DXY was strong last night:

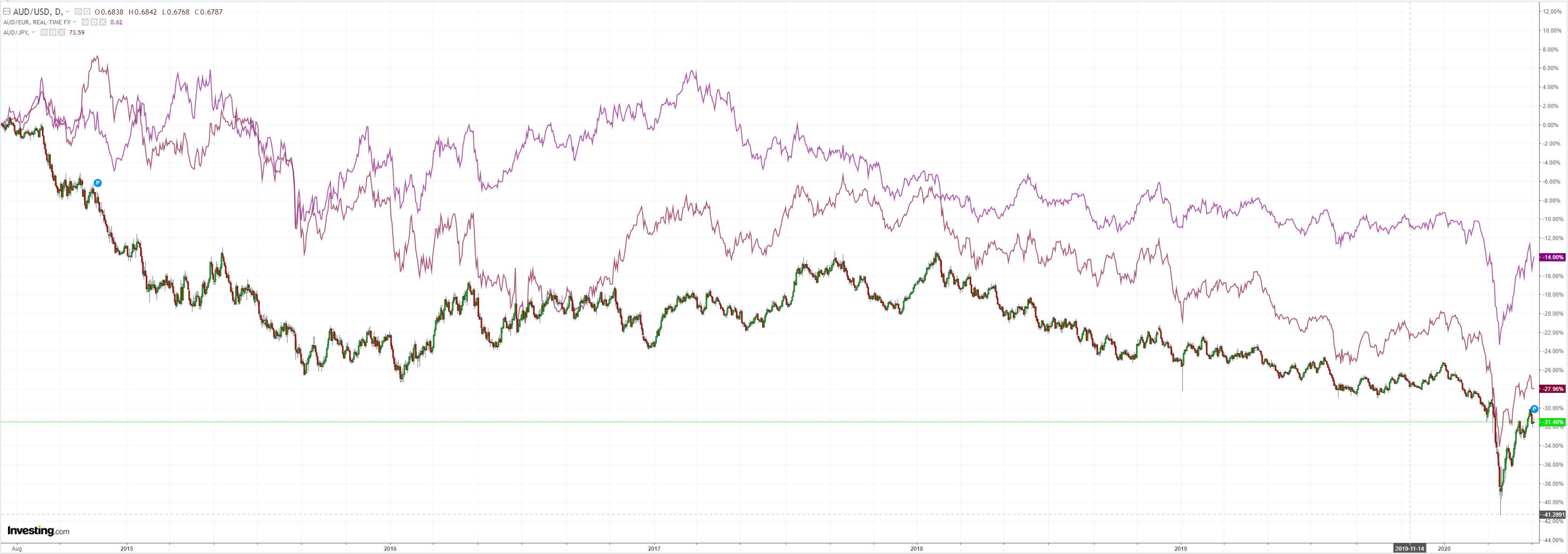

The Australian dollar was mostly soft:

Gold was stable:

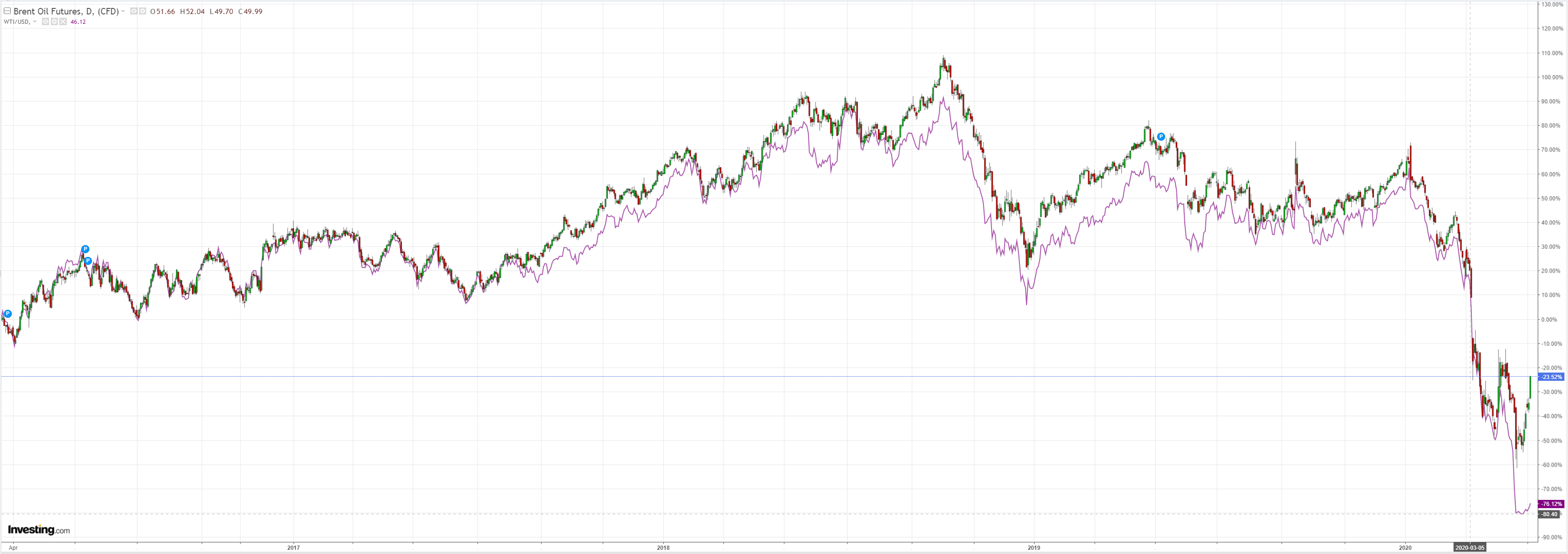

Oil has likely bottomed but Brent has overshot:

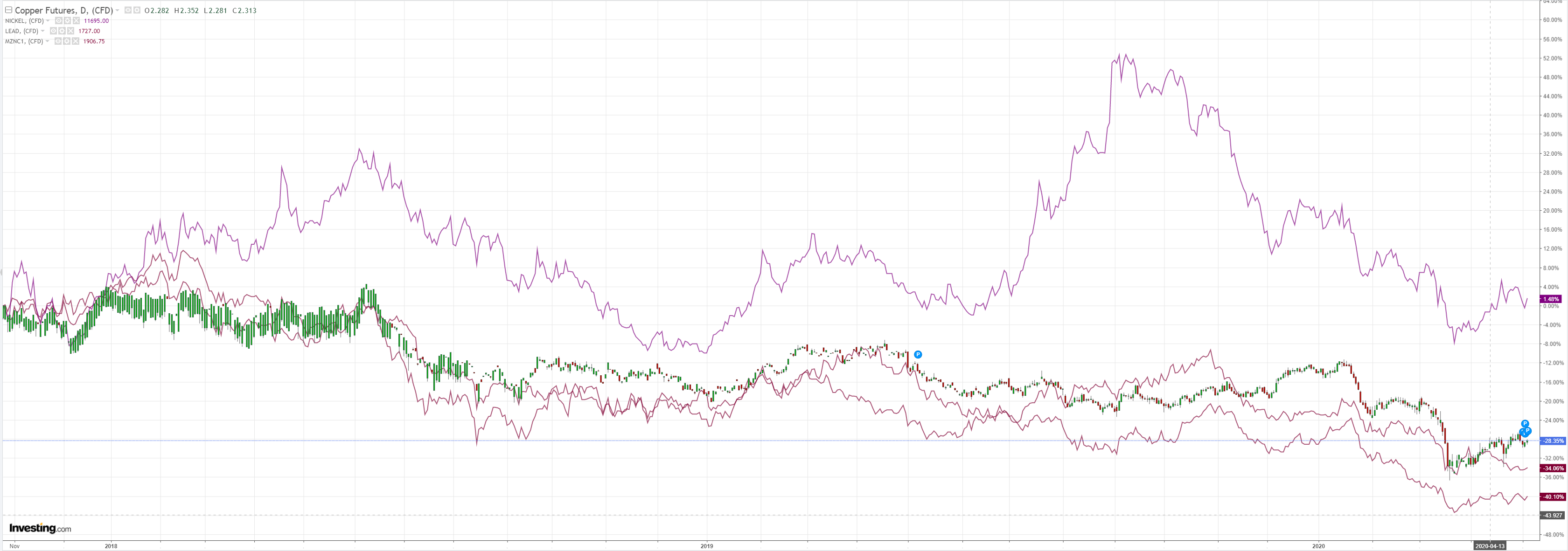

Dirt was firmer:

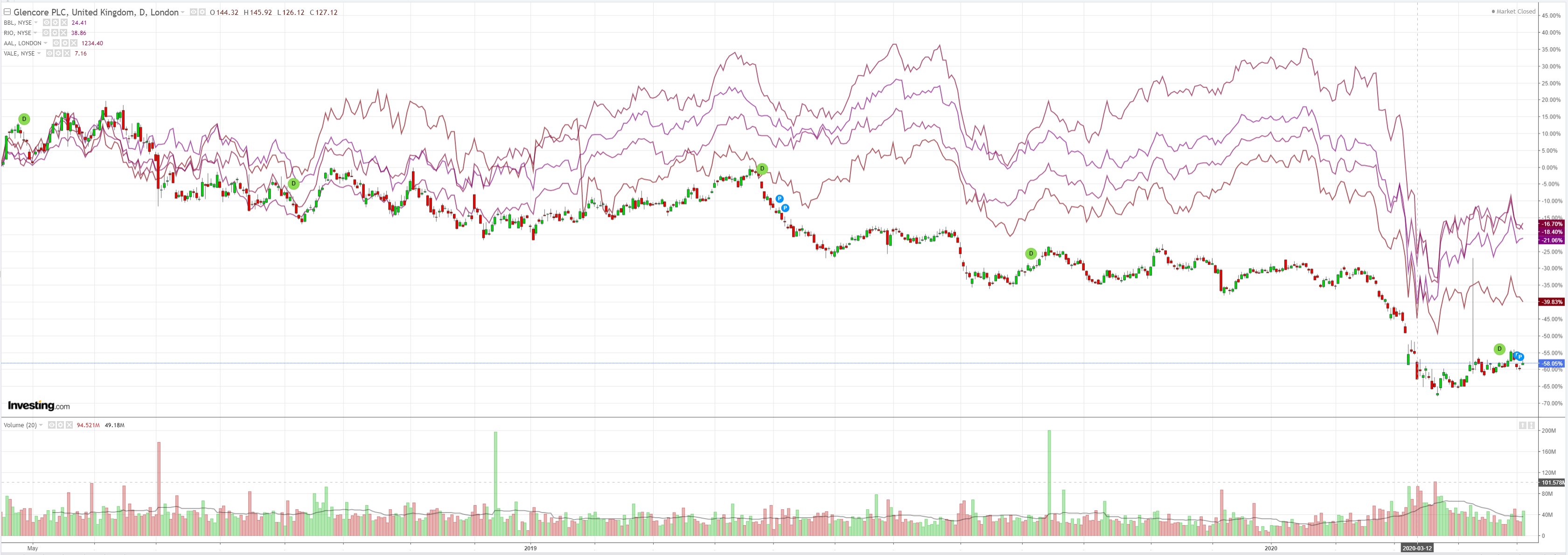

Miners not so much:

EM stocks struggled:

