DXY took off last night. CNY is close to breaking down to its lowest levels since the GFC:

The Australian dollar was bashed versus DMs:

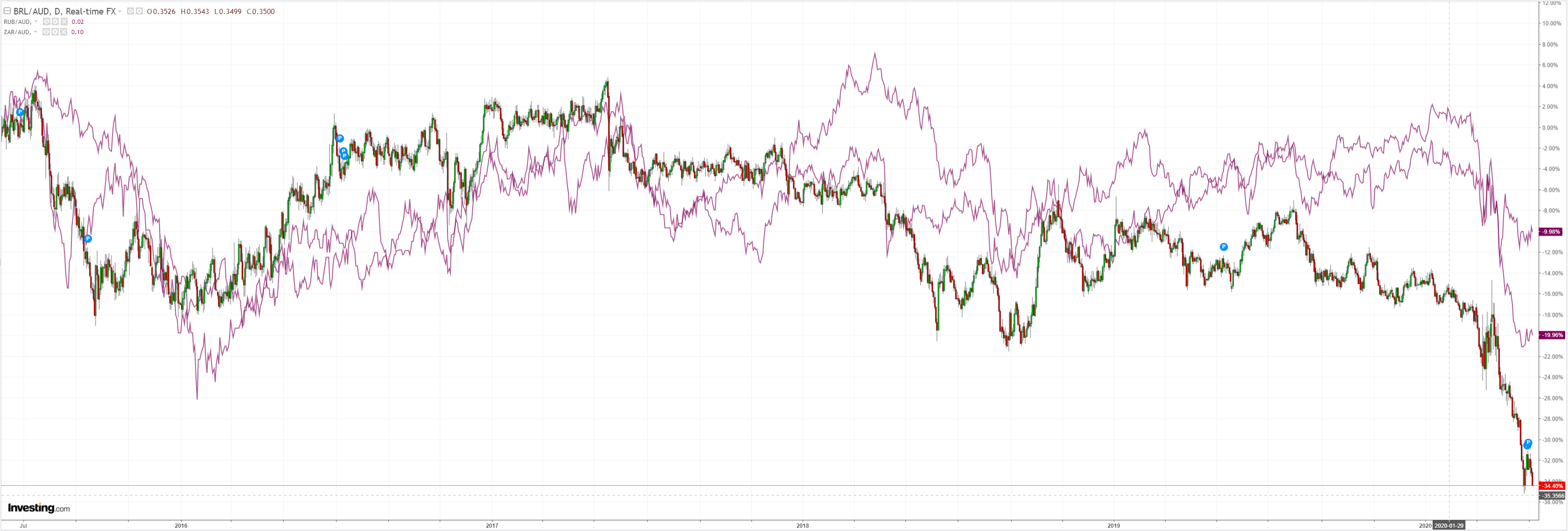

EMs were hit even harder:

Gold sagged:

Oil too:

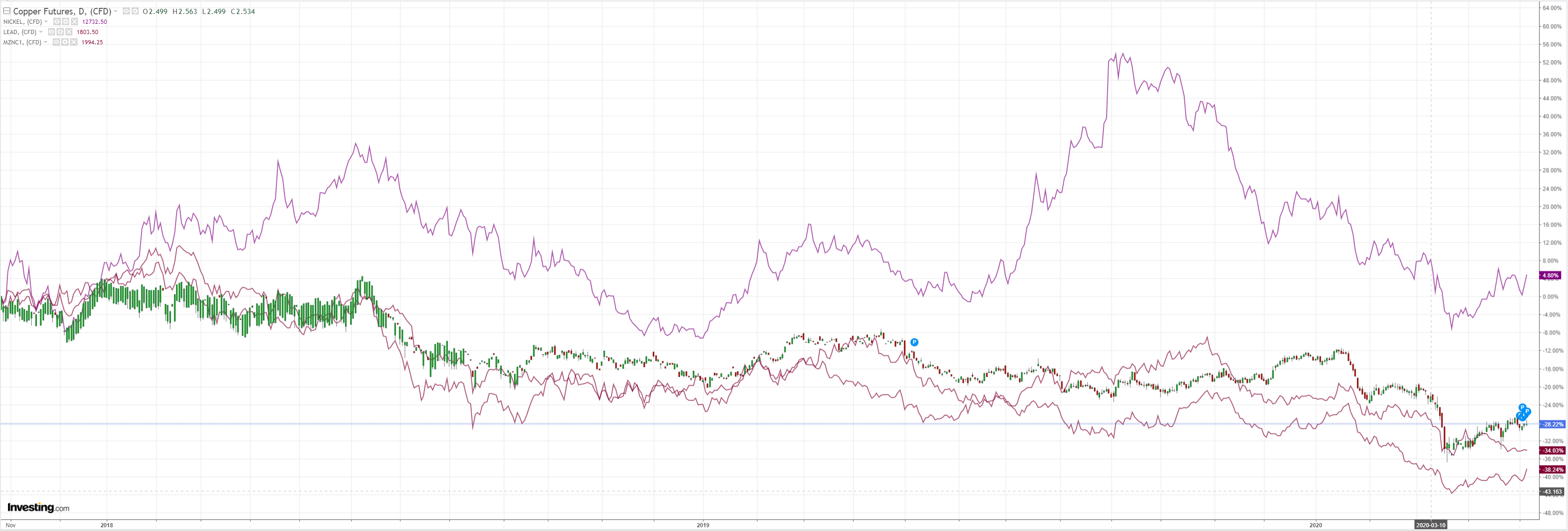

Dirt did better:

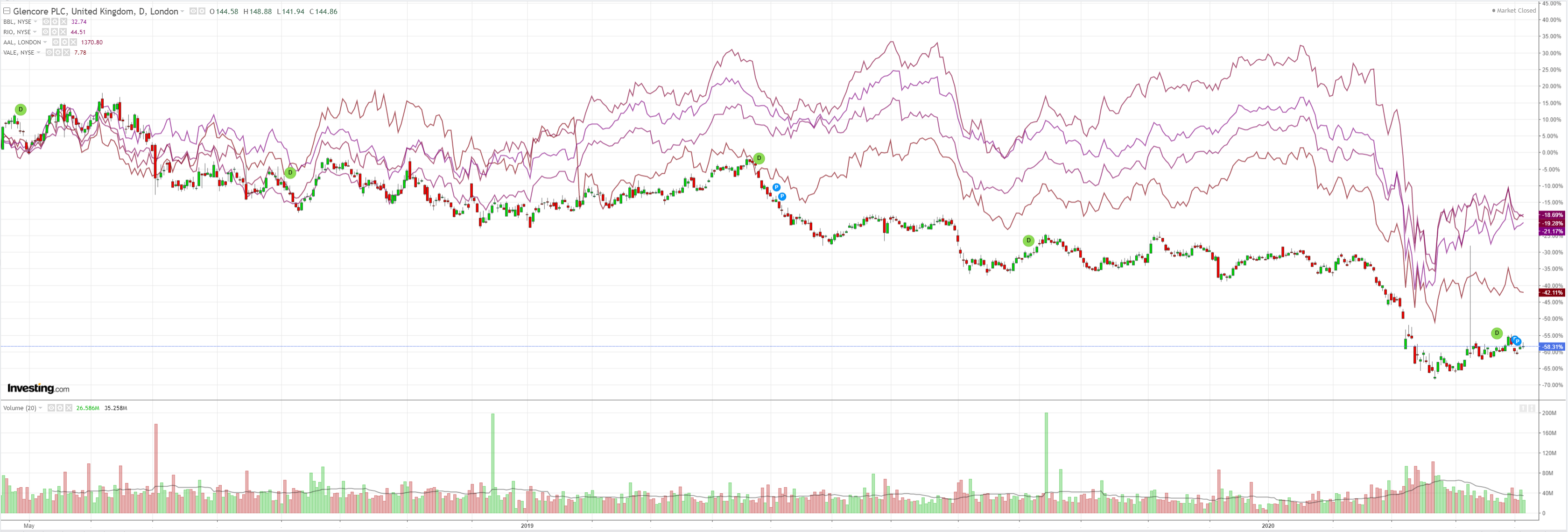

Miners were soft:

And EM stocks:

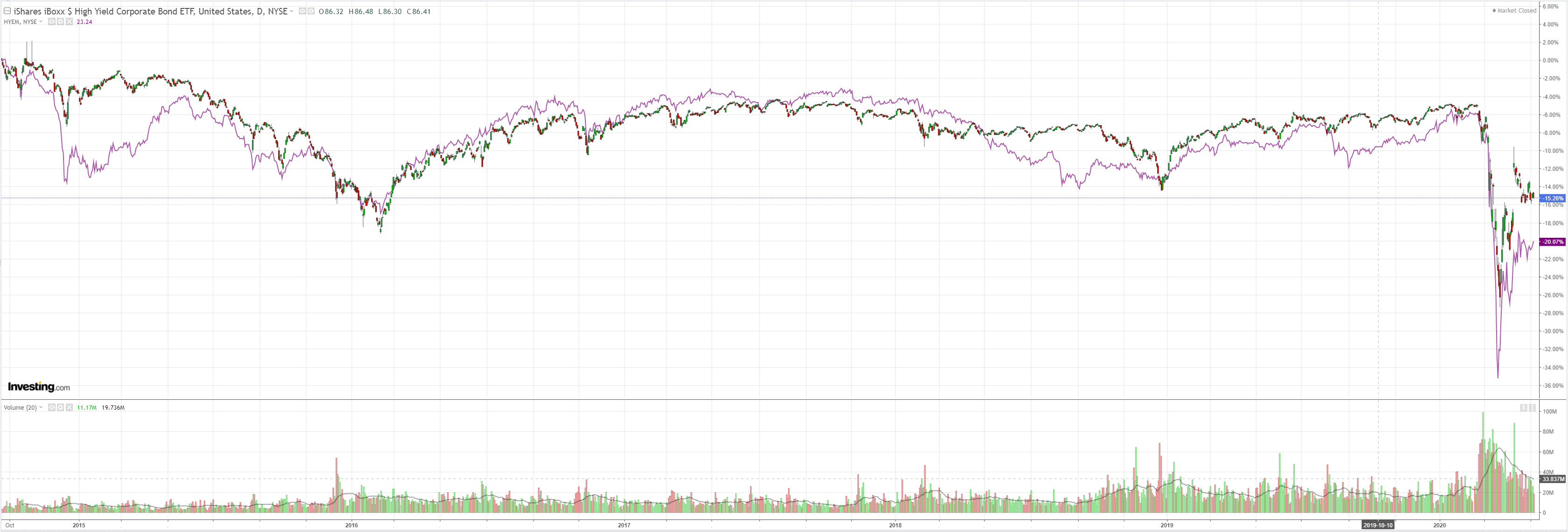

Junk held on with oil’s support:

Bonds were soft for the same reason:

Stocks fell:

Westpac has the wrap:

Event Wrap

COVID-19 update: The global case count, according to the latest data from John Hopkins University, indicates 80k new confirmed cases worldwide on 4 May, vs 76k the previous day and vs 102k at the peak on 24 April. Whereas in March daily cases accelerated, in April they have trended sideways.

The US Treasury announced its Q2 and May funding programs, increasing both to record levels, Q2 at $3tr and May at $96bn. Issuance will be skewed towards longer maturities: “Based on current fiscal forecasts, Treasury intends to increase auction sizes across all nominal coupon tenors over the May-to-July quarter. The increase in coupon issuance will be larger in longer tenors (7-year, 10-year, 20-year, and 30-year).”

The Fed’s Kaplan expected Q2 GDP to fall 25% to -30% annualized, with the unemployment rate peaking around 20%. But he also expected recovery to start in Q3, expecting it to be “very phased and very gradual”. He also confirmed the Fed will keep policy very accommodative for an extended period of time. Barkin said the mountain of debt will have to be addressed at some point, but not now.

US April ADP employment fell 20.2m (vs est. -20.6m) and is seen as a guide to Friday’s payrolls data (also est. -21m).

The EU published its Spring 2020 economic forecasts, consolidating national forecasts, and warned that the uneven impacts of COVID-19 posed risks to the stability of the region. The forecasts central profile is for Eurozone GDP to contract 7.7% in 2020 and then rebound 6.3% in 2021.

Eurozone March retail sales -11.6%m/m (est. -10.6%m/m, prior 0.6%m/m) underscored the hit to activity as the lockdowns began. Final April services PMI at 12.0 was similar to the flash reading (11.7) and again highlighted the record collapse in activity. German March factory orders slumped -15.6%m/m (est. -10%m/m), underscoring the disruption wreaked by lockdowns, with capital goods dominating the declines, -22.6%m/m.

UK April construction PMI fell even more than expected to 8.2 (est. 21.7, prior 39.5) despite parts of the sector remaining active as part of essential services.

Event Outlook

Australia: The major release of the day will be the March trade balance. Westpac is looking for the surplus to widen to $6.8bn, led by a sharp rebound in exports. The April AiG Performance of Services Index is also due, following a substantial fall of 8.3 points in March. Hospitality, the arts and retail have been hit particularly hard by the virus.

New Zealand: RBNZ inflation expectations are expected to drop sharply in the Q2 update, given the scale of the economic downturn. The Q1 read came in at 1.9%, just below the target midpoint.

China: the April Caixin composite PMI and services PMI (market f/c 50.1) will both be published. The official PMIs have indicated that conditions held up over the month. The April trade balance is expected to narrow to $8.68bn as the exports side contracts. Finally, April foreign reserves are expected to remain broadly stable at $3056.00bn after a surprise drop in March.

Germany: March industrial production is due, and the market is anticipating the largest fall on record at -7.4%.

UK: The BoE will announce its May policy decision. The policy rate is set to hold at 0.1%, but the focus will be on the Bank’s assessment of its asset purchase program.

US: Given the deterioration in the labour market, Q1 nonfarm productivity is poised for a sharp contraction of 5.5%. Following this, initial jobless claims will print, and the market is looking for yet another sizeable read of 3000k. Consumer credit is also due, and after jumping in February, a pullback to $15.0bn is expected. The FOMC’s Kashkari (2:00 am AEST) and Harker (6:00 am AEST) will discuss COVID-19.

None of that matters. What does is this:

According to Nomura’s McElligott the rally is now done, at least for the next few months, and as the Nomura strategist writes, “his sense is ‘lower’ for the next move in Spooz across the Summer months, as I think the market’s current pragmatism towards the virus in conjunction with the “feel-good” of the rally leaving it exposed to the downside of a coming second-wave as cases, as restrictions ease and some States rush back to “normalcy”…yet with fewer Fed and fiscal bullets in the chamber next time around.”

Another reason why the ramp is ending is that, as noted above, CTAs are now “somewhat distant from next triggers” and as a result “we are running out steam on the systematic vol-control-type re-leveraging at “status quo,” where in order to make the $allocation to Equities grow again significantly, we would need to see 3m realized vol (~60) fall below 1m realized (~40)—and that would require a significant “impulse” move requiring a new catalyst—so not necessarily a “sell” catalyst, but speaks to a potential “demand” vacuum.”

He then looks as the historically “weak-ish” thematic Summer seasonality for Stocks (Sell in May) and risk-sentiment (where Gold and USTs trade strong, while May thru Sep is bad for EEM and US Equities themes see Duration Sensitive Equities / Mo Longs tend to strongly outperform vs Cyclicals / Mo Shorts) matters into this current “directionless” trade

As McElligott adds, this “meh” seasonality also corresponds with this period where most of the “positive catalyst checklist” boxes made by clients in March/April in order to set scenarios to dip back-in from the long side have now largely been achieved. Of note, the ‘get constructive again’ starter kit established in March / early April is all green, so little upside left here:

What this meant then too and occurring simultaneously was a set of further positive inputs into the “vol normalization” process, following the various “short vol” stop-outs in late March—by late April we’d seen the return of Overwriters into “expensive” vols, while too we saw the resumption of an upwardly-sloping front-end of the VIX curve as an “all-clear” signal for the return of systematic “Short Vol” & VIX roll-down strategies

The drop in the VIX created mechanical covering of either legacy shorts (CTAs) or re-leveraging into longs from “vol control” / “tgt vol” space—and over the 1m stretch, and as we noted last week, we even got a day when the CTA signal had flipped back to “+100% Long,” which prompted Nomura to estimate ~$50B of CTA buying across US Eq futs on the month-long gradual / partial cover (from prior -100% position), while too our Vol Control model estimated ~ $15B bot over the past 2wks, as realized trailing vols reset gradually lower.

But now that these “positive catalysts” have largely been squeezed-out, the Nomura quant warns that “we are pivoting into said seasonality; an ugly forecast revision period for corp EPS; data continues to come-in even worse than expected as consumer psychology remains altered; the corporate cashflow disruption and imminent bankruptcy realities become front page daily news (particularly anticipating bloodshed in the energy space); and 2nd order white collar layoffs in corporate America all contribute to another sentiment swoon”

And then there is the new unknown element which is the China-US COVID / Trade War “hot potato,” where many see this rhetoric risk again growing over the Summer election cycle—and could really magnify the risks ahead of the U.S. Election, as Republican Govs look to reopen some states, while Democratic states stay slow on reopening and wait to see if another COVID wave 2.0 kicks-off…which could be seized into the election and act as a back-breaker for Republicans into Nov—either way, we have seen nothing but FXI / EEM vol buyers, with FXI Put Skew 98th %ile

This, as McElligott conlcudes, is also why it seems that “the obvious trade the market is putting-on again so far in May and ahead of the Summer is a resumption of the “Everything Duration” dynamic within Equities—long Bond Proxies (Sec Growth and Def / Min Vol) vs back again short Cyclicals / Value / High Beta as a preferred hiding-spot / comfort-blanket—as such, I’d likely prefer to express this “Momentum” view than an outright “bearish Equities” one”

This “downbeat Summer” trade would then look like a move BACK TO THE FUTURE of the “everything duration” safe-place trade, which should mean that “Momentum Long” of Secular Growers and “Cash / Assets” factor (stuff that can grow profits and earnings without a hot cycle) and Bond Proxies / Min Vol / Defensives likely continue to outperf “Momentum Shorts” being Cyclicals/ Value factor (EBITDA / EV) / Size / High Beta.

In short, the robots are done. Combine that with a developing new narrative to displace the “v-shaped recovery”, returning trade war, via Reuters:

US President Donald Trump said on Wednesday he would be able to report in about a week or two on whether China is fulfilling its obligations under a Phase-1 trade deal the two countries signed in January.

Speaking at a White House event, Trump told reporters China may or may not keep the trade deal.

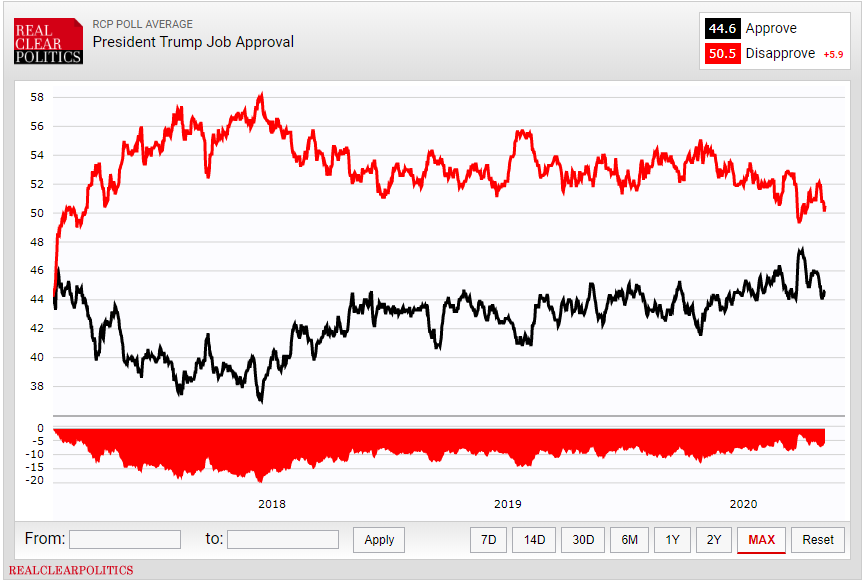

China has no chance of fulfilling its side of the deal. But that does not matter. The key chart is this one:

Trump’s appalling mismanagement of the virus means blame must be deflected to China if his polling falls.

Given his historic failure, that’s an odds-on bet.

Even if the virus war remains largely rhetorical, the base case is swinging swiftly towards it getting worse not better over the next six months putting stocks and the Australian dollar squarely in the gun.