DXY is still strong:

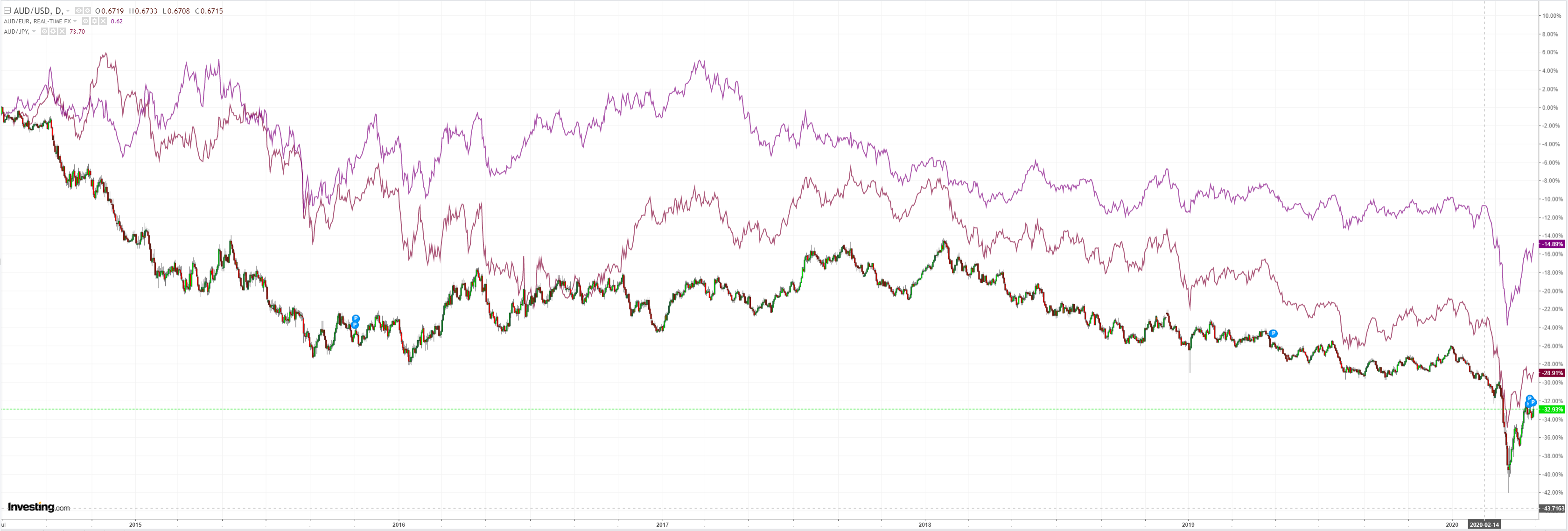

But not as strong as the Australian dollar:

Gold looks strong too:

Oil paused but it’s not over:

Dirt was mixed:

