DXY was soft last night:

The Australian dollar universally sagged:

Gold was firm:

Oil too:

Dirt fell:

And miners:

EM stocks rolled:

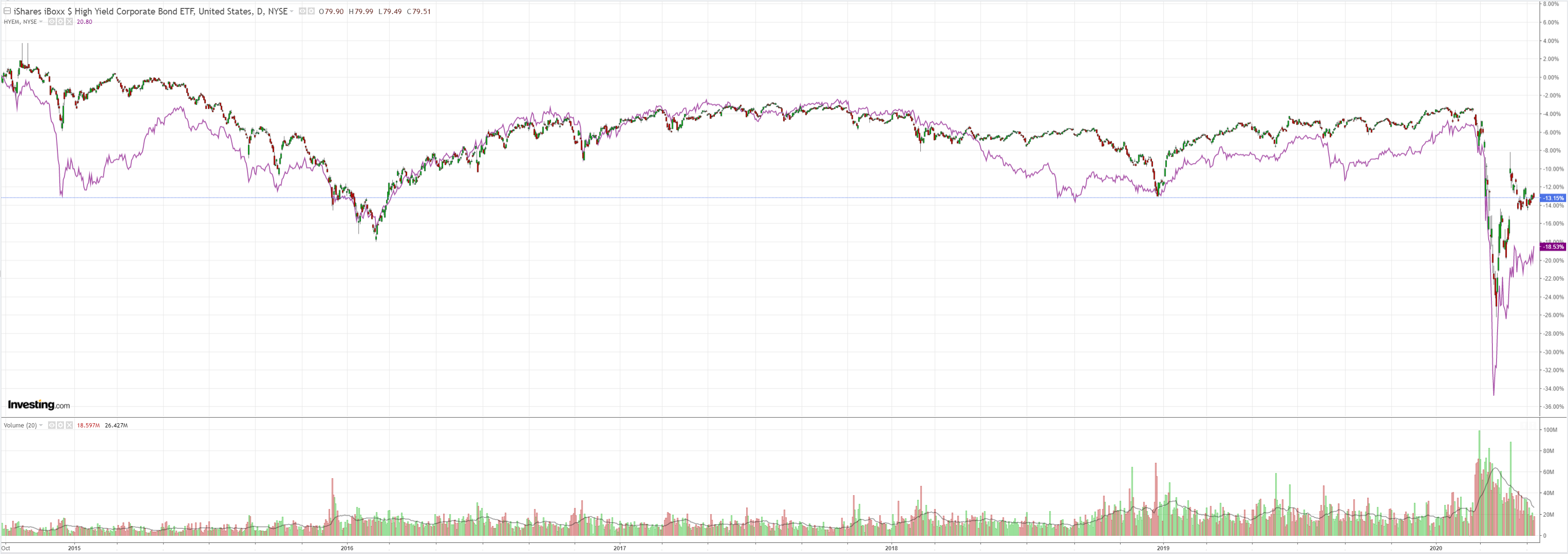

Junk lifted as the Fed began to buy:

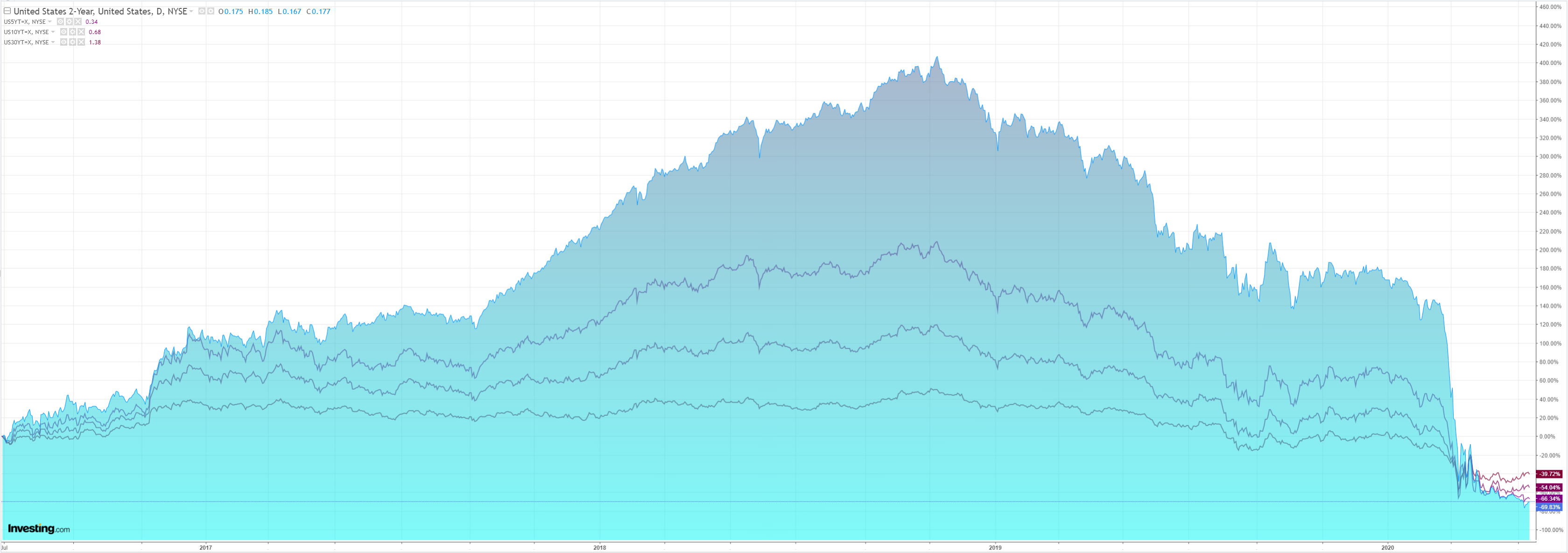

Bonds were bid:

