DXY was down again last night:

The Australian dollar has all but erased the crash now, against all DMs:

And is leaving EMs in the dust:

Gold could not hold new highs:

Oil is not fixed:

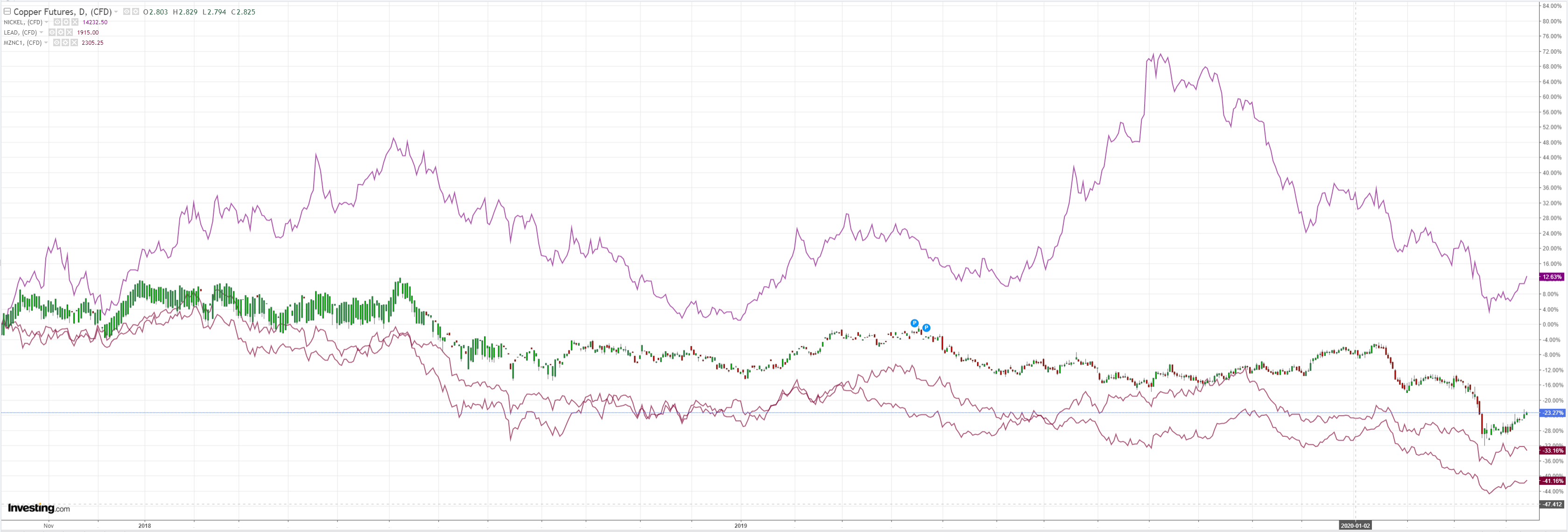

Dirt has hit a floor for now:

Miners rallied:

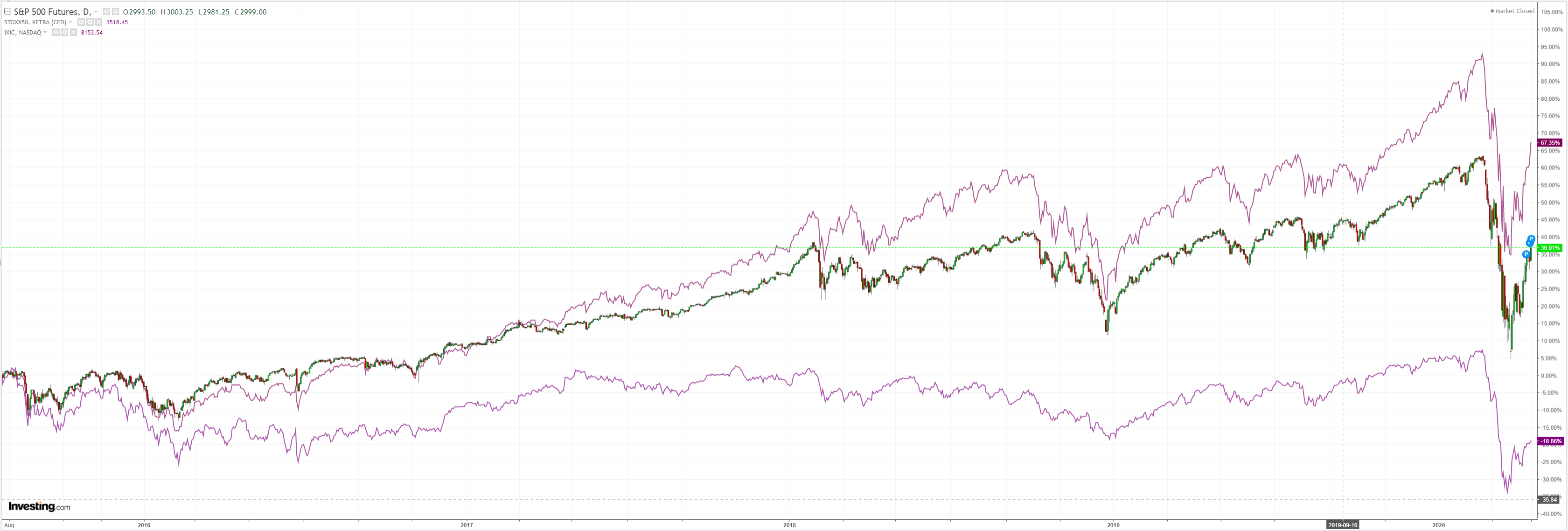

EM stocks too:

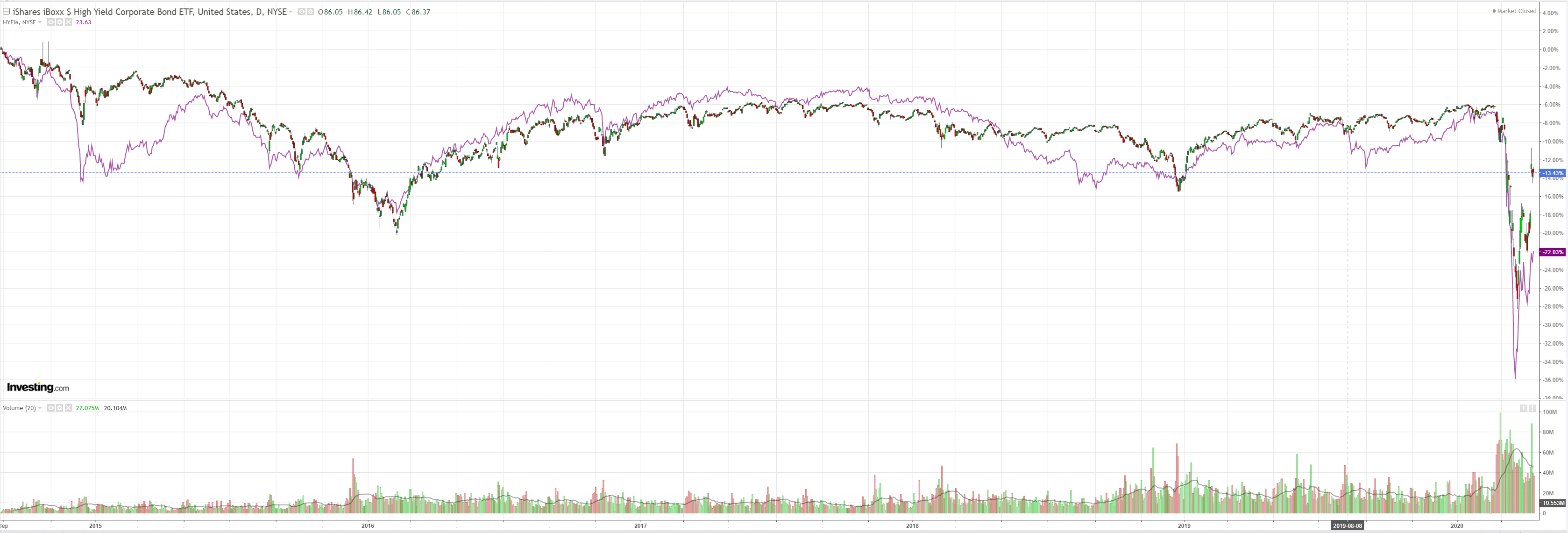

Junk should be getting crushed with oil but instead it is bid on the Fed:

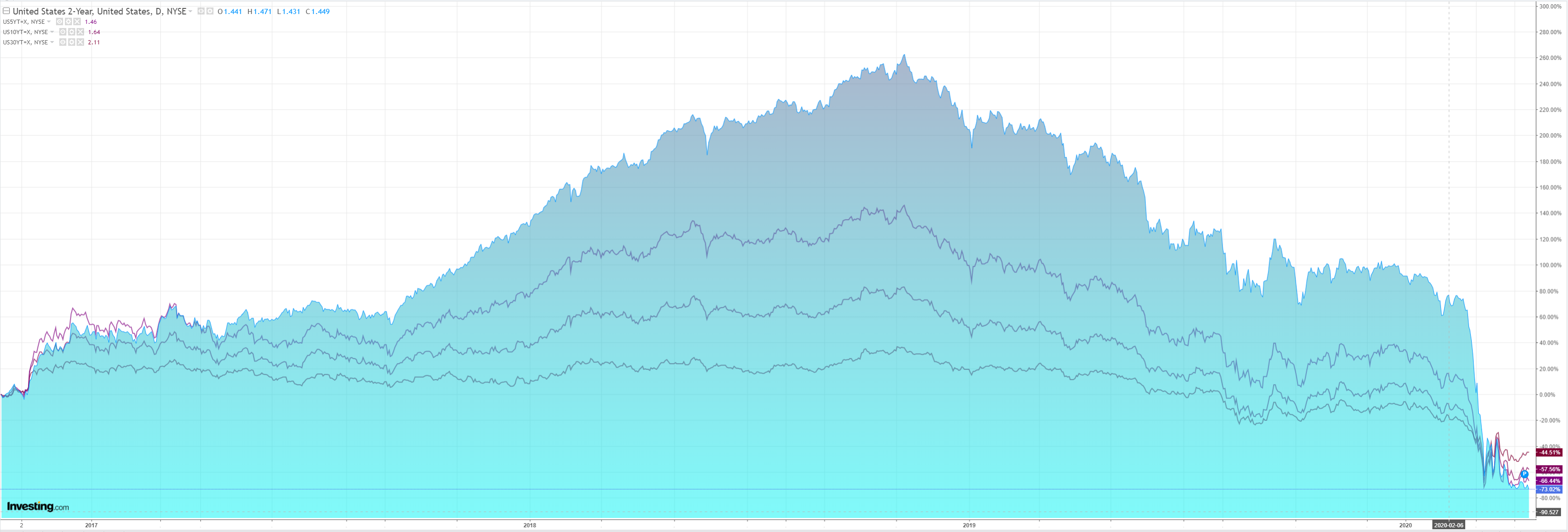

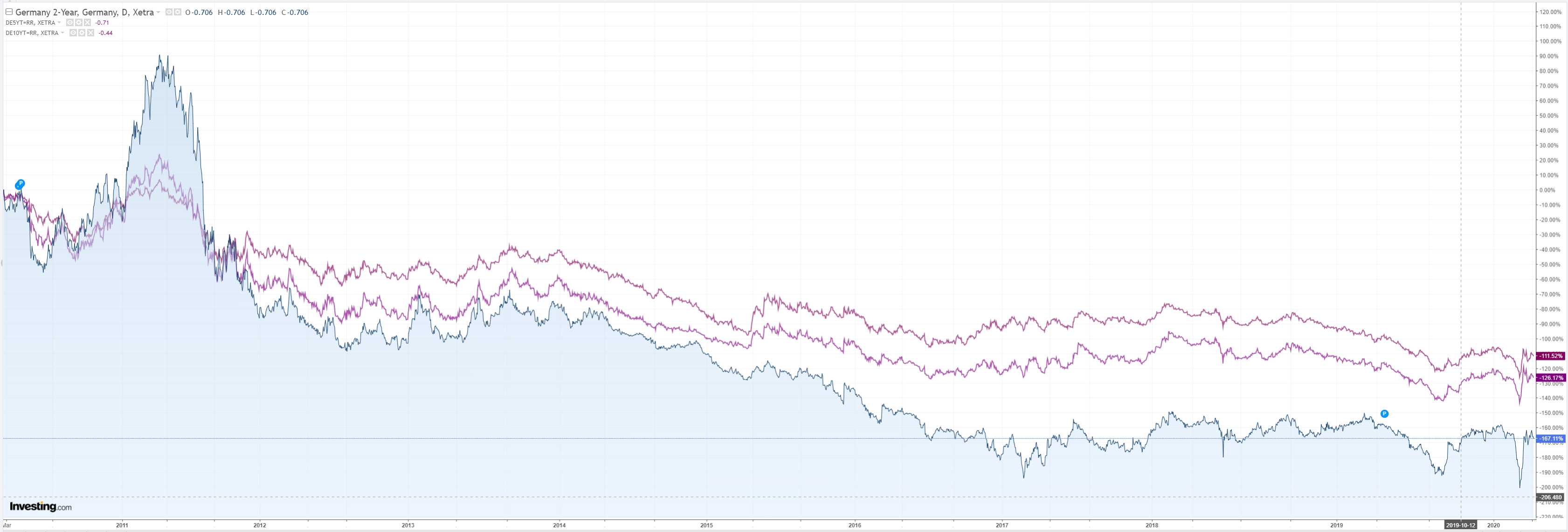

Bonds were bid:

US stocks learned nothing for their last blow-off. Europe is not so stupid:

Westpac has the wrap:

Event Wrap

COVID-19 update: Latest data from John Hopkins University indicates 73k new confirmed cases worldwide on 13 April, vs 75k the previous day.

The IMF issued its latest World Economic Outlook, entitled “The Great Lockdown: Worst Economic Downturn Since the Great Depression”. It projects a 2020 contraction in world growth of -3%, with US -5.9%, Euro Area -7.5%, UK -6.5%, Australia -6.7%, and China +1.2%.

UK’s Office of Budget Responsibility published a “Coronavirus Reference Scenario” in which GDP contracts 13% in 2020, a worse scenario based on a 3-month lockdown where GDP contracts 35%, and a 3-month partial relaxation scenario where GDP contracts 17.5% before returning to “normal activity” in Q4.

The Fed’s Bullard and Evans discussed its rescue policies, saying that a V-shaped recovery was still possible given that pre-COVID-19 fundamentals were good. However, Bullard also said that the US lost income of USD25bn per day during the COVID lockdown.

Event Outlook

Australia: The WBC-MI Consumer Sentiment survey is poised to fall sharply in April, following a read of 91.9 in March (the second lowest print since the GFC). Themes this month will include social distancing restrictions, disruptions in financial markets and the likelihood of a severe contraction in economic activity.

New Zealand: The March update of the REINZ house prices is due. House prices charged higher over the year to Feb (+8.7%yr), and reports for March point to solid demand and continued momentum in price growth. Westpac expects the March food price Index to have risen by 0.2%.