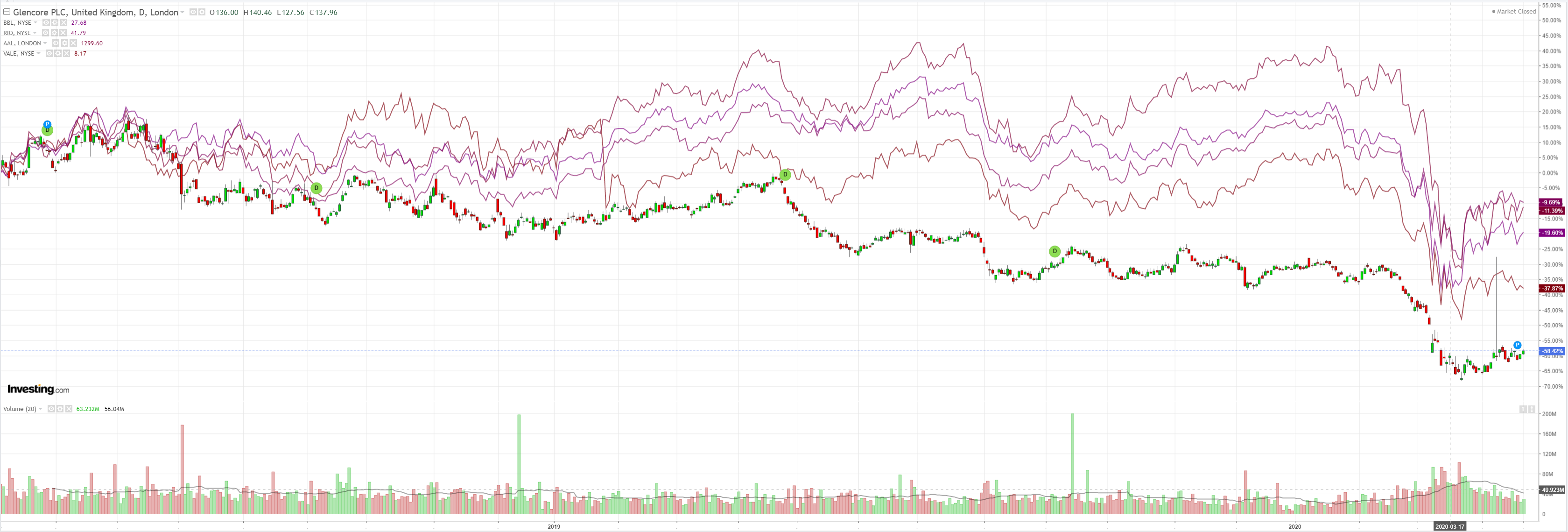

Miners too:

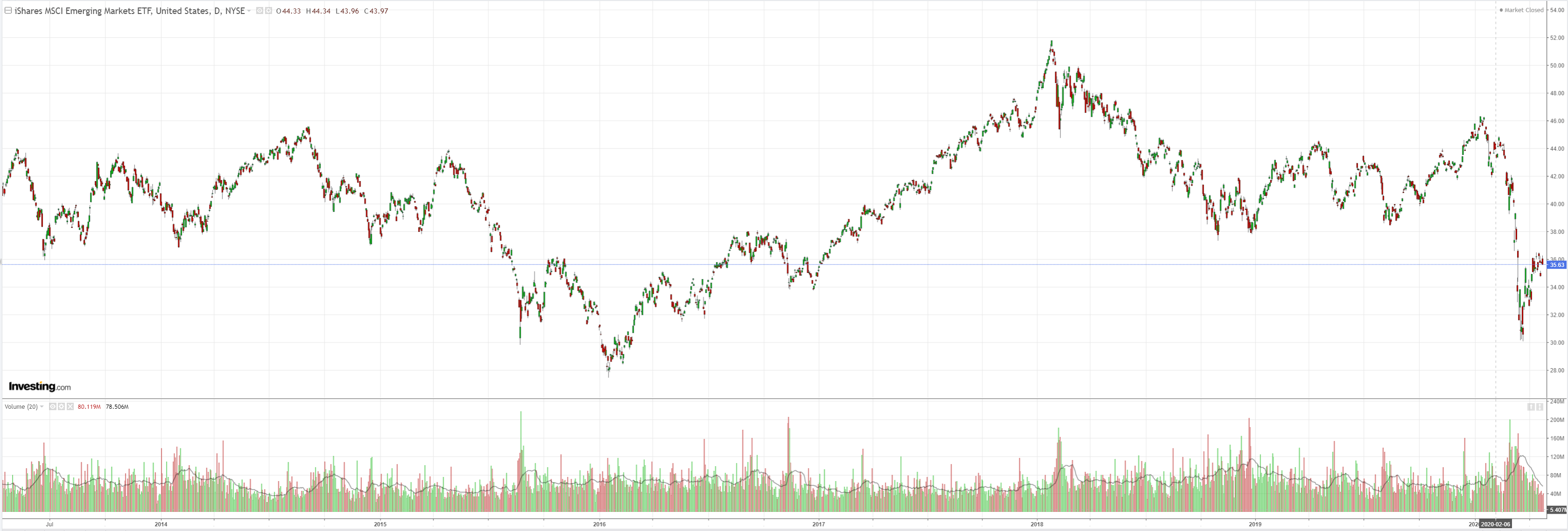

EM stocks are stuck:

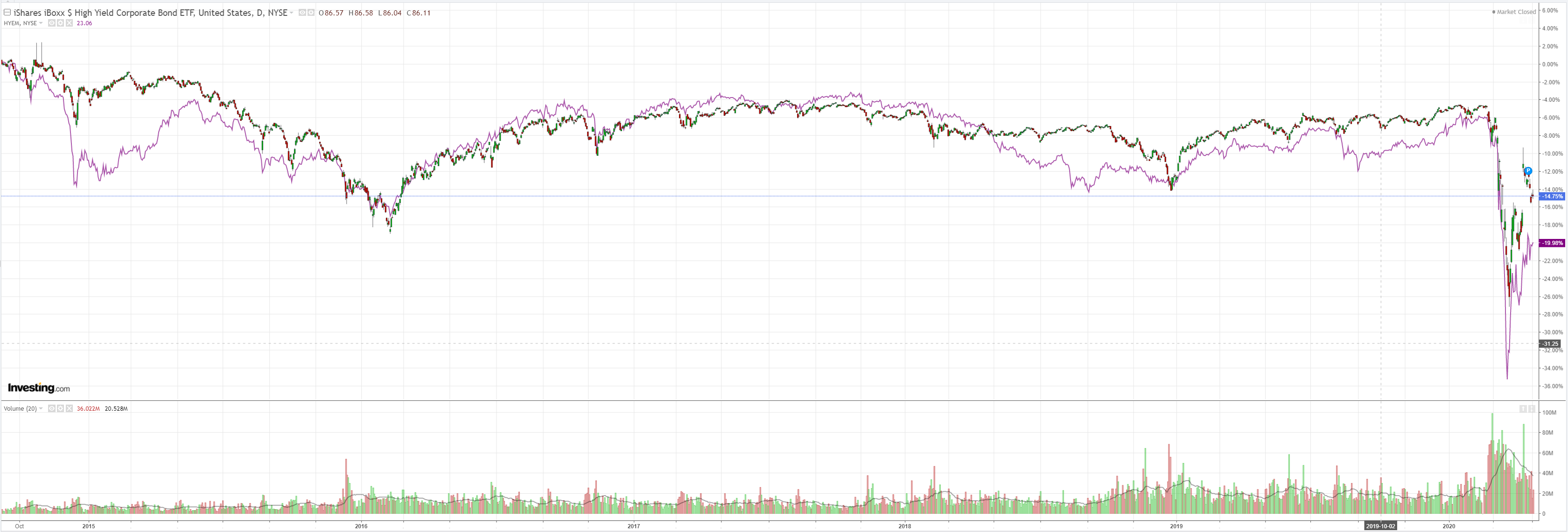

Junk is still fine:

