Should we trust Chris Joye’s Flying Circus?

Chris Joye had a very busy Friday. To begin with, he co-ordinated the rebuttal petition to Australia’s best-in-class economist’s open letter arguing we should not rush the reopening of the economy:

Summary: Australia’s outstanding success cauterising the spread of COVID-19 has placed us in a position to seek to promptly reactivate the economy. If the current lockdown is allowed to continue as some academics propose, millions of Australians will suffer from dire economic and human costs, including prolonged unemployment, rising suicide rates, homelessness, domestic violence, drug and alcohol abuse, and abject poverty. A measured exit from the current containment strategy will spark a recovery in employment, incomes and growth, and minimise the financial and health costs from what could otherwise be a 1-in-100 year depression.

Such a bold call deserves to be taken seriously so let’s assess it. Those signing on included:

- Everald Compton, Adjunct, Professor, Faculty of Health and Social Sciences, University of Queensland

- Adam Creighton, Economics Editor, The Australian

- Will Hamilton, CEO, Hamilton Wealth Partners

- Kieran Hennessy, CEO Seattle Group

- Nick Hossack, Principal, Benchmark Analytics, former adviser to Prime Minister Howard

- Christopher Joye, CEO, Coolabah Capital Investments

- Stephen Koukoulas, CEO, Market Economics, former adviser to Prime Minister Gillard

- Ian Macoun, CEO Pinnacle Investment Management, inaugural CEO of QIC

- Harry Moffitt, CEO & Psychologist, Stotan Group

- Terry McCrann, Business Columnist, Herald Sun & The Australian

- Andrew Mohl, Former CEO, AMP and Non Executive Director, CBA

- Campbell Newman AO, Chairman of Arcana Capital and Former Premier of Queensland

- Anthony Roberts, Managing Director, Porter Davis

- John Stone, former Treasury Secretary and Senator for Queensland

- Ramesh Thakur, Emeritus Professor, Crawford School of Public Policy, The Australian National Uni

As noted on Friday, this is a grab bag of economic marginals versus the blue-chip 134 professors and lecturers on the original petition.

I do not wish to make a false appeal to authority, but that credibility gap does count for something.

Measuring how large is the gap is not easy given we don’t know the individuals very well and only a few have participated in public discussion. We can observe that Joye’s Flying Circus has a preponderance of Murdoch commentators, notorious fiscal hard-nuts, and investors.

The first we should probably disregard given the known biases within News Corporation.

The second, we know their positions on everything well in advance.

The third, we have to wonder about their motives. Are they front-running an early opening in their portfolios? A question I will return to. (And yes, I am aware that we could also be accused of this but our positions are all very much on the record).

We can, at least, add some texture to those that have argued in the public sphere. The leading two on that front are Chris Joye himself and Stephen Koukoulas.

We had the fortune of interviewing Mr Joye on February 20, when we were already deep into the health crisis. He said:

“I don’t have a strong view on coronavirus. I was at a conference yesterday and I heard people argue very strongly that this was the butterfly effect that would effectively trigger the next major global meltdown and then I heard a lot of folks were fading corona. The market’s been fading corona. We’re very respectful of market pricing. On the other hand, markets make mistakes.”

A fair enough view but not exactly right in retrospect. He started to make more sense a week later and, along with MB, drove the monetary debate forward.

Joye subsequently added some COVID-19 curve models to the public sphere and argued conclusively when the pandemic would peak, ignoring the risk that his parameters may be wrong. And ignoring that even small changes in parameters make a huge difference in outcomes. It’s still too early to know either way.

So, Mr Joye was initially slow to react to COVID-19, added some good policy suggests mid-crisis, but has since drawn aggressive conclusions from limited, uncertain data sources.

Turning to Stephen Koukoulas, we shift from mercurial to humbling. I have already been forced on two occasions to blog Mr Koukoulas’ chaotic take on COVID-19 from the outset:

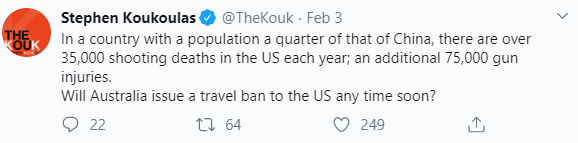

Early on, Mr Koukoulas blasted the decision to implement a travel ban on China:

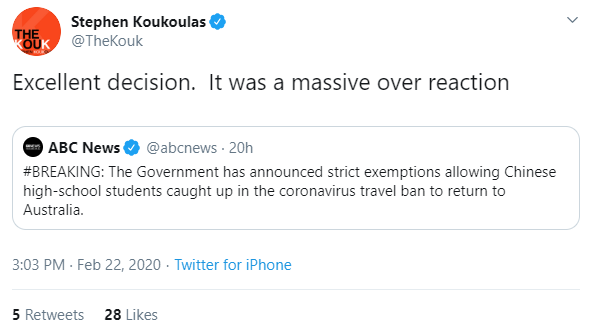

He then called for the travel ban to be lifted on the eve of global disaster:

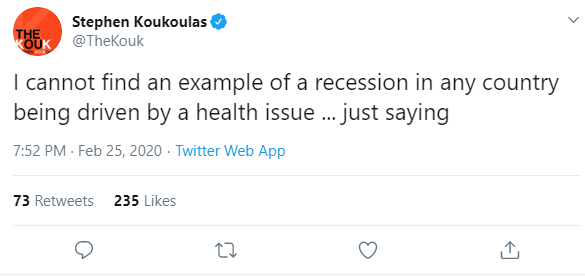

He also played down the economic impacts:

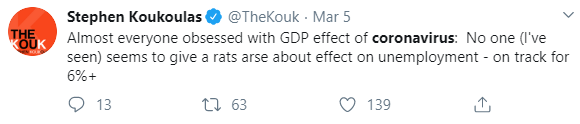

Next, Mr Koukoulas slammed into reverse gear, warning of widespread economic damage from the virus and demanding massive stimulus:

Next, he attacked those that did call it right:

Oh no:

We are seeing an array of Steve Keen wannabes starting to emerge saying “I called the crash”.

Amazing that they were more prescient than every medical professional in the world.— Stephen Koukoulas (@TheKouk) March 25, 2020

Mr Koukoulas has since oscillated, almost minute-by-minute, between attacking the Government for taking on too much debt, and demanding more stimulus. If he had signed both competing economist’s petitions it would not have surprised anyone.

I think you will agree that anything Mr Koukoulas touches with respect to COVID-19 should be discounted.

So, not discounting the possibility that behind the Joye’s Flying Circus is a secretariat of all-powerful research, that’s not much of a proven intellectual basis to demand something so dramatic as an immediate reopening of the economy. And this is where I wonder if anyone on Chris Joye’s list of prognosticators has given the due time, research, and thought to a decision of such gravity.

For instance, one would have thought that such a heady group of investors would recognise an asymmetric bet when they see one. By that, I mean that the upside to opening the economy early is minimal while the potential downside is catastrophic.

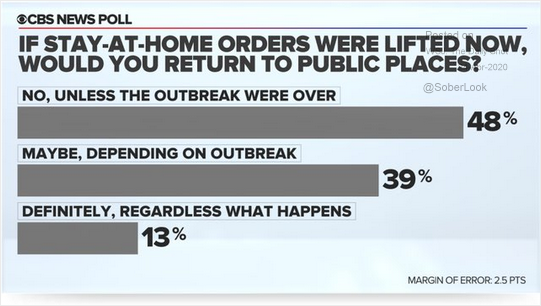

If we reopen early then we will see some renewed economic activity, certainly, and some reduction in the fiscal deficits versus if we stay closed. But it won’t be a great deal on either count given the earlier we open the less likely everybody will be to trust it. There is, here, an analogy with Ricardian equivalence in that the less government does, then the more the private sector will do. A recent CBS survey of Americans supported this view (notwithstanding their different experience of the virus):

As well, the local fiscal stimulus is good enough that activity will be supported anyway. As many an economist has already declared, JobKeeper alone has reduced peak unemployment from 15% to 10%. And more can be done. Much more. With the RBA controlling the yield curve, the stimulus options are limitless.

Conversely, the downside to an early opening gone wrong is extreme. If we trigger another breakout of the virus it would necessitate another, even more severe, lockdown. Much like what has happened in Singapore. This is particularly true given the virus is more dangerous and difficult to contain in Winter.

That outcome would result in the total collapse of faith in authorities to manage the crisis, delivering a much deeper structural blow to confidence across the economy, for a much longer period.

We need to ask whether Chris Joye’s Flying Circus has done the detailed research about re-opening economies that are on display in Tomas Peuyo’s work? It’s no easy matter and will take time to get the comprehensive infrastructure in place.

Or, has the Flying Circus given much thought to the scenario of eliminating the virus altogether. There is credible medical research arguing that in as little as seven weeks of shut down we will achieve it:

This is a real possibility that would position the economy as a fortress that could reopen with complete confidence to operate at full domestic capacity.

Indeed, recent MIT research showed harsher lockdowns during the Spanish flu of 1918/19 led to much stronger economic recoveries.

Let’s close with another Chris Joye Flying Circus moment from Friday afternoon that may help cast light upon his haste. At the AFR he wrote:

So I will repeat what I have publicly and privately advised the many folks who have inquired about my forecast for the $7 trillion-plus residential real estate market: home values are unlikely to fall materially and, in my central case, will either move sideways or at most fall by up to 5 per cent over the next three to six months, after which the robust cyclical boom will resume.

…According to the world’s most advanced daily house price index, produced by CoreLogic, Sydney and Brisbane prices continued climbing through March and April. In Sydney we are just starting to see some evidence of flat-lining. Melbourne prices have moved sideways since mid-March, but show no signs of any striking deterioration.

Given Mr Joye helped create the CoreLogic index during his time at Rismark, which was subsequently acquired by RPData now CoreLogic, this is a curious example of intellectual onanism in which one quotes oneself while fantasising that it is somebody else.

Does this imply that Mr Joye needs house prices to rise pronto? Is his portfolio of debt securities, such as bank hybrids, front-running it?

I don’t know.

In the context of a question of national life and death, Chris Joye’s Flying Circus should make it clear, as well as answering every other question posed.