US: The day will open with March retail sales. The market expects a substantial fall of 8.0%, with discretionary spending particularly weak. March industrial production will follow, and is tipped to contract by 4.0% as supply chain disruptions and the demand shock weigh on output. The April NAHB housing market index is also due, and is expected retreat to 55. Finally, the Federal Reserve’s Beige book will be published, and FOMC member Bostic will speak via Zoom to a joint meeting of Birmingham clubs.

Canada: The BoC will deliver its April policy decision. With the policy rate at its “effective lower bound” of 0.25%, the focus will be on alternative measures.

The Australian dollar has almost completed a crash round trip. This is the great benefit of the floating currency. It massively devalues when it is needed so that domestic prices do not need to.

It’s not illogical at this point, either. We’ve got the second-largest fiscal support package globally. The most modest QE. The terms of trade have held up remarkably and the trade account is still in surplus.

From the perspective of an Australian international stock investor it is marvelous as well. The AUD protected our stock global portfolios all the way down. Now it is reloading the hedge much faster than stocks are coming up. Sure, this inhibits returns for a while as the currency has come nearly all the way back while stocks are only halfway. But if you believe, as we do, that more trouble is ahead and capital protection is still the main game, then having such an elastic currency is a huge advantage.

I still see lower ahead for the AUD, likely before it fully retraces.