COVID-19 update: The global case count continues to roll over, with latest data from John Hopkins University indicating 69k new confirmed cases worldwide on 27 April, vs 75k the previous day and vs 102k at the peak on 24 April.

US Confidence Board’s April consumer confidence survey was in line with weak expectations at 86.9 (est. 87.0, prior revised to 118.2 from 120.0), led down by a deep slump in the current situation to 76.4 (prior 166.7), although expectations rose from 86.8 in March to 93.8. Richmond Fed April manufacturing survey fell to -53 (a record low and vs. est. -43) from the prior month’s 2. New orders collapsed to -61 from zero, and shipments fell to -70 from +13. Inventories rose (to 30 from 14) as shipments collapsed. US March trade balance fell to -USD64.2bn (est. -55.0bn) as exports declined (-6.7%m/m) more rapidly than imports (-2.4%m/m). March wholesaleinventories showed a deeper wholesale draw (-1.0%m/m, est. -0.4%m/m) but retail inventories rose +0.9%m/m (est. +0.5%m/m). S&P/CoreLogic/Case Shiller Feb. house prices (pre-COVID impacts) rose +4.16%y/y, vs. est. +4.10%.

Event Outlook

Australia: Westpac forecasts headline Q1 CPIinflation to print at 0.1%qtr, 1.9%yr, with falls in holiday travel (impacted by the bushfires and virus disruptions) and petrol prices. The Q1 trimmed mean CPI is forecast to be a subdued 0.3%qtr, 1.6%yr. This is consistent with weak wages growth, patchy consumer spending and softness in housing inflation.

New Zealand: Westpac expects that the March trade balance will print at $670m. This widening is largely driven by the exports side, which was resilient despite the lockdown in China.

Euro Area: April EC economic confidence is expected to pull back sharply to 74.0; PMIs have already highlighted the dark shadow over economic conditions.

US: Westpac expects that Q1 GDP contracted by -2.5%yr annualised (market f/c -3.8%yr). March pending home sales are likely to have seized up amid lockdown restrictions (market f/c -13.6%). The FOMC will announce its April policy rate decision; with the fed funds rate midpoint at the effective lower bound of 0.125%, no change is anticipated. Chair Powell will then hold the post-FOMC meeting press conference at 4:30 am AEST.

