But the Australian dollar sank right along with it:

With EMs:

And gold:

Advertisement

Oil did better:

But not dirt:

Miners were hit:

Advertisement

EM stocks too:

Junk rose:

As most yields fell:

Advertisement

Bunds were uber-bid as the ECB demanded fiscal c0-operation rather than extending its programs:

Aussie bonds rallied:

Advertisement

Stocks corrected moderately:

Westpac has the wrap:

COVID-19 update: The global case count, according to the latest data from John Hopkins University, indicates 80k new confirmed cases worldwide on 29 April, vs 75k the previous day and vs 102k at the peak on 24 April. Whereas in March daily cases accelerated, in April they have trended sideways.

Eurozone Q1 GDP fell -3.8%q/q, as expected, but the French release posted a fall of -5.8%q/q and was followed by a sharper than expected rise in German April unemployment of +737k (est. +74.5k) to 5.8% (est. 5.2%, prior 5.0%). Eurozone March unemployment did not record such a sharp move, rising to 7.4% (est. 7.8%) from 7.3%, with reporting anomalies.

The Fed announced an expansion of its Main Street Funding package after recent consultations. It increased the scope and eligibility to assist SMEs.

US weekly initial jobless claims of 3.8m (for a six-week cumulative rise of almost 30mn) slightly exceeded the 3.5m median expectation. Chicago PMI fell to 35.4 (est. 37.7, range 25 to 44.8, prior 47.8). March personalspending fell -7.3%m/m (est. -6.2%m/m) with personal income falling -2.0%m/m (est. -1.5%m/m). The core PCE deflator fell from 1.8% y/y to 1.7% (vs 1.6% expected).

Event Outlook

Australia: The April AiG PMI is due. Although manufacturing spiked in the February update, any remaining strength is set to unwind. April CoreLogic home value index is expected by Westpac to post a modest gain of 0.3% as coronavirus begins to disrupt the housing market.

New Zealand: The April ANZ consumer confidence index is expected to remain subdued, following a sharp fall in March.

US: Construction spending is expected to fall by 3.5% in March; such a read would represent the sharpest monthly decline since 2011. The April ISM manufacturing index is due. The market expects a substantial decrease to 36.0 as supply disruptions and the coronavirus demand shock weigh on the manufacturing sector.

A lot of month-end selling and rebalancing no doubt. The Australian dollar fall once again illustrating that it is nothing more than proxy for stocks at the moment, via Nomura:

Advertisement

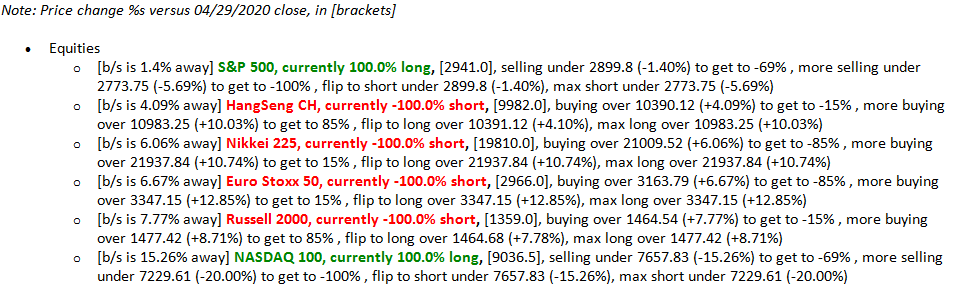

McElligott today writes that his CTA model’s S&P futures position flipped yesterday, from the recent “-69% Short” signal to the current “+100% Long,” they bought a total of $36.8BN across Emini futures yesterday.

And as stocks seek to recapture 3,000 and the Nasdaq unchanged for the year, McElligott points out that the “buy to cover” triggers are getting closer across various other Global Equities futures legacy “short” positions as well, and worth keeping track of (still “-100% Short” in HSCEI, Nikkei, Estoxx & RTY):

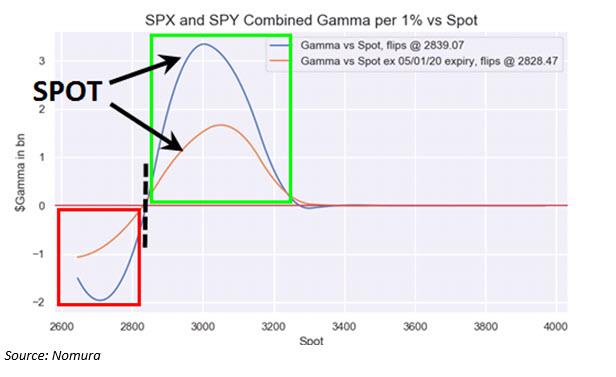

Meanwhile, as pointed out previously, the higher the market rose – start of the recession notwithstanding – the greater the gamma push, and as we have recently seen the aggregate SPX/SPY dealer positioning flip from what had been “short gamma” to then a “neutral gamma” one and now increasingly outright “long gamma” (approaching overwriter strikes), Nomura “sees the benefits of “vol suppressing” dealer hedging behavior with these grinding, less spastic market moves, while the largest Gamma strikes shift higher on the move, with the biggest gamma strike now at the nice, round 3,000.

US Equities continue to sit near 2 month highs, to the shock of many who “fundamentally” remain focused on the obviously horrific economic ramifications of the COVID19 shutdown…but without an appreciation of the ability within the Equities market to “pull forward” future inflections, on top of client positioning dynamics, vol dealer positioning / hedging realities and the “sling-shot” that is a market structure built-upon “negative gamma” which creates this seemingly rolling “Crash DOWN, then Crash UP” cycle.

Effectively, in a “VaR” risk management world where volatility is the exposure toggle—the implications of vol resetting LOWER (following a “macro shock” spike) then has a tendency to contribute to sling-shot HIGHER in spot Equities, as vol control & target volatility strategies mechanically need to re-leverage risk exposures, while “expensive vol” / inverted VIX term-structure, per the back-testing model-driven systematic community, signals an “all-clear” to load back into “short vol” behavior…all of which feeds into the risk virtuous cycle.

For the time being at least, wherever the robots go, the Australian dollar will follow.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.