The bank believes we are heading for a severe downturn in commercial property valuations, which will trigger a sharp rise in loan losses in Westpac’s business and institutional banking divisions.

…Chanticleer understands the economic forecast underpinning the $1.6 billion impairment includes a spike in mortgage defaults along with a 10 per cent to 15 per cent decline in residential property prices.

…But it is the commercial property weakness that will worry the prudential regulator and investors because the loan numbers are so large.

The conclusion is that Westpac will not need capital.

Good luck with that.

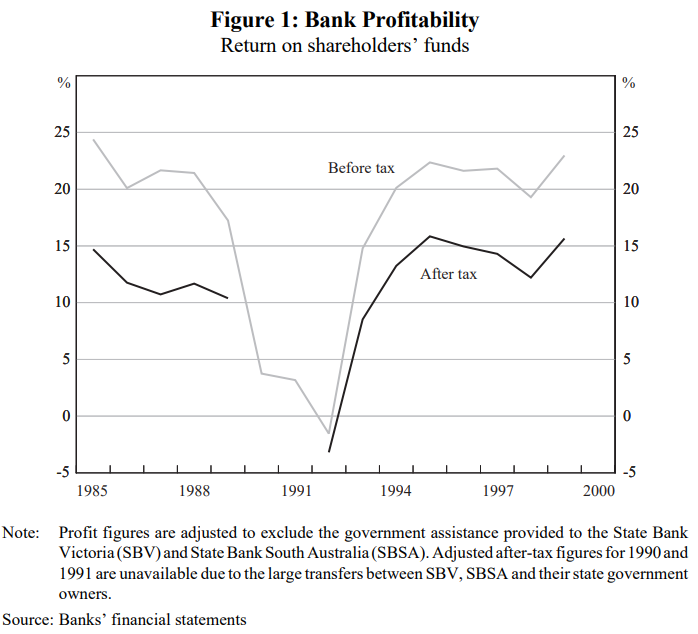

The RBA has a glossy memory of the last time Westpac faced this kind of shock:

The largest losses were recorded by the State Bank of Victoria (SBV) and the State Bank of South Australia (SBSA). Both banks were owned by state governments and experienced pre-tax losses exceeding three times the 1989 level of shareholders’ funds. Large losses were also recorded by Westpac and ANZ (two of the four major banks) in 1992, following comprehensive market-based revaluations of their property assets; in Westpac’s case this process led to a reduction of almost 40 per cent in the value of its property assets and collateral. While the losses by these two banks were large, they were easily absorbed by the banks’ capital.

Advertisement

Easily absorbed, eh. Doesn’t anyone remember failed rights issues and Kerry Packer. From the Canberra Times in late 1992:

Kerry Packer, Australia’s wealthiest businessman, has staged a daring share-market raid to pick up more than 8 per cent of Westpac, Australia’s largest bank.

A string of disasters has left Westpac vulnerable to a’share raider and even a possible takeover.

Westpac’s problem loans exploded to $9.26 billion. It was forced into massive property writedowns.

The failure of a $ 1.2 billion rights issue which only 27 per cent of shareholders took up, left underwriters with the remaining shares and culminated in the resignation of the company’s chairman, Sir Eric Neal, and three other board members.

The company’s share price was more than halved from more than $5.50 in early 1990 to $2.51 in early November.

It closed at $2.99 yesterday, its highest price since the failed rights issue closed in September. Strong buying, mainly by Mr Packer, has pushed the share price up 26c this week.

Mr Packer’s 8.27 per cent stake in the company has so, far cost him about $230 million, a remarkably small outlay to give him 8.27 per cent — and considerable influence — over Australia’s largest bank, with assets of $ 110.9 billion and Australia’s seventh largest company with a market capitalisation of$5.342 billion.

Although Mr Packer is limited by the Banking Act to a maximum 10 per cent in Westpac, by working with Westpac’s largest shareholder, the AMP Society, which holds 15 per cent, Mr Packer is likely to put the bank’s management under strong pressure to improve its performance.

It will be amusing if a Chinese tycoon comes calling this time.

Advertisement

This will be a bigger recession than 1991 and the property writedowns will again be huge again. Importantly, there is a structural change in this shock, both for lower office and retail occupation plus lower immigration hitting residential. Values will shunt lower permanently.

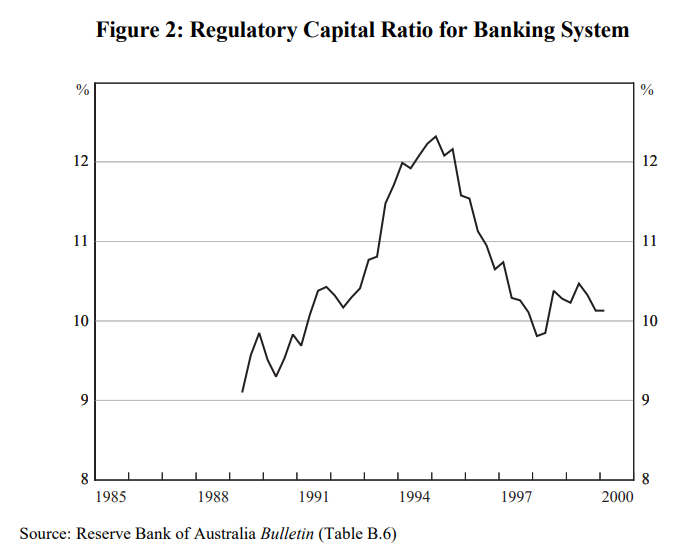

We’ve got more public support for banks these days but the entire country is massively more leveraged as well. Capital ratios were calculated differently but they were roughly the same level as today:

Advertisement

And note that the close shave led to much higher capital, weighing on shareholder returns for years.

If WBC can sail through this shock without raising capital then I will eat my hat.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.