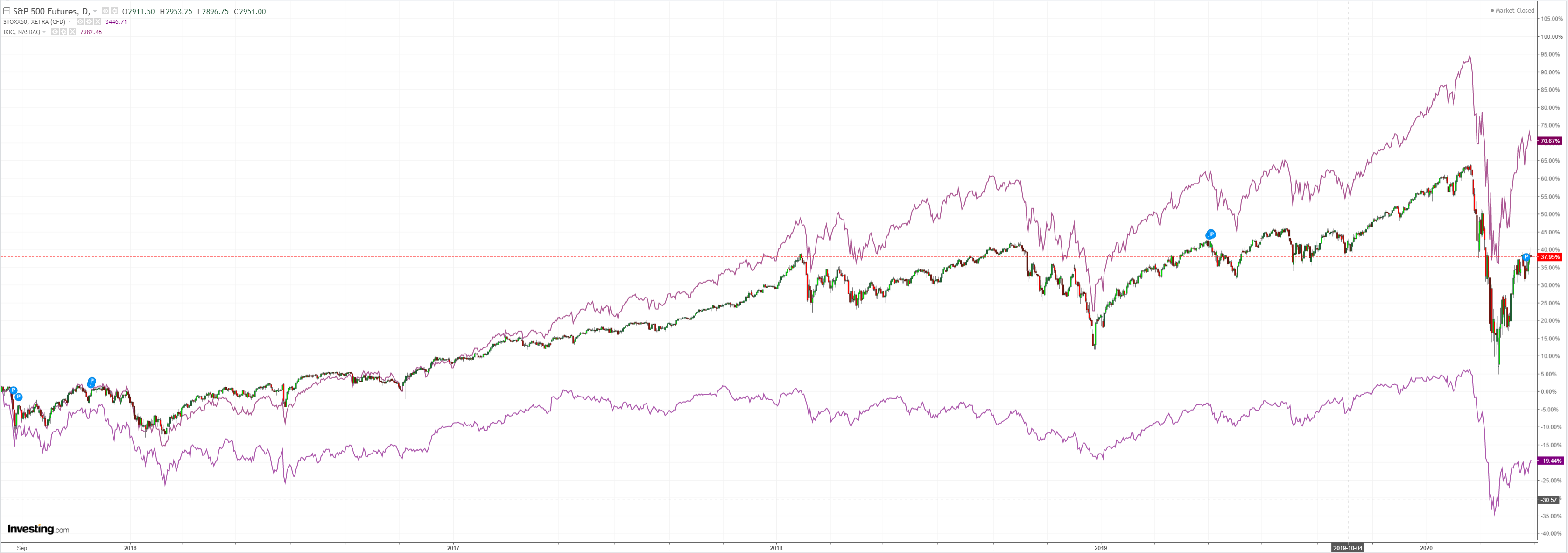

Data is still universally disastrous and irrelevant. What matters right now is momentum only which puts us firmly in the realm of the robots, via Nomura:

Advertisement

…the buying of equities we are seeing has a strongly technical flavor, as it is apparently being led by trend-following algos (CTAs, risk-parity funds), including by way of short-covering.

…risk-parity funds appear to have slightly upped their allocations to DM equities and EM equities in the context of their month-end rebalancing, and have been buying equities accordingly.

…what we are seeing is arguably a classic bear market rally.

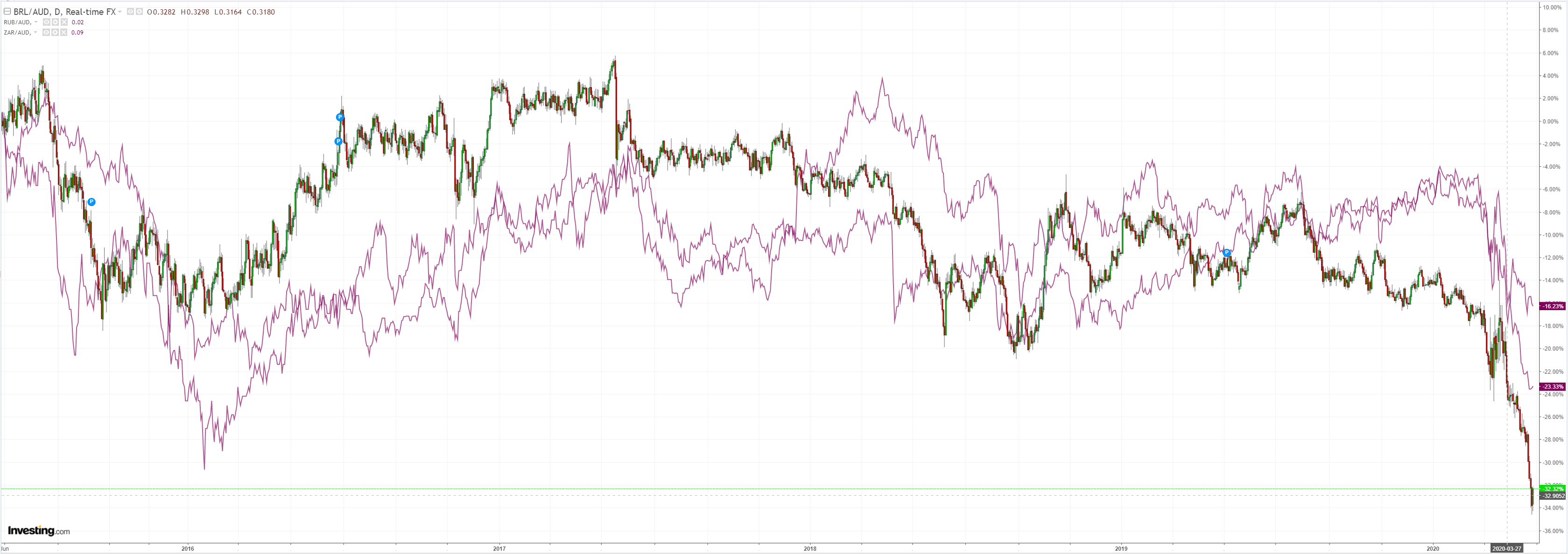

I posit that the same applies to the Australian dollar. It will top out when the market begins caring about data again.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.