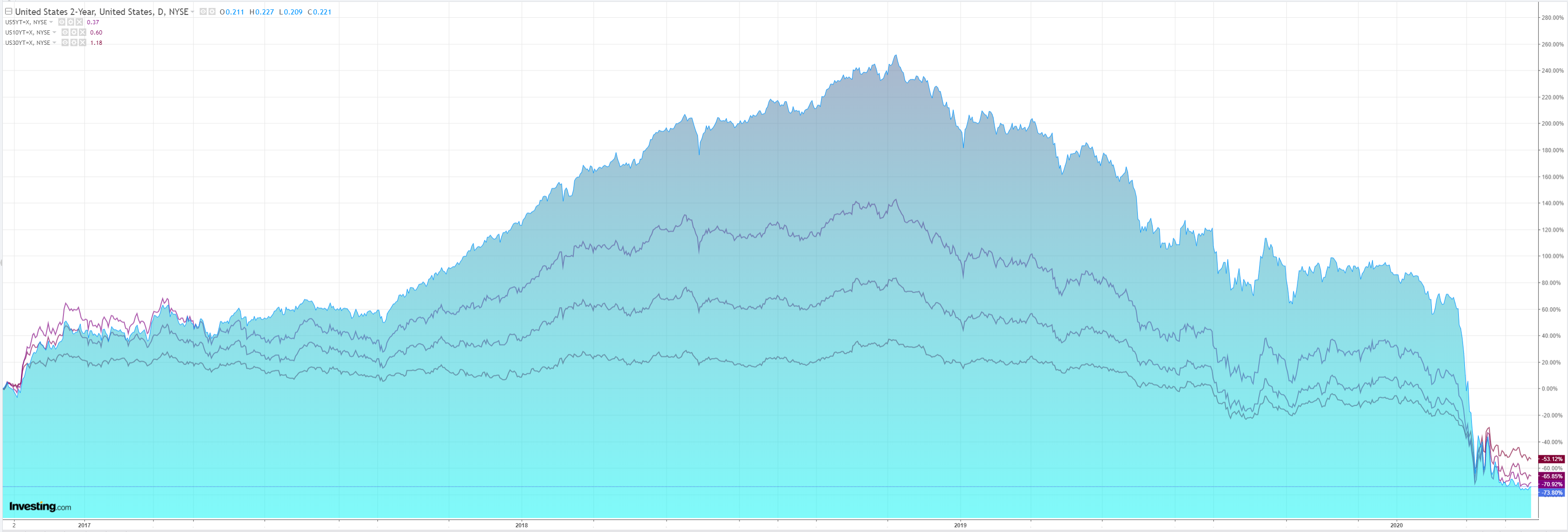

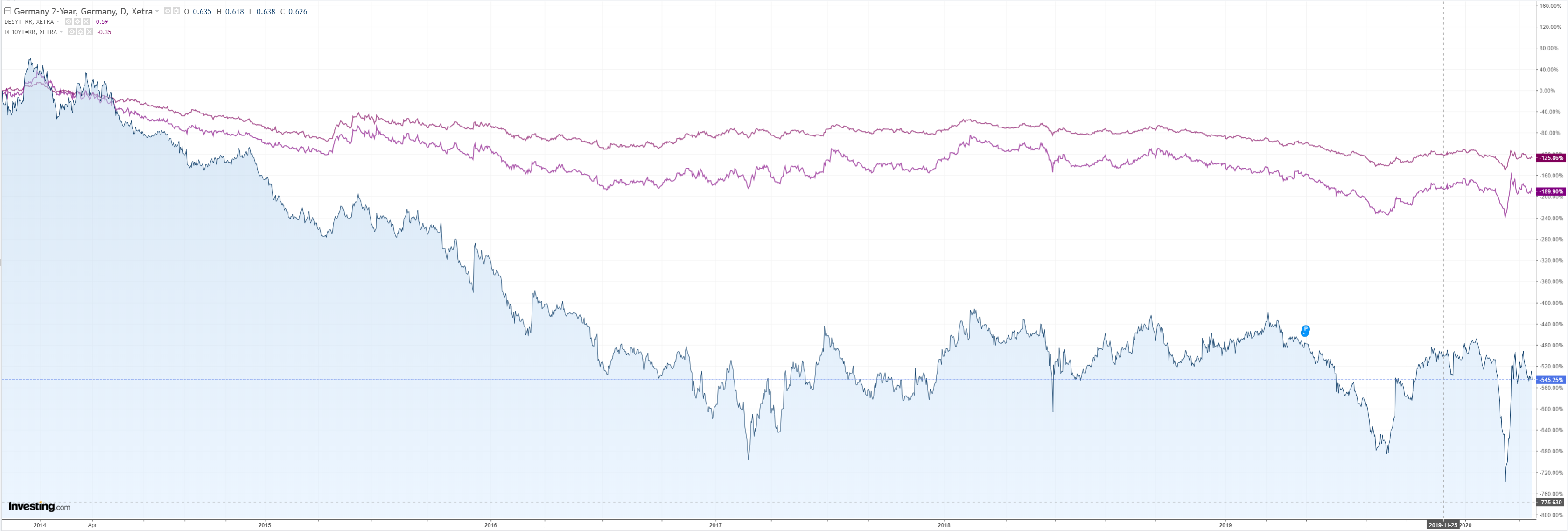