Stocks were bashed:

Westpac has the wrap:

Event Wrap

COVID-19 update: The global case count, according to the latest data from John Hopkins University, indicates 76k new confirmed cases worldwide on 11 May, vs 78k the previous day and vs 99k at the peak on 12 April. Whereas in March daily cases accelerated, in April they have trended sideways.

US head of infectious diseases, Fauci, warned in testimony to a Senate hearing that an easing of restrictions too early leading to serious consequences.

US headline CPI fell by 0.8%m/m, as expected, for an annual pace of +0.3%y/y, (vs est. +0.4%y/y). The core measure, ex-food and energy, fell by a record -0.4%m/m (vs. est. -0.2%) for an annual pace of +1.4%y/y (est. +1.7%y/y).

The US NFIB small business survey for April fell by less than expected, at 90.9 (vs est. 83.0, prior 96.4). Although own business prospects reflected record lows for sales expectations, the outlook for the economy was surprisingly positive over the coming six months.

Fed speakers (Bullard, Kaplan, Kashakari, Harker, and Mester) were consistent in their messages, keeping policy low for a long period but resistant towards a negative interest rate. They also stressed the importance of seeing a return to activity post lockdown, although Harker did warn of the risks of early exits.

BoE Dep. Gov. Broadbent underscored the MPC’s preparedness to provide further support as needed with all tools at their disposal under review, including, on questioning, negative interest rates.

Event Outlook

Australia: The day will open with the May Westpac-MI Consumer Sentiment Index. In the April update, sentiment plunged to 75.6, recording the largest monthly fall in the 47 year history of the survey. Developments over the last month have been mixed. On the positive side, the Australian coronavirus count has been lower than feared and restrictions will be eased earlier than expected. However, news around the economy has confirmed the heavy impact on activity and jobs. Following this, the Q1 Wage Price Index will be released. Westpac is looking for a weak print of 0.5% in Q1 to be followed by a material slowdown as the coronavirus shock plays through.

New Zealand: The major event of the day will be the RBNZ policy decision. With the OCR on hold at 0.25%, the focus will be on the QE program which Westpac expects will be increased to $60bn. Markets will also be interested in forward guidance on the OCR, the RBNZ in March committing to no changes before March.

Euro Area: April industrial production will be released. The market is looking for the largest monthly fall on record at -12.5%.

UK: The market expects a 2.6% contraction in the preliminary read of Q1 GDP. Despite the sharp fall (the likes of which have not been seen since 1974), the UK has thus far fared better than the continental majors.

US: The PPI will round out the day. The market expects that factory price deflation will continue with a print of -0.5% in April.

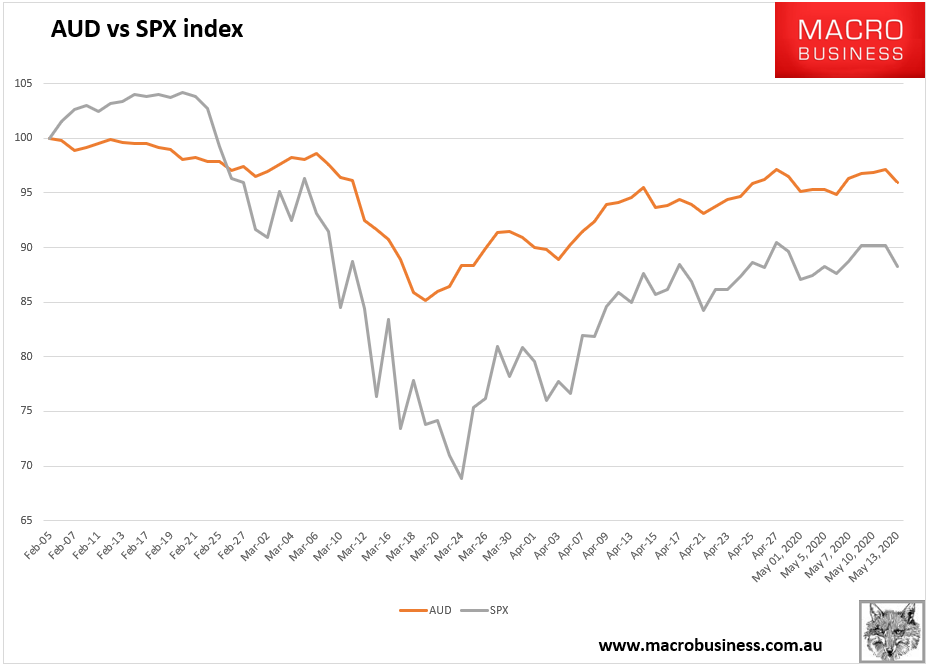

The only chart that matters for the AUD remains this one:

Follow the stocks!