Warwick Smith, research economist at the University of Melbourne, has penned a scathing attack on Australia’s compulsory superannuation system, labeling it a “ponzi scheme” that is helping to drive “speculative bubbles”:

If our goal is an adequate and sustainable income in retirement for all Australians, our main priority ought to be ensuring that those remaining in the workforce are productive enough to support themselves, their children, those without work and those who have retired.

In other words, if you’re worried about the economic impact of our ageing population on our material standard of living (and there are reasons not to be worried) you would want our focus to be on productivity, rather than retirement savings.

To the extent retirement savings are used for productivity enhancing investment, that’s good. The reality is much of our retirement savings are funnelled relatively unthinkingly into an already bloated financial system where they expand speculative bubbles.

Elsewhere I’ve referred to it as Australia’s first compulsory Ponzi scheme…

The best way [to improve the retirement system] would be to get rid of compulsory superannuation, give all the money back to account holders (slowly to avoid too much inflation), mandate a 9.5% pay rise in its place and redirect the tens of billions of dollars we currently spend on superannuation tax concessions toward rent assistance, a higher Newstart allowance and a higher pension.

Smith’s ponzi scheme claim is an interesting one. Effectively he is arguing that mandating Australians to direct 9.5% of their wages into financial markets necessarily inflates stock and bond prices which, because prices are rising, then encourages more people to pile in, creating asset bubbles.

However, with the large baby boomer cohort entering requirement age, and needing to draw down on their savings, this risks deflating asset prices and creating a situation whereby the level of one’s retirement income is dependent on whether they withdraw their savings while the “bubble” is still inflated.

The obvious short-term solution to this dilemma is to increase mandatory contributions into superannuation from 9.5% of wages currently to the legislated 12%. This will ensure that the net inflows into superannuation continues to rise as more baby boomers retire, thereby keeping the bubble inflated (at least until generations X and Y retire).

While there are certainly ponzi elements to Australia’s superannuation system, there are far bigger problems that preclude it from being a genuine retirement pillar.

First, superannuation is voluntary for the self-employed. Thereby it misses some 2 million Australian workers.

Second, superannuation can be withdrawn in full and spent from 60 years of age – many years before the official retirement age of 66 (rising to 67).

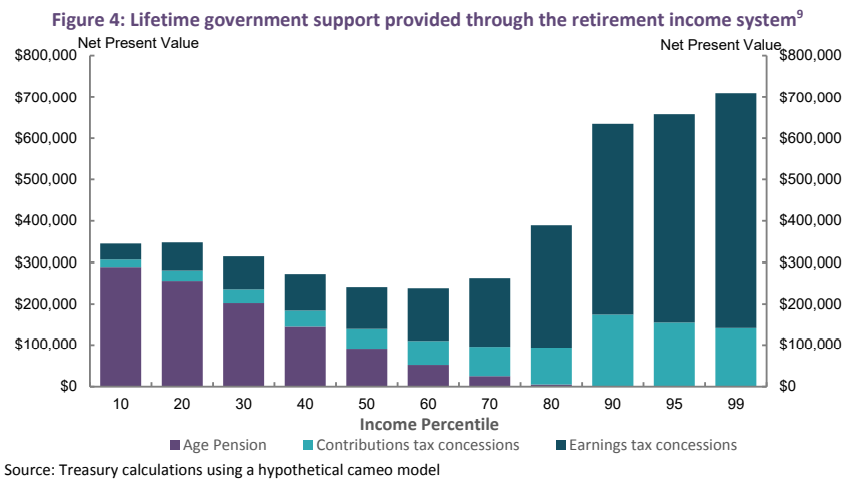

Third, the lion’s share of superannuation concessions flow to those that do not need them, namely higher income earners. This means that superannuation costs the federal government far more than it saves in Aged Pension costs. Moreover, how much superannuation one saves is dependent on long one works and how much they earn, which obviously favours high income earners.

Accordingly, Australian Treasury research shows that the top 1% of income earners will receive more than $700,000 in taxpayer assistance over their working lives. This far exceeds the $50,000 of taxpayer assistance received by the bottom 10% of income earners (see next chart).

Fourth, superannuation nest eggs are exposed to market risks, which means that balances can be wiped out via a stockmarket crash, as we have experienced recently (as well as during the Global Financial Crisis).

Now compare the superannuation system to the Aged Pension, which does not suffer from the above pitfalls and should be considered Australia’s genuine retirement pillar.

The Aged Pension is available universally as soon as one reaches retirement age, provided they are not already wealthy. Since it is means tested, it is targeted towards those that need it most, rather than the wealthy. It is not based on how long one works or how much they earned during their working lives. And it is not subject to market risk.

Given these facts, taxpayer resources should move away from supporting superannuation towards boosting the Aged Pension, which is Australia’s genuine retirement pillar.