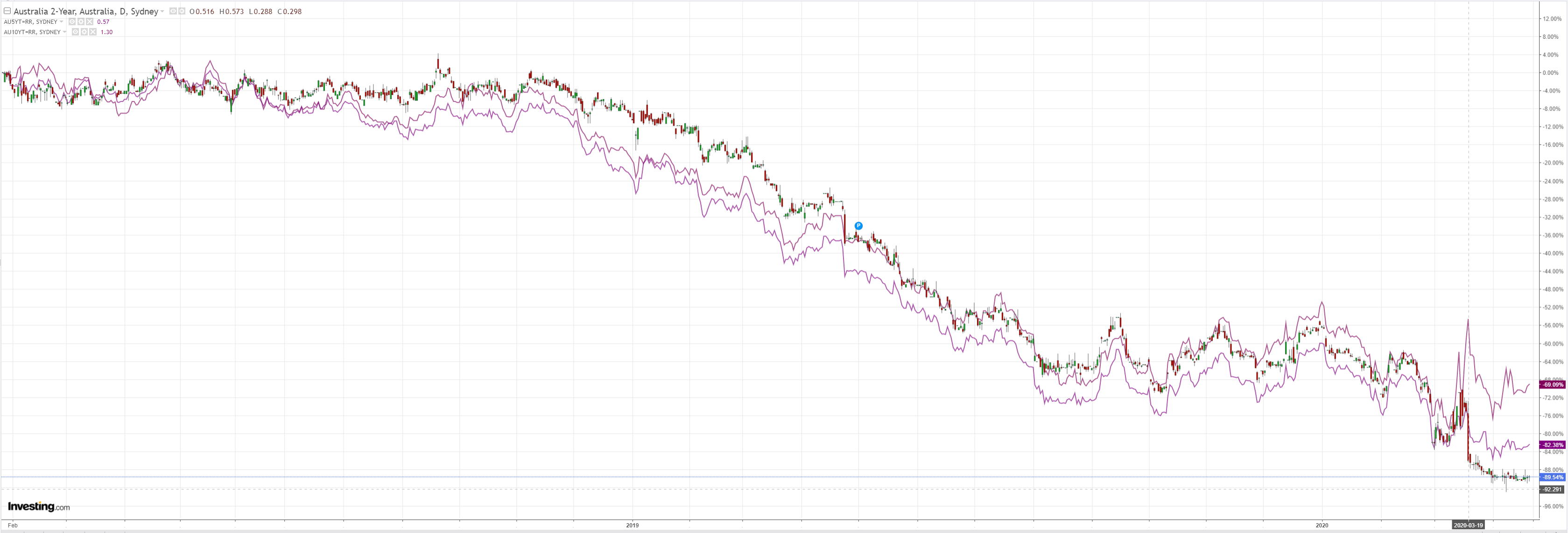

Bonds were bid:

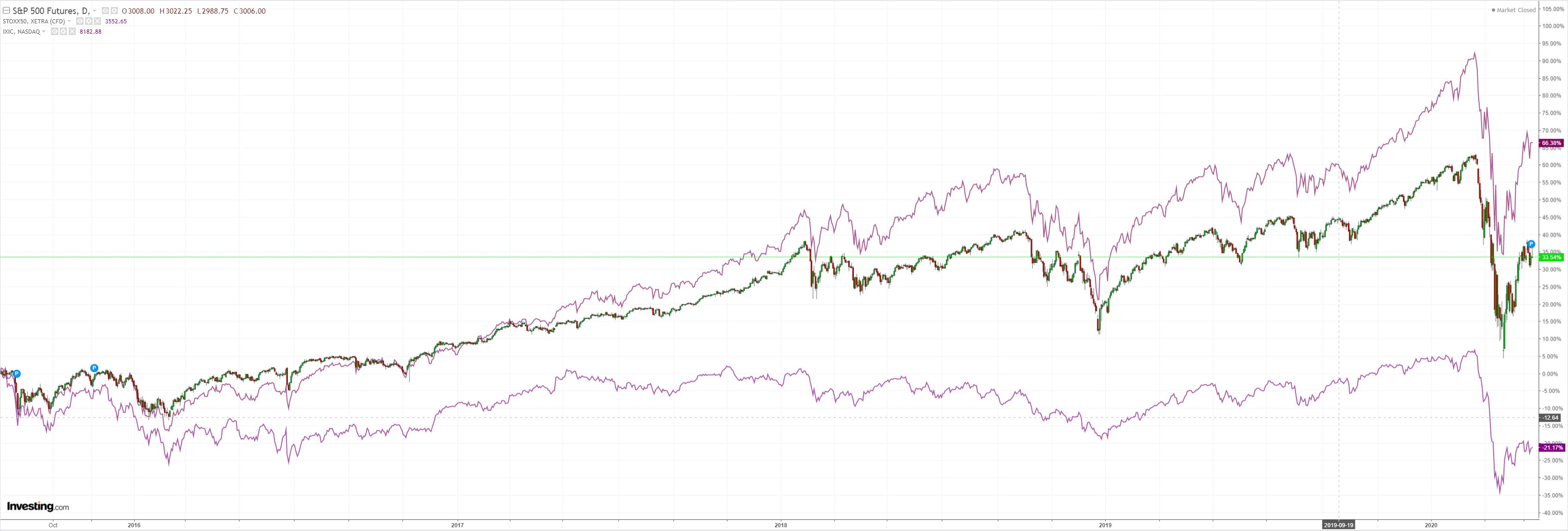

Stocks look tired:

Westpac has the wrap:

Event Wrap

COVID-19 update: The global case count continues to roll over, with latest data from John Hopkins University indicating 74k new confirmed cases worldwide on 22 April, vs 89k the previous day and vs 99k at the peak on 12 April.

Gilead Sciences antiviral drug remdesivir failed its first randomized clinical trial, the Financial Times reported, citing draft documents published accidentally by the World Health Organization. The drug company disputed that characterization.

EU leaders endorsed a short-term EUR540bn stimulus plan but failed to agree on the longer term rebuilding program, with member states split on how to spread the financial burden.

Eurozone Apr. PMIs fell sharply. Services plunged to 11.7 (prior 26.4) with manufacturing falling to 33.6 (prior 44.5). The pessimistic write up warned of a secondary wave of COVID infections and a contraction of around 7.5% of GDP.

UK Apr. services PMI slumped to 12.3 (prior 34.5) and manufacturing fell to 32.9 (prior 47.8). Markit suggested the decline indicated GDP contraction of around 7%.

BoE’s Vleighe stated that the Bank would issue new economic updates as scheduled on 7th May but he highlighted that the contraction facing UK was the greatest in 100 year within a speech outlining the Bank’s QE stance, low rates and the potential to lend directly to the Govt. though the Ways and Means (effective overdraft) facility.

