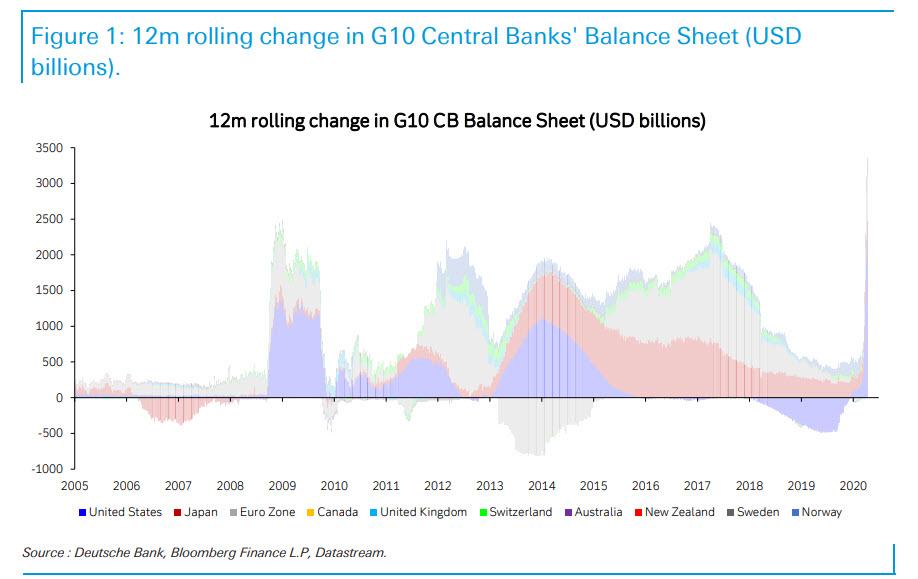

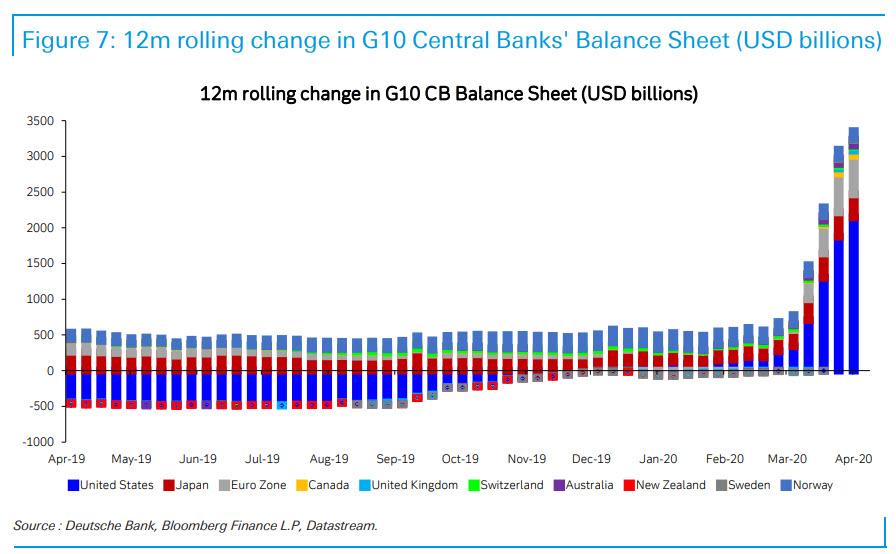

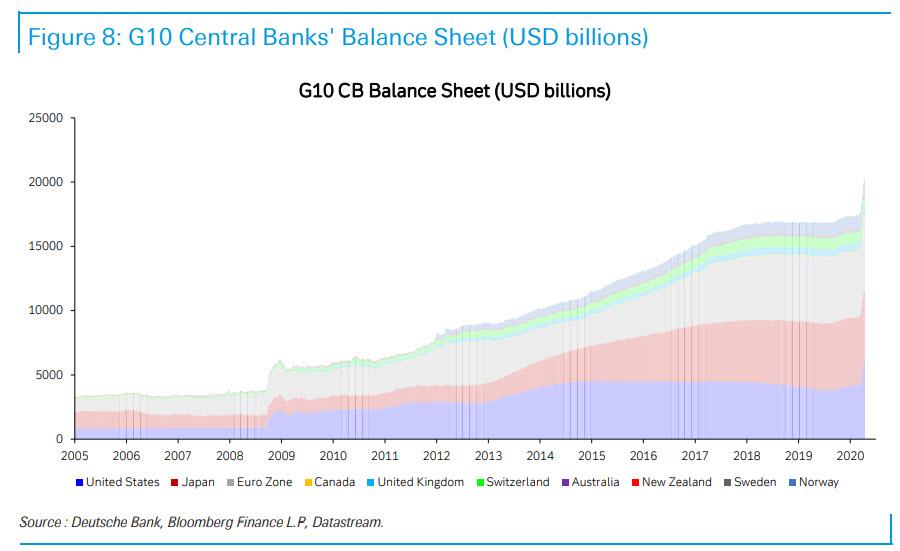

By almost any metric Central bank balance sheet expansion in the last few weeks has already exceeded anything seen in the 2008/9 crisis period. In the last six weeks alone, G10 Central banks have expanded their collective balance sheet by $2.7 trillion, and 2/3rds of this comes from the Fed.

The Fed has stepped up into a role sometimes seen by China, in its credit policies, and sheer scale of support.

The steep ascent of Central Bank balance sheets has of course been more than matched by the collapse in the global economy. Unprecedented QE policy accommodation will then build substantially from here, which warrants asking all the usual questions about what this might reap? The answers unfortunately belie simplicity. QE delivers very different results depending on circumstance, but in general, the marginal risk appetite gains from QE will wane with time.

The Fed appears to be working under the premise that in past crises of historic proportion, there are almost no occasions when the monetary authorities are remembered and accused of doing too much. So why not load the bazooka with the kitchen sink and go nuclear?

Theoretical models typically would see large scale QE as negative for a currency, but in this instance, the initial positive QE impact on risk (helping EM and commodity currencies) but also seen as an alternative to negative rates, is a mixed bag for the USD, enough to leave the USD choppy at elevated levels.

The experience during and after the 2008 crisis, is that markets are apt to initially support a major currency backed by an aggressive Central bank, especially when the economic morass that provoked the easing is universal. There is currently a brief window for many Central Banks to pursue QE, including EM Central Banks precisely because everyone else is doing it.

If persistent QE looks like the Central Bank is out of ideas, and, especially where the actions are enacted by a Central bank in isolation, QE will be greeted with a weaker currency. The EUR and JPY have periodically suffered this fate, and Japanization will become a more widespread phenomena in this downturn.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.