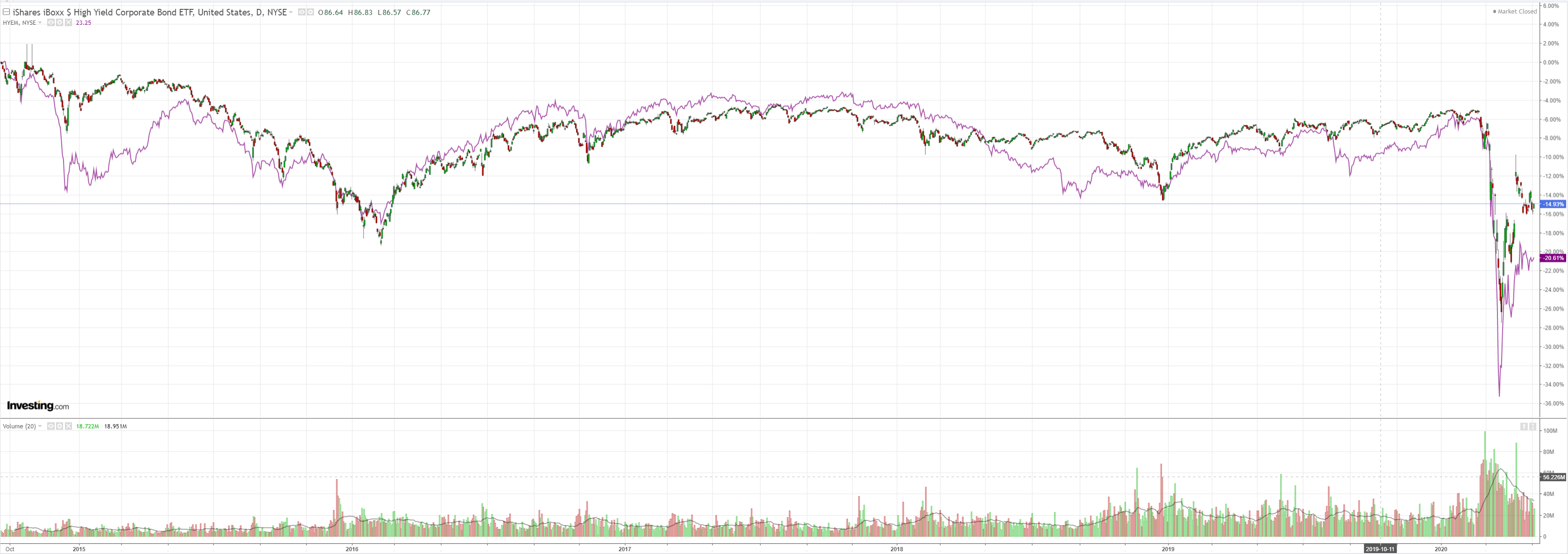

Junk too:

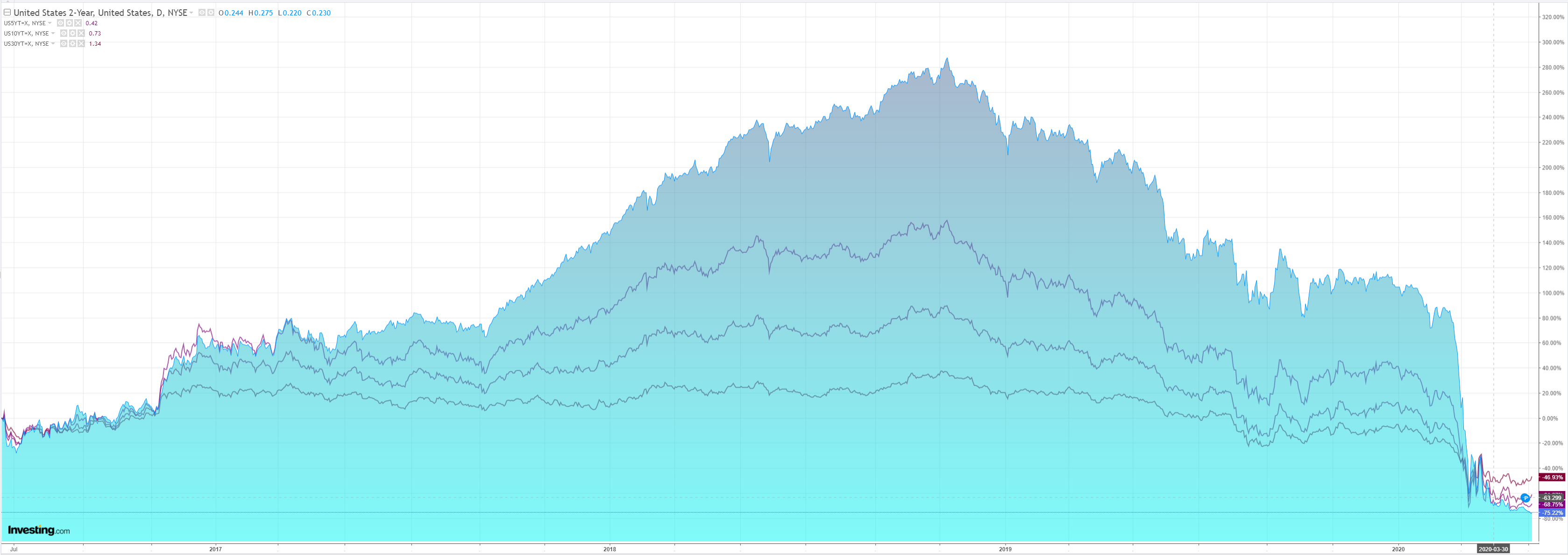

Bonds were soft:

As stocks rebounded:

Westpac has the wrap:

Event Wrap

COVID-19 update: The global case count, according to the latest data from John Hopkins University, indicates 76k new confirmed cases worldwide on 4 May, vs 79k the previous day and vs 102k at the peak on 24 April. Whereas in March daily cases accelerated, in April they have trended sideways.

US non-manufacturing ISM fell to 41.8 from 52.5 (slightly higher than expected). The business activity index fell to a record low of 26.0, from 48.0, and there were also sharp declines in the new orders (to 32.9 from 52.9) and employment (to 30.0 from 47.0) components.

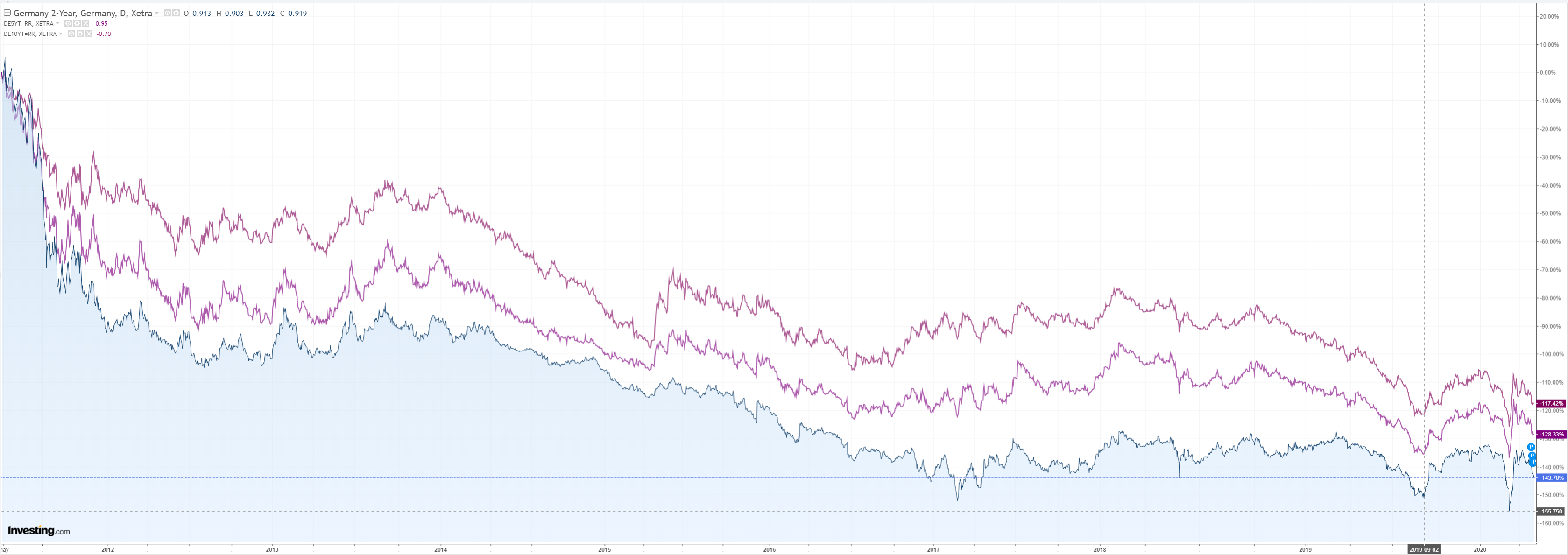

Germany’s constitutional court ruled that some of the measures its central bank (Bundesbank) is taking under the ECB’s asset purchase program are not covered by EU law. The Bundesbank must cease participation after three months unless the ECB can amend the rules.

The GDT dairy auction resulted in a 0.8% decline in prices overall, with NZ’s key export product – whole milk powder – up 0.1%.

Event Outlook

Australia: March retail sales will be the major release of the day. Westpac is looking for the extraordinary stockpiling surge of 8.2% reported in the preliminary estimate to be confirmed in the final read. Real retail sales for Q1 will also be published. Westpac expects a solid rise of 1.6%, largely driven by the strong nominal sales of March. However, the wider consumption measures reported in the national accounts may record a decline over the quarter – retail only makes up 30% of total consumption, and many other segments are more susceptible to a shock from the virus.

New Zealand: In the Q1 Household Labour Force Survey, Westpac is expecting a small drop in employment of 0.2%, dragging the unemployment rate up to 4.3% (from 4.0%). Because the survey is sampled continuously over the quarter, only a fraction of the lockdown will be captured in this release. Looking ahead, Westpac expects that the unemployment rate will peak at 9.5% in the June quarter. In addition, the Q1 Labour Cost Index is expected to increase by 0.5%, lifting private sector wage growth to its fastest pace since 2009. However, the index was measured in mid-February, and will miss the impact of the lockdown. Wages growth will be soft going forward, aside from government-mandated increases.

Asia: April Nikkei PMIs will be released for India, Hong Kong and Singapore.

Europe: March retail sales are due. The market expects a dramatic fall of 10.6% as lockdowns and precautionary savings disrupt spending. The Q1 flash GDP estimate has already highlighted the unprecedented collapse in activity.

US: For the April ADP employment change, Westpac expects that a record-breaking 22m jobs will be reported lost over month. As a stark contrast, the March print came in at -27k. At 3:30 am AEST, the FOMC’s Bostic will discuss the response to the virus.

Most markets have gone nowhere for three weeks now. For the time being at least, life is steadily leeching form the bear market rally pulse.

The Australian dollar is still beholden to it.