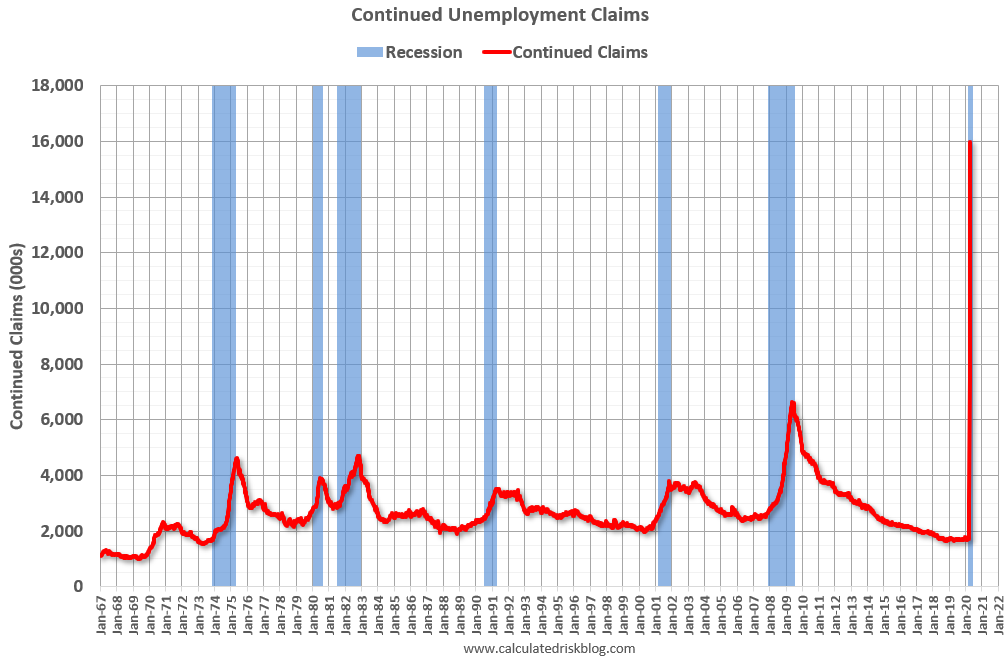

US weekly jobless claims rose 4.4m, close to estimates. The five week total stands at 26.5m. Continuing claims (admittedly two weeks prior) slightly undershot estimates at 16.0m (est. 16.7m). US Markit Apr. PMIs did not fall as steeply as those in Europe. Services did fall sharply to 27 (prior 39.8, est. 30) but manufacturing was relatively steady at 36.9 (est. 35.0, prior 44.5). However, the profile is still very weak, signally “an historically dramatic contraction”. US Kansas Fed manufacturing survey fell to -30 (shy of est. -37) from prior -17 within a clearly negative COVID disrupted survey. March new home sales fell 15.4%.

Event Outlook

Japan: CPI is expected to have remained at 0.4%yr in March. Inflation was stagnant prior to the advent of the contagion, and the combination of demand disruptions and low oil prices will put further downward pressure on sluggish underlying price growth.

Germany: The April IFO business climate survey will reflect the deterioration in conditions, and is expected to fall to 79.7. This read would surpass the low point of the GFC.

US: March durable goods orders are poised for a substantial contraction (market f/c -12.0%); the investment outlook will remain weak in the months ahead.

Dat was apocalyptic everywhere. US unemployment is out of this world:

So, why did the Australian dollar bid? Some are saying being ahead of the virus curve is the cause. Perhaps, for one day.

But Nomura has the truth of it in a more general sense:

- the buying of DM equities in April thus far has been powered by CTAs and other short-term trend-followers along with fundamental value hedge funds and other such perma-contrarians

- Meanwhile, the funds looking least interested in buying have been those that focus mostly on fundamentals. In particular, the global heavyweights among macro hedge funds are still bearish on equities. We suspect that global macro hedge funds will remain bearish until there is some reason to believe that DM economies are on their way to finding a floor.

- Of course, it could still happen that investors quickly become more optimistic before economic indicators have had a chance to bottom out. Should that happen, global macro hedge funds might have to make an emergency rush for the exits from their short trades. However, our impression is that there is not much impetus among global macro hedge funds to rethink their current strategies just now