superannuation bubble inflated.