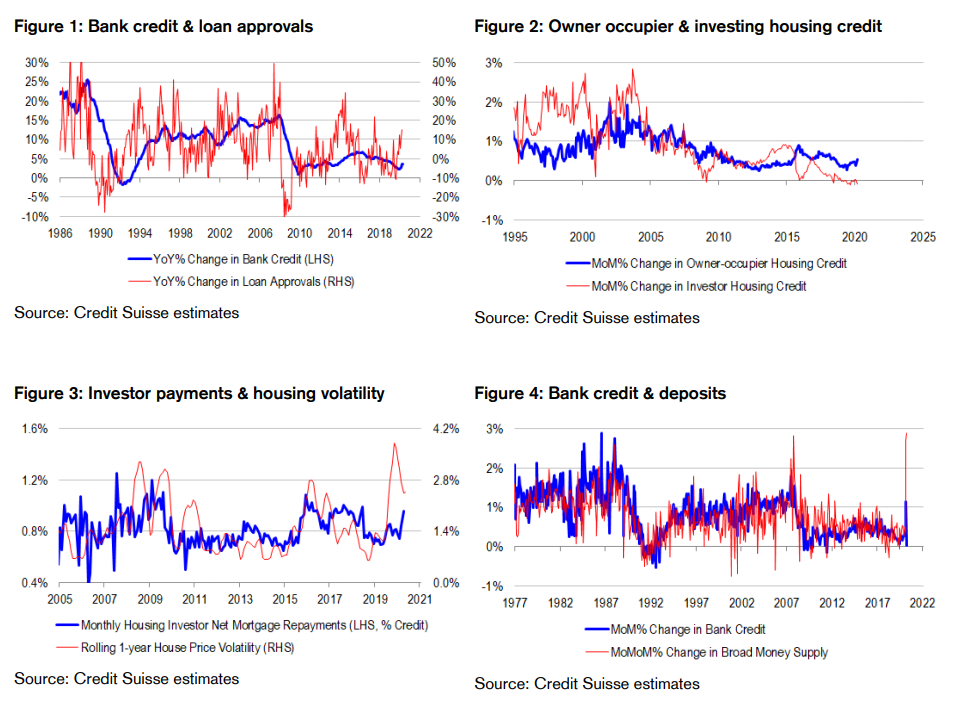

Credit growth surprises materially to the downside. Bank credit was unchanged in April, compared with the Consensus forecast for 0.6% monthly growth. Year-ended growth slowed to 3.6% from an upwardly revised 3.7%, versus expectations for a pick up to 4% . Compositionally, business and housing credit rose moderately, while personal credit fell. Arguably the major source of downside surprise was in the business lending category, with firms not drawing down more heavily on their credit lines which economists expected. But we think that there was an interesting story to tell with regards to debt repayment as well.

Housing investor de-leveraging continues to negate owner-occupier debt holidays. Although housing credit grew moderately in April, there were divergent trends between owner-occupiers and investors. Like we saw in March, investor credit declined, while owner-occupier credit rose. Investor credit has been declining because borrowers have become much more uncertain about prospects for house price inflation amid lower migration and heavy supply. They have also had to worry about non-payment of rents during the shutdown phase. Therefore, they have chosen to de-risk and de-lever on their biggest overweight exposure in housing, having being wrong footed on their risk assumptions. Investor mortgage principal payments have risen accordingly. In contrast, owner-occupiers have benefited from debt repayment holidays granted by the banks, and their reduction of principal repayments has inflated the stock of credit.

Strong money supply growth, but arguably not strong enough. Broad money supply is the broadest definition of bank deposits. In theory, deposits are created by bank lending and fiscal deficits. Also, in Australia, there is the classification issue of cash held in superannuation accounts not being counted in the official measures of bank deposits. With all of this in mind, it is an interesting exercise to dissect the strong growth in broad money supply in April of 2.9% in sequential rate of change terms, and $60 billion in dollar terms. Clearly, bank loan growth did not contribute to deposit growth in April. But fiscal deficits should have added $24 billion. And arguably, emergency superannuation withdrawals eclipsing $13 billion, could have materially increased measured deposits to the extent that there was spare cash in these accounts to withdraw, or to the extent that proceeds that were not obtained by super funds selling assets to another member of the general public. In principle, conventional RBA quantitative easing (QE) should not have had a major impact on measured deposits, as the program should have been conducted as an asset swap with the banks, rather than with the general public. However, the Bank has officially been buying bonds from non-banks as well, and so QE has probably has increased deposits in the system. Indeed, in April, the RBA purchased $25 billion of government bonds. Also, the AOFM has been conducting purchases of private securities of non-bank lenders to support small business lending, and in April, $190 billion of transactions were settled. Marrying up the data, we find that broad money supply growth in April cannot easily be explained by the sum of bank loan growth, fiscal deficit spending, emergency superannuation withdrawals, RBA QE and AOFM lending. If anything, money supply growth should have been even stronger than recorded. This leads us to suspect that some of the money injected or freed up by policy makers has been used by the private sector for debt repayment purposes, as principal repayments destroys deposits – the flipside of new loans creating them.

Either worry about deteriorating borrower equity or de-leveraging. We find it quite concerning that non-repayment of debt is currently seen as the primary way of inflating the stock of credit. Indeed, with property prices falling, non-repayment of debt leads to incredibly sharp deterioration of the equity base of borrowers on a mark-to-market basis. After all, every 1% decline in house prices represents a 2% decline in the average equity base of mortgagees because of leverage. But an even bigger concern is that despite the attempts to reflate the credit stock through non-repayment of debts, the economy is struggling to do so! Investors are reacting rationally to high uncertainty by de-risking and de-leveraging on their housing exposures, counteracting policy maker attempts to drive repayments lower. To be sure, if the economy fully re-opens, and population growth accelerates, perhaps there is not too much to worry about longer-term, everyone can cross the “bridge” that policy makers have tried to build, and life can get back to normal for housing investors. But the reality is that a full re-opening of the borders is not on the table yet, because it is the riskiest decision that policy makers need to make in light of a possible second wave of COVID-19.

RBA right to lobby for fiscal stimulus extension. In his late May testimony to Parliament, RBA Governor Lowe recognized that the economy has been performing better than feared, and applauded fiscal policy makers for their responsiveness to the crisis. But he also tried to persuade them to taper or extend programs like Job Keeper, while reminding them that at the zero bound, the burden of counter-cyclical easing falls more on them than the Bank (hence the reticence to entertain negative rates). With housing uncertainty high, and de-leveraging pressures lurking beneath the surface, the risks are that by September, when fiscal stimulus formally runs out, that the economy’s credit impulse will be quite weak, and in need of a boost. For what it is worth, we think that Lowe’s view and advice